Wk20 MacroTechnicals - Is This The Top?

Stunning rally has challenged my bearish view but energy related risks accompanied by tighter financial conditions with little interest in the left tail argue for caution

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.”

- Sir John Templeton

As readers will know, for the past month I have held the view that a stock market rally would be difficult to sustain given the macro backdrop being shaped by the energy shock. That has been proven quite wrong with the S&P500 rallying some 15% since the end of March. As a result, I've missed that rally and that was a rather huge miss. On a personal level though, I find myself being consoled that a miss was probably due after consistently nailing major turns over the years (as some of my peers and readers will know). But even as I attempt to reassess macro and market conditions as objectively as I can at this point after being getting it so emphatically wrong the past month, I still have enormous difficulty coming to terms with the rally being a durable one over the medium term, even though I remain very bullish over the longer term on AI excess demand persisting well into the future.

As I begin to put down my thoughts for the week, I'm somewhat randomly remembering a link EMH once had on his profile page which would have taken you to the above page, though I do seem to remember it being slightly different to what shows now. A site with the URL address asking whether “this is the top” is answered with a big fat "NO" in perpetuity. The irony of that perpetual (I think) message especially striking now, as if it captures the current market perfectly - every warning indicator looking premature, every small pullback being buyable, and every macro concern losing against the belief that stocks can keep rallying.

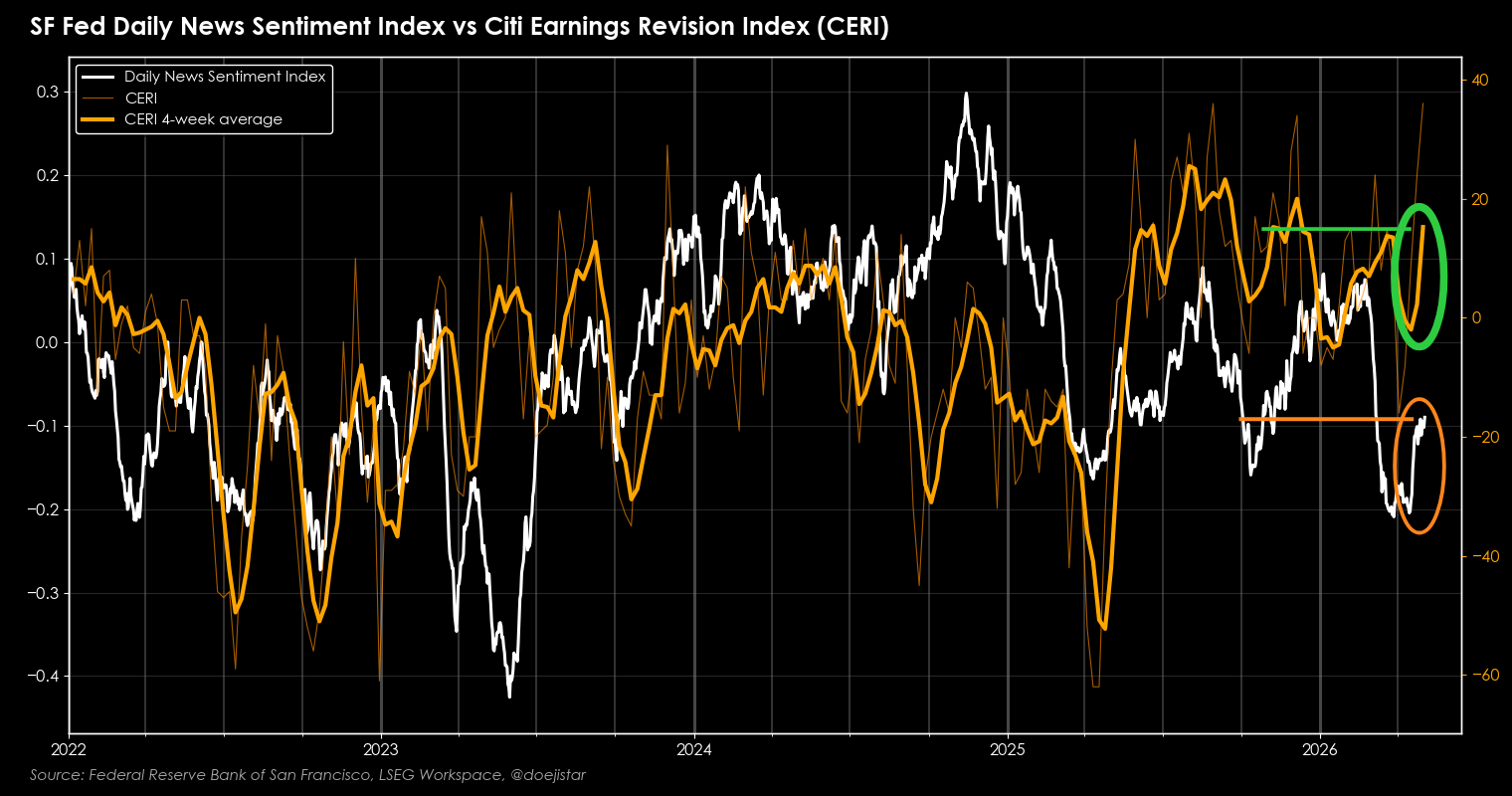

The stunning rebound is perhaps best captured by this chart. CERI (measures net EPS revisions) rebounding back to 2025H2 levels reflects a particularly strong Q1 earnings season. The SF Fed News Sentiment Index (measured from news articles) reflects a big improvement since the height of the war likely to be driven by a combination of earnings beats, AI narratives, as well as a ceasefire coming into place with some optimism of a settlement being reached; but the sentiment index remains negative on balance possible reflecting lingering macro concerns due to higher energy prices and cost pressures on the economy.

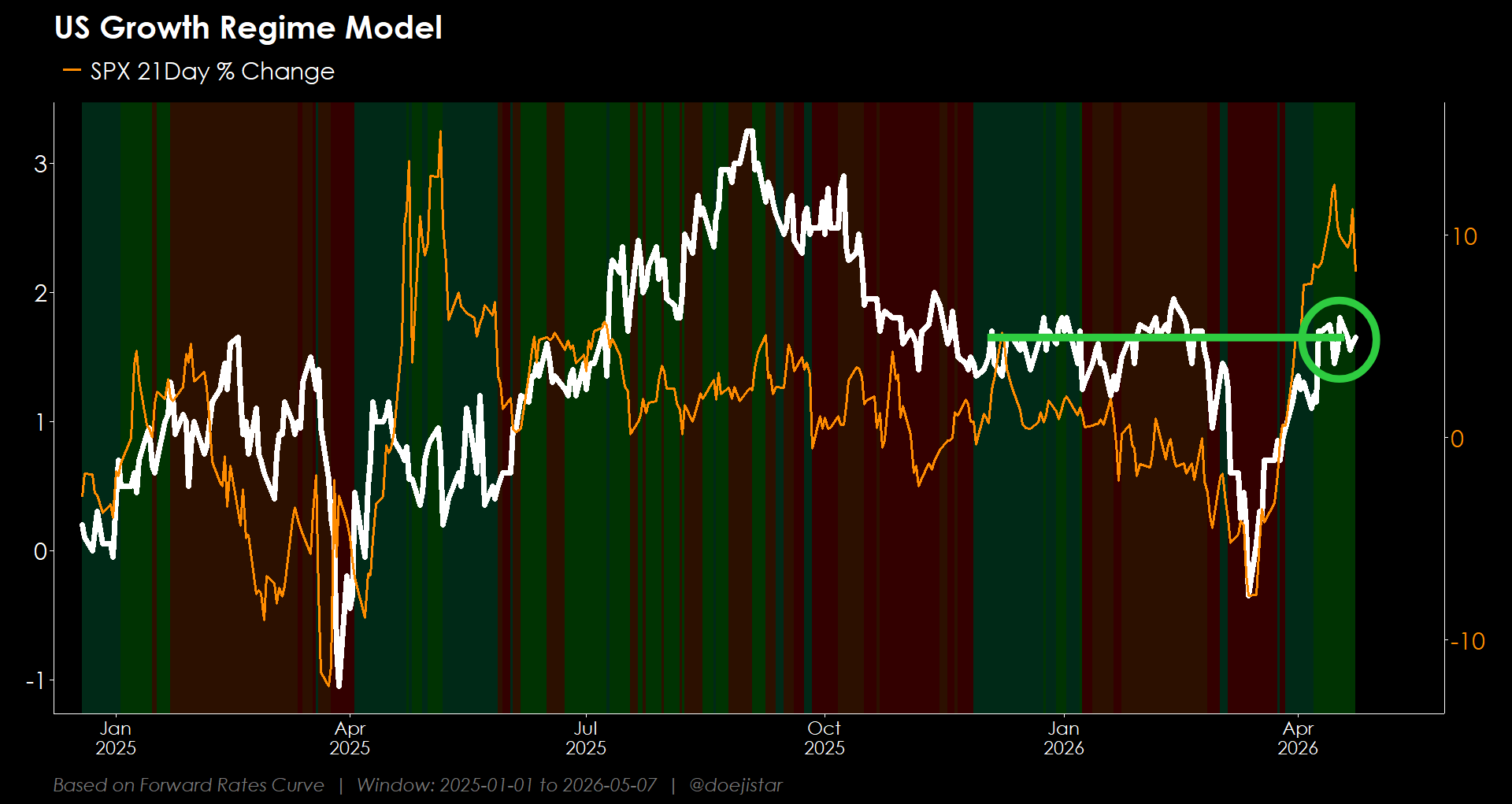

But it's not just stocks and earnings expectations believing in a strong growth outlook; the bond market (as the ultimate macro indicator) has also repriced for higher growth via the forward rates curve, putting growth expectations being as strong as it was before the war.

Circling back to stocks, it is important to recognise that the recovery has been very uneven. Forward multiples for the S&P500 is now 2.5 below year-beginning levels, 1 multiple below for the Nasdaq, and almost 3 multiples above for Semis. If there is any indication that the stock market will be correcting, we should see that in the semis and I do think there should be some pause for thought due to the risk of a more persistent energy shock becoming increasingly palpable as I highlighted last week in Wk19 MacroTechnicals - Sell In May & Go Away? piece that AI Capex will not be immune to the developing macro risks. It assumed a resolution around the Strait of Hormuz would not be in sight, and therefore supply chain disruptions and cost pressures to persist and permeate throughout all levels of the economy and financial conditions to tighten. A scenario in which even AI capex projects would also be impacted, and in turn has the potential to create fresh uncertainties around profitability and ROI timelines.

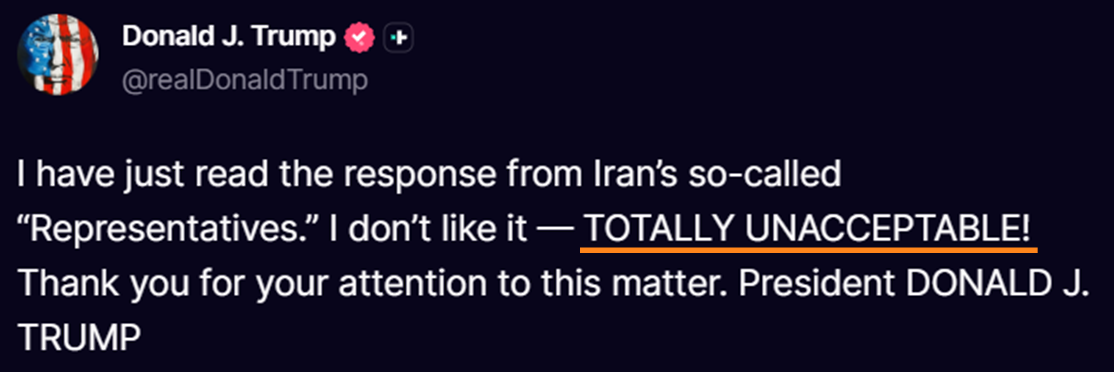

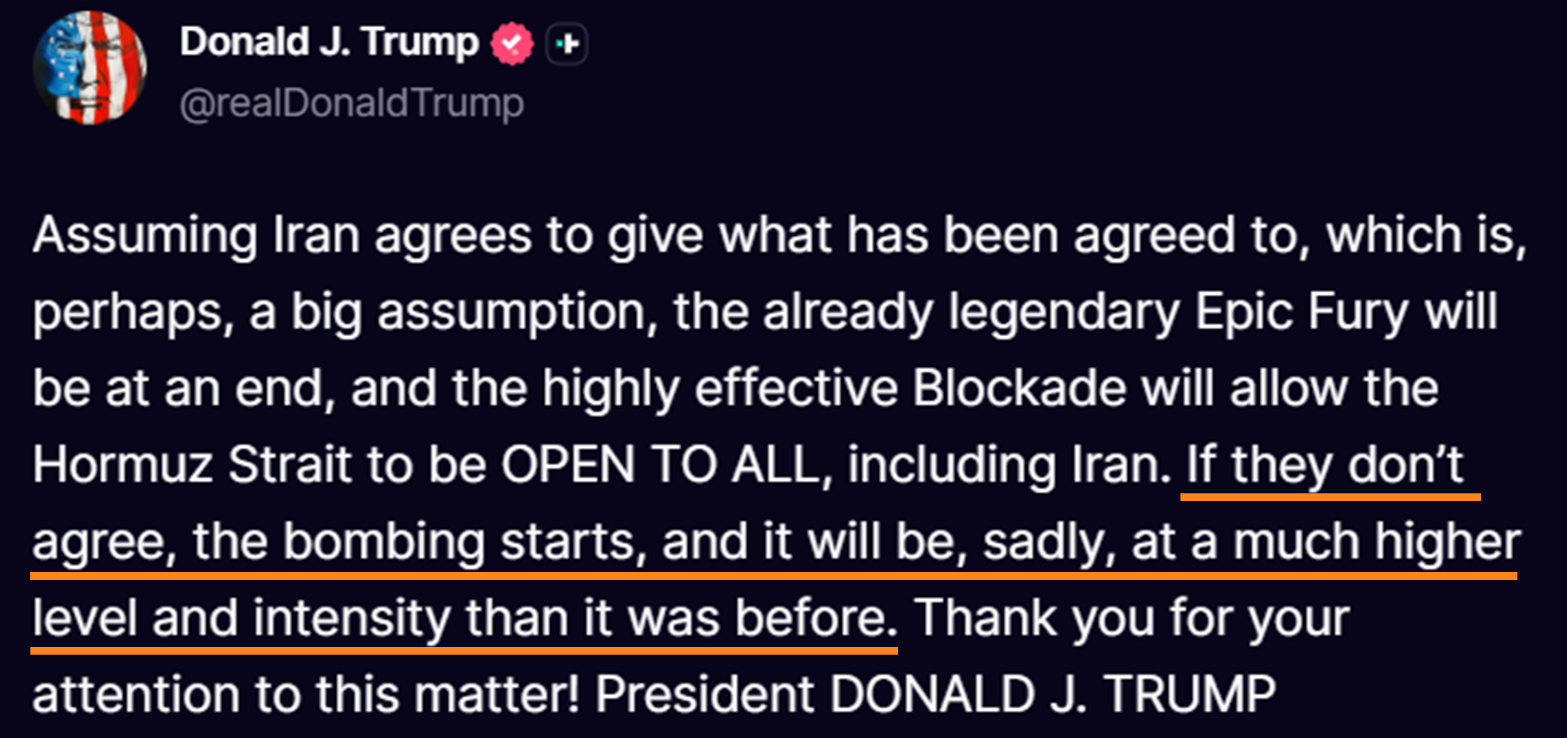

Meanwhile, the market has been riding on a lot of 'deal optimism' being expressed by certain government officials as well as a certain news outlet continually implying that a deal was highly likely. And as was expected according to our game theory framework we have set up over a month ago in Wk13 MacroTechnicals - Echoes of 2022, those risks have not lessened at all this past weekend with Trump rejected the latest Iranian response.

The pathway to a deal remains narrow, and the conflict looks set to continue as we embark on a new trading week.

If you found this useful, consider subscribing to stay in the loop. Premium members also get real-time reactive analysis, opportunistic trade ideas, via our highly active Discord server.

Later this year, we’ll launch our MacroTechnicals course, covering both macro and technical frameworks we use across swing and day trading the market, as well as aiding management of our investment portfolios. Existing Premium members will receive it for free, so take advantage now to lock in access before it launches as a higher-priced standalone product.

Let’s dive into the macro and market technicals for trade ideas.