Wk24 MacroTechnicals - Trimmed Gets Mean

If CPI confirms bleed through into core, there is nothing Warsh can say or do to convince the market otherwise

After a huge positive surprise to the Friday jobs report, the market has gone back to pricing in a full hike by year-end. With CPI this week and FOMC the following, it is worth considering whether that pricing is justified and whether the incoming Fed chair Kevin Warsh pushes back on such a scenario.

Let's take stock of the major issues impacting inflation. To start with, it's not quite clear whether the US-Iran ceasefire is holding up with strikes and retaliations gradually re-escalating in recent weeks. It's also not quite clear the US is politically capable of giving Iran terms they would agree to - they're in no rush at all, they genuinely possess the ability to drag out talks knowing that time works in their favour while the world digs deep into their Oil reserves and, knowing peacemaker-Trump is unable to start a full-blown war. The implication of those points put together is that the price of oil and all its by-products is simply not set up to fade anytime soon. Finally, the US economy proving resilient suggests there is no immediate demand destruction to offset the rising trajectory of inflation which will, with time, bleed into core/underlying inflation and bolster the case for a hike.

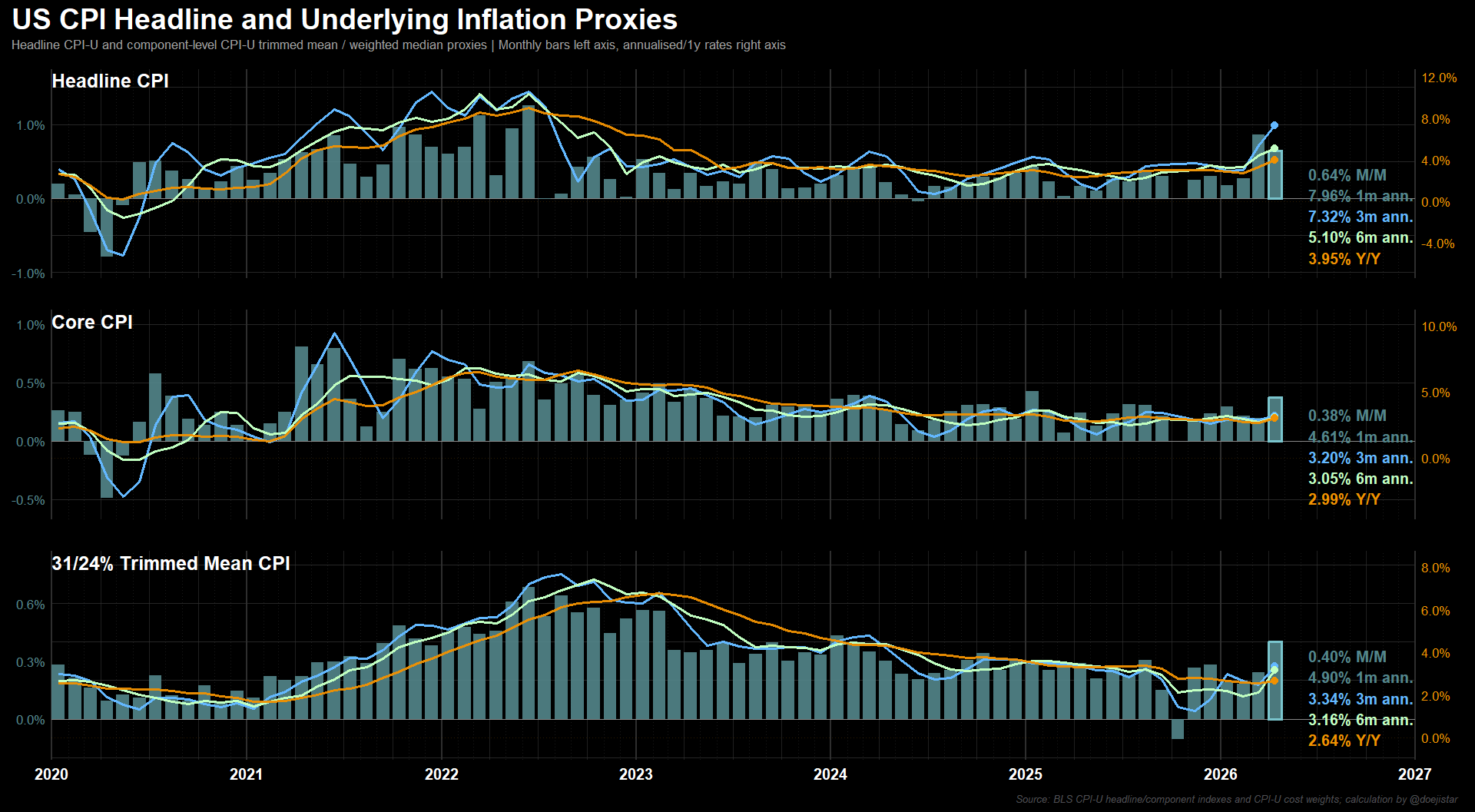

As for Warsh, he's stuck. It's virtually impossible to argue against upside risks while they are progressively stacking up, and looking at trimmed mean (underlying inflation) measures is unlikely to present a case anytime soon given core CPI has jumped up +0.38% which equates to an annualised rate of 4.61%, and the trimmed mean increase was even stronger at +0.40% in April.

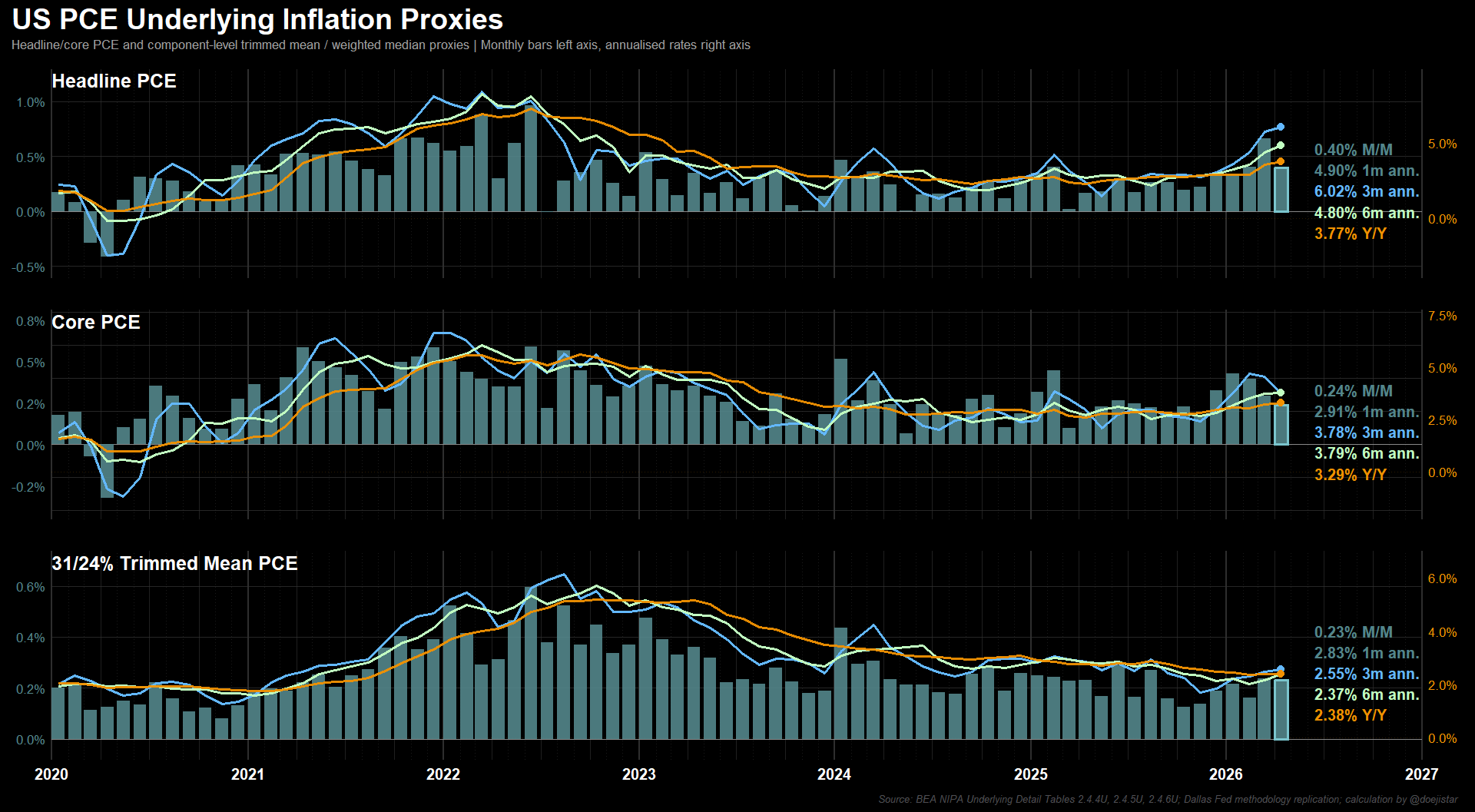

Core PCE shows a softer April print but interesting to note that the trimmed mean PCE (Dallas Fed's methodology) is showing a rising 3 and 6-month trend.

PCE isn't released until after next week's Fed meeting however so as we have seen just one month to possibly suggest energy impacts have begun bleeding into underlying inflation measures, whether that is becoming a trend will be the key focus for CPI, which will have a significant bearing on how front-end rates react, and therefore the dollar, precious metals, and stocks this week.

Subscribe to stay in the loop, if you haven't already. Subscribe to Premium for real-time analysis and opportunistic trade ideas.