Wk23 MacroTechnicals - Dispersion Trap

Comfortable markets, uncomfortable backdrop

The macro backdrop remains uncomfortable. Inflation cooled at the margin, but not enough to remove the risk of a feed-through into stickier underlying (core) inflation. At the same time, the US consumer is looking more fragile with real spending and income growth on the decline while recession concerns build. Outside the US, the picture is mixed but increasingly policy-sensitive. Europe still faces sticky core inflation, Canada is flirting with recession again, Australia and Japan have seen softer inflation impulses, while the RBNZ has shifted decisively hawkish despite a weaker growth outlook. The broader theme points to a path of tightening financial conditions, with central banks increasingly focused on inflation over growth risks.

In the face of that macro backdrop, the markets still appear calm but there are some technical risks with the market getting increasingly stretched, volatility metrics at low extremes, and the so-called dispersion trade looking dangerously crowded again - a condition that has preceded meaningful pullbacks in stocks, as well as being vulnerable to negative headline triggers often leading to a burst in short-term volatility.

Of course, none of this may matter much if Trump finds the off-ramp that markets are eagerly expecting. Yet despite repeated promises and optimistic statements from officials, mediators, and Trump himself, the conflict is now entering its fourth month with little evidence of a clean resolution. Meanwhile, the ceasefire Trump says is going “great” continues to feature US “self-defense” strikes, Iranian retaliation, and Kuwait caught in the crossfire.

That's an awful lot of discomfort...

Macro

FRAGILE US CONSUMER OUTLOOK

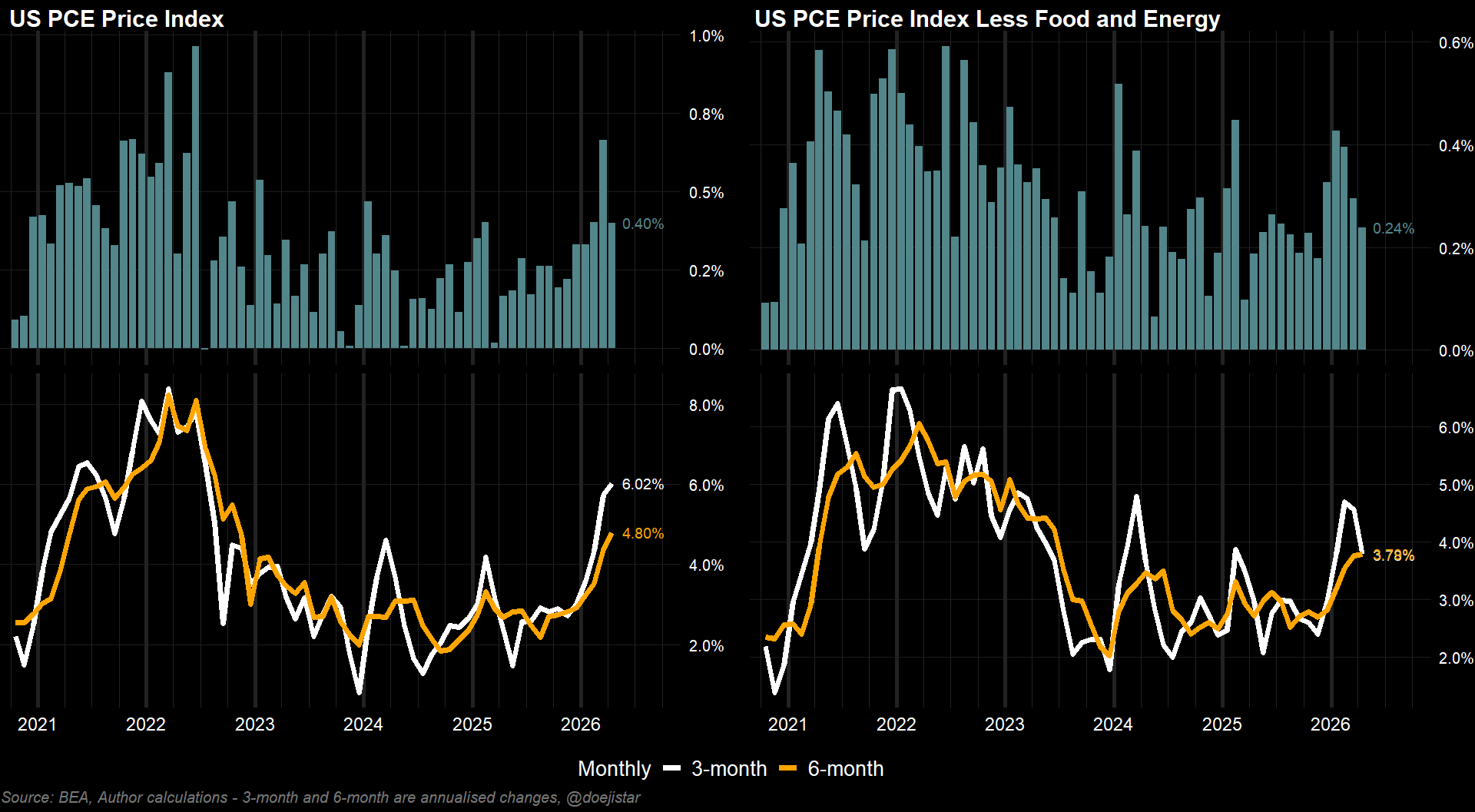

Softer than expected PCE to soothe fears of inflation accelerating rapidly but still elevated at 0.4% to keep the 3 and 6-month rates running at the strongest pace since 2022. On the other hand, core PCE saw its weakest monthly increase so far this year taking the 3-month annualised rate down to 3.78% from above 4.5% in the prior 2 months. While gasoline and food inflation are the main drivers of higher inflation for the moment, the risk (and tendency) is that it will soon translate into higher stickier inflation.

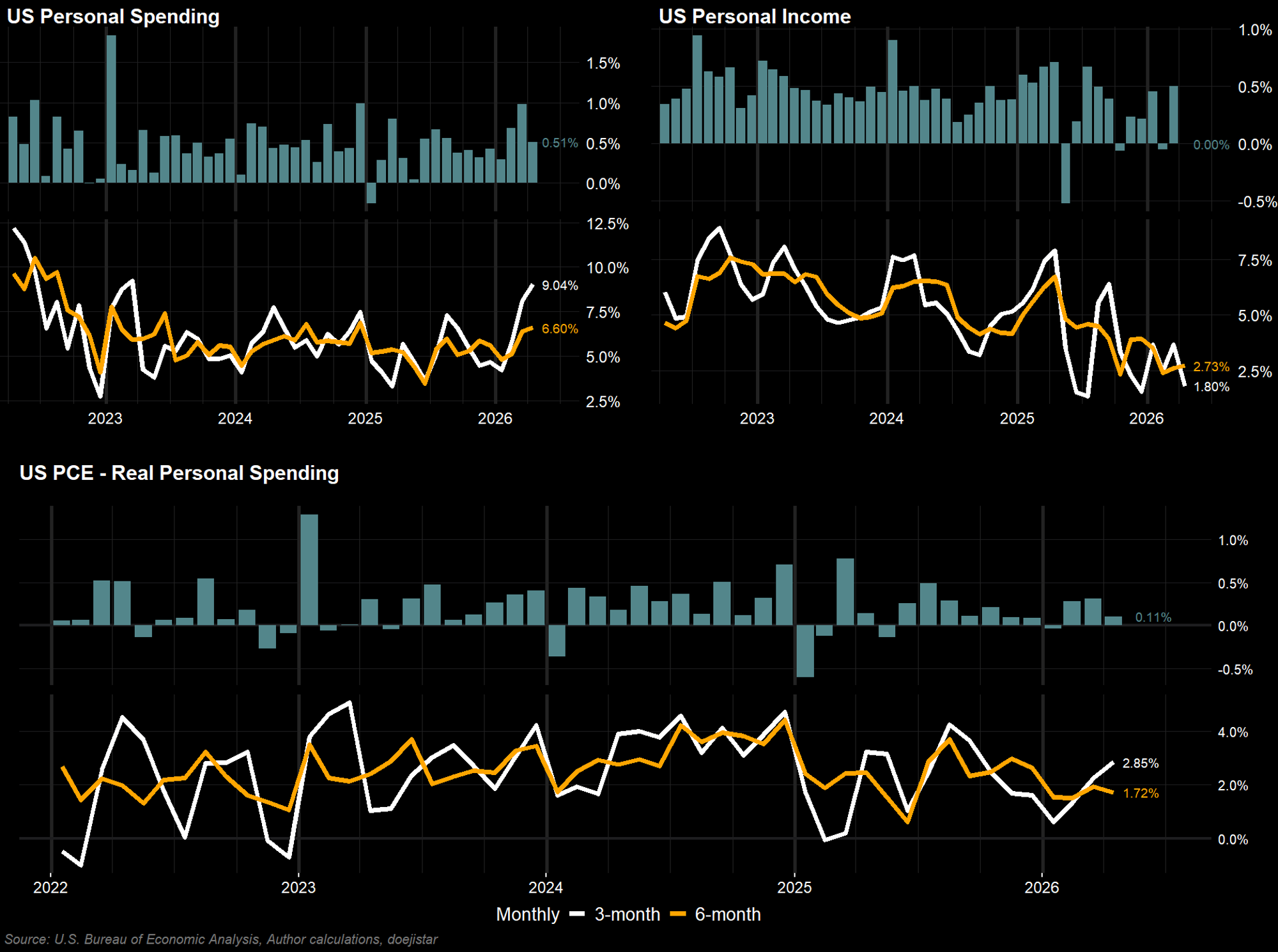

Nominal spending stays resilient to keep the rising trend intact, but real spending though positive still looks far less impressive. And with income growth slowing sharply, the outlook is highly fragile should incomes continue to fall out of pace.

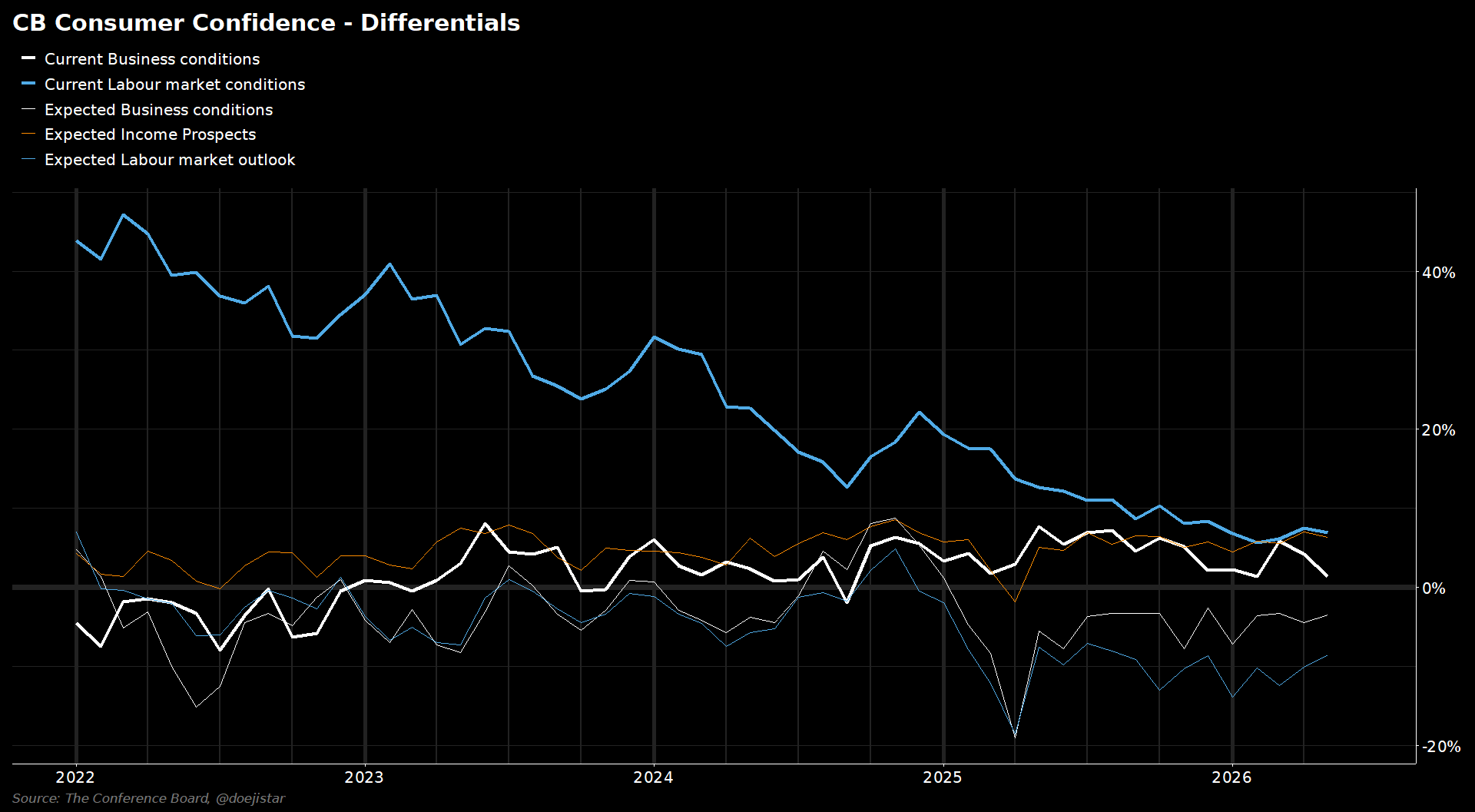

Inflation and higher gasoline prices have weighed on consumer confidence but there is some optimism about the future to offset those primary concerns.

Component differentials show consumers' perception of current business conditions to be at the pessimistic end of recent years while references to prices and oil and gas were noted to have increased in frequency for a second consecutive month, with mentions of war, geopolitics, and conflict being elevated. Other highlights from report:

- Big-ticket purchase intentions softened pointing to weaker discretionary demand ahead, and spending behaviour remains defensive being focused more on essentials and lower-cost consumption.

- Inflation expectations eased slightly but remain elevated. Nearly half of consumers still expect higher interest rates over the next 12 months.

- Recession concerns also increased, suggesting consumers are becoming more cautious on the economic outlook.

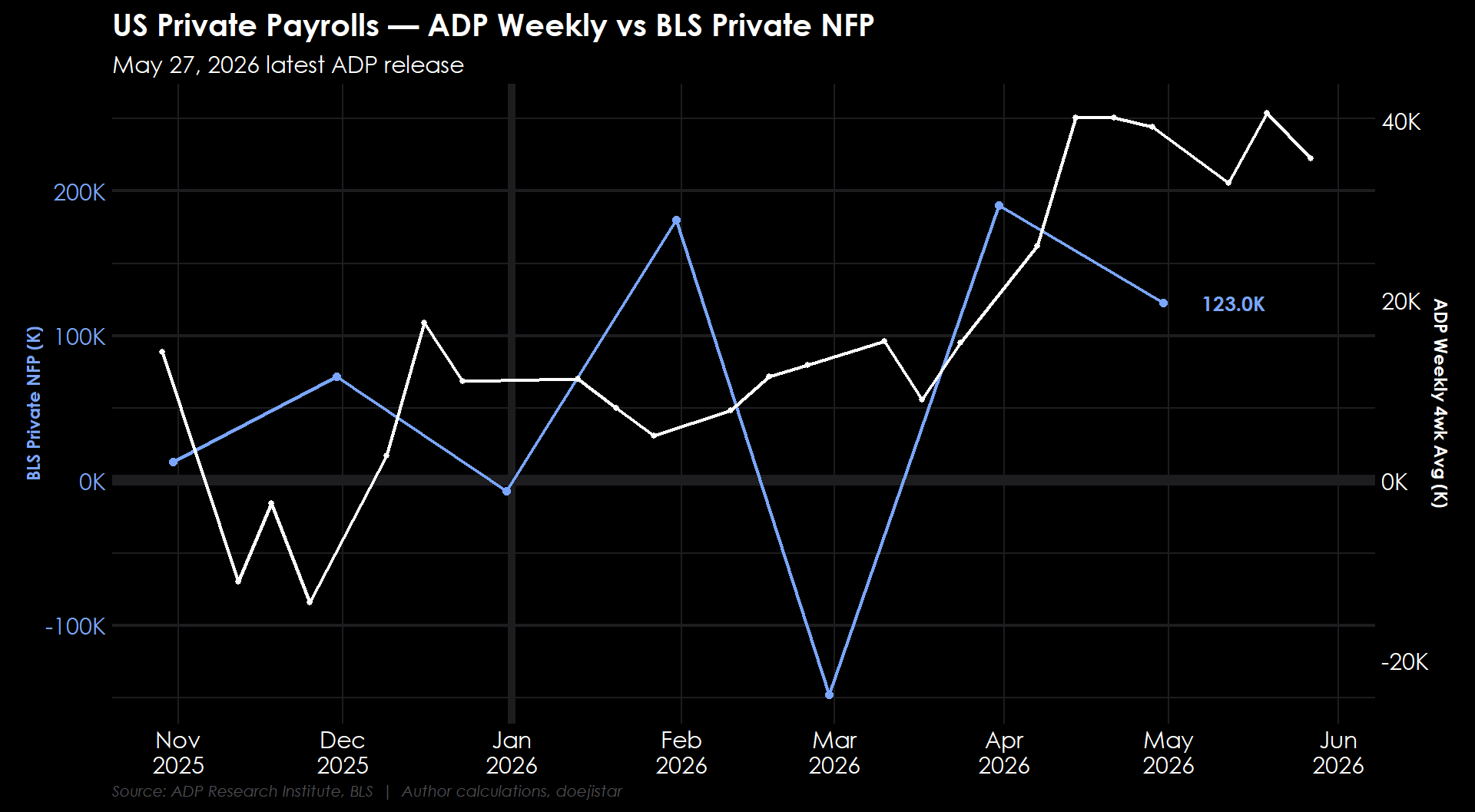

The bright news is that the labour market data, though one of the more lagging macro indicators, appears to be in decent shape. ADP's weekly private payrolls estimate has held steady though May.

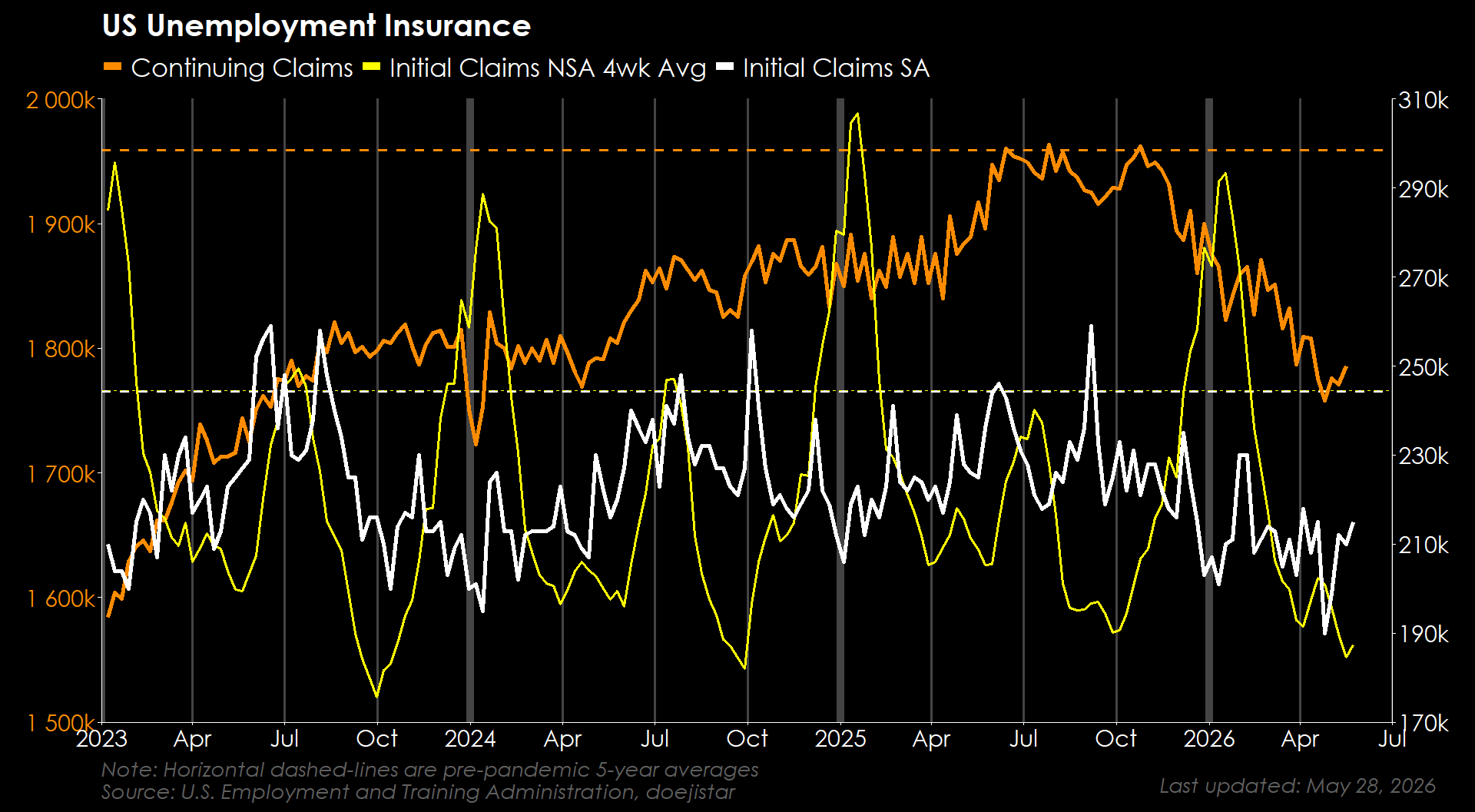

And unemployment claims are still at very low levels.

It is therefore no surprise that commentary from Fed members have shifted more hawkish as they remove their easing bias, and the case is certainly building for the next move being a hike than it will be a cut due to the resilience of economic data that may support underlying inflation pressures as a result of the recent surge in energy prices.

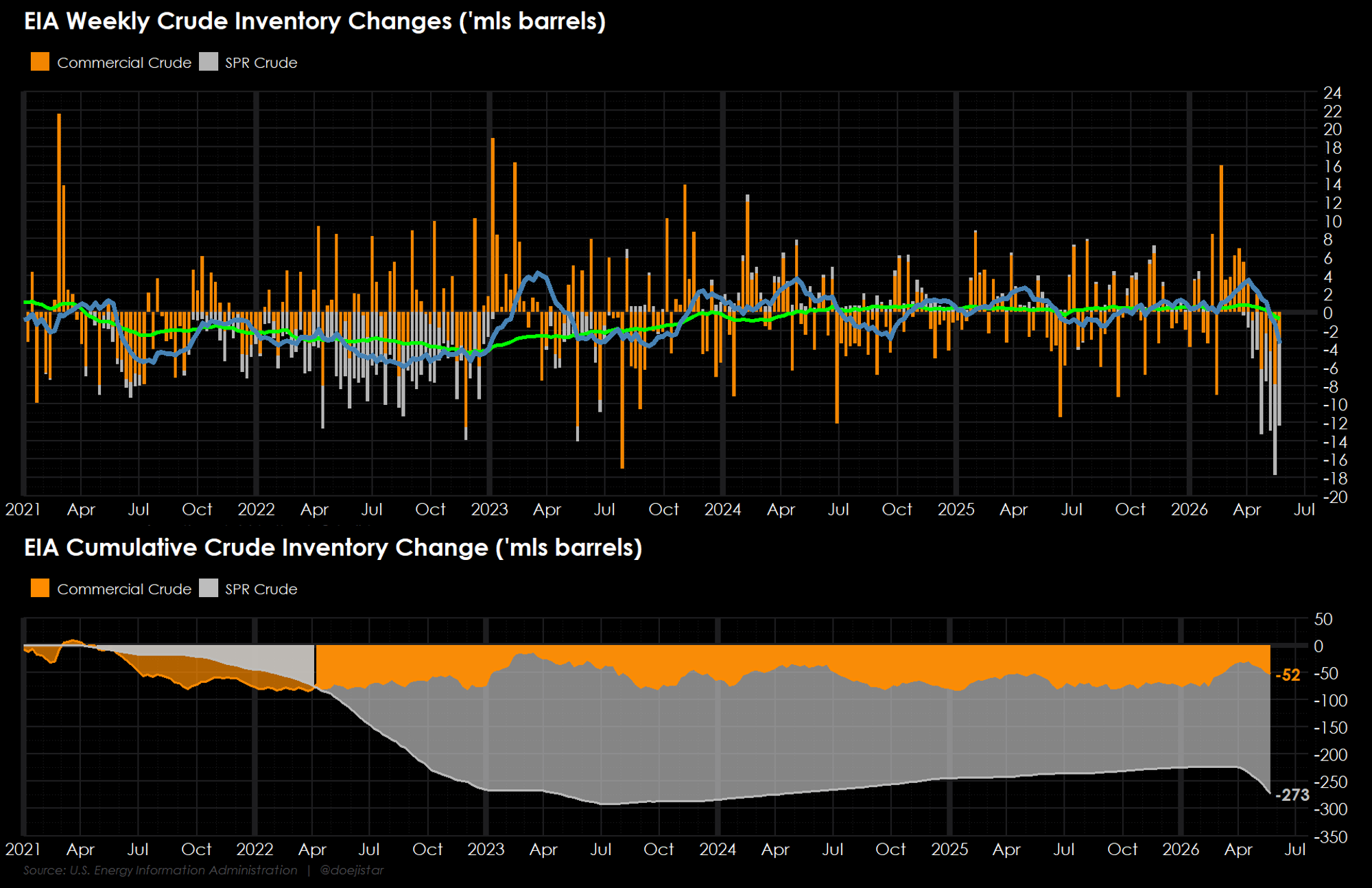

OIL SUPPLY INCREASINGLY UNDER PRESSURE

Market seemingly in a not-panicking-yet mode, but lack of delivery on a promised deal while inventories are drawing down poses an unignorable risk. Particularly in the absence of a deal over the coming weeks.

EX-US DATA AT A GLANCE

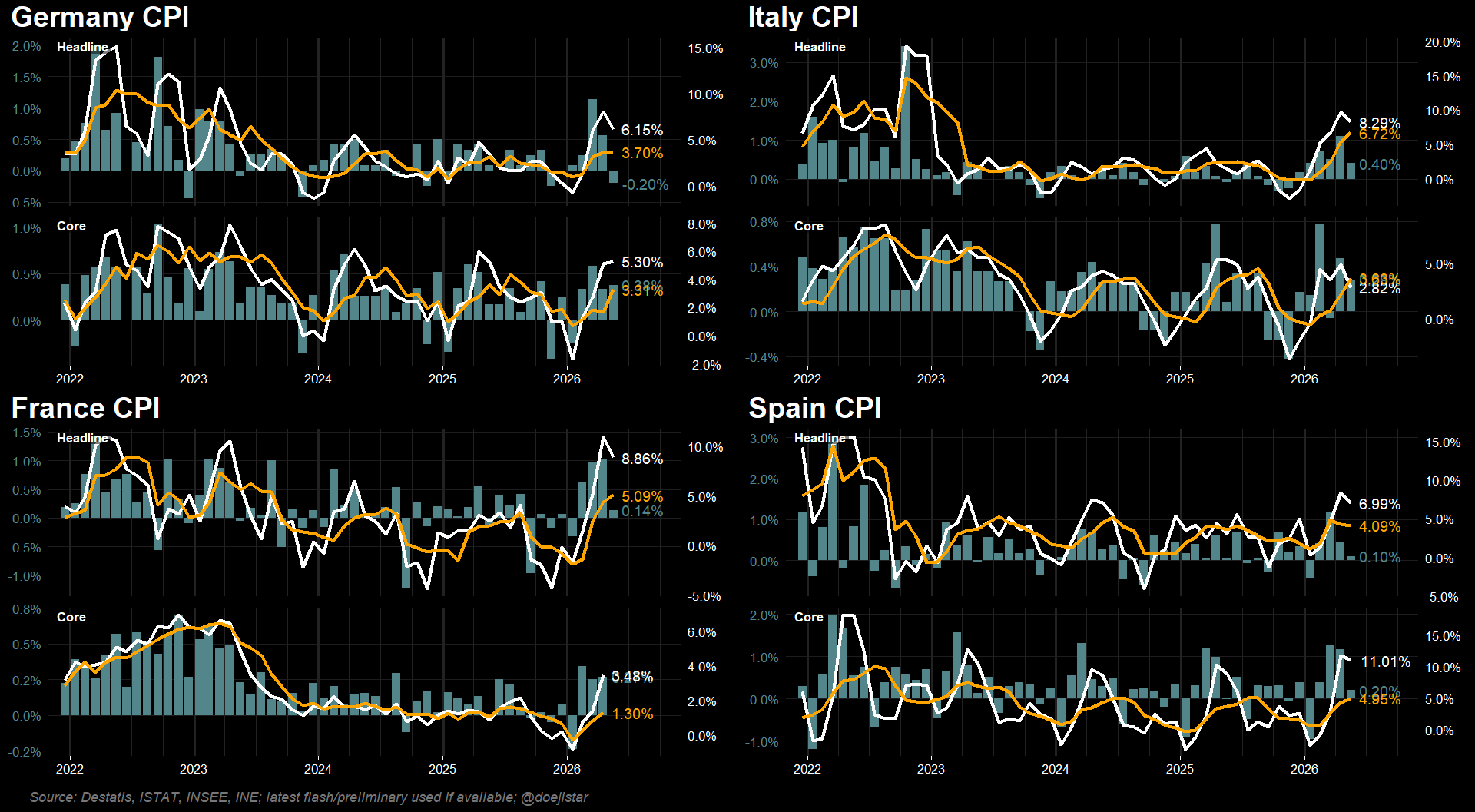

Latest preliminary CPI data from Europe's Big-4 showed a downshift from the prior month, but core remains sticky. That still leaves inflation mostly running well above the current 2.15% policy rate at the ECB.

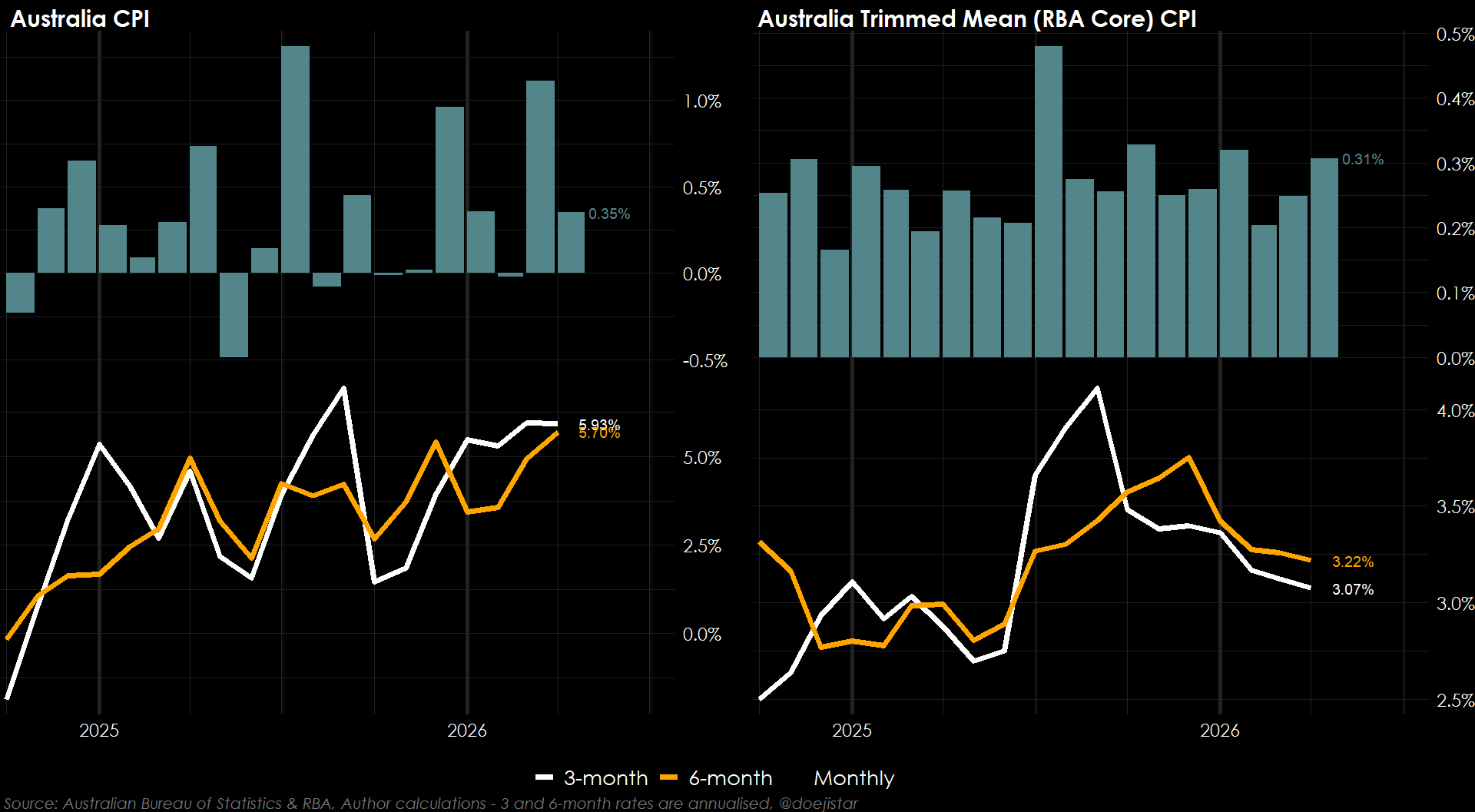

Australia CPI was 0.36% which was a sizeable miss against expectations for 0.6%. Trimmed mean equaled expectations but prior month saw a downward revision to keep the 6-month annualised rate in the low 3s, versus the RBA Cash Rate currently at 4.35%.

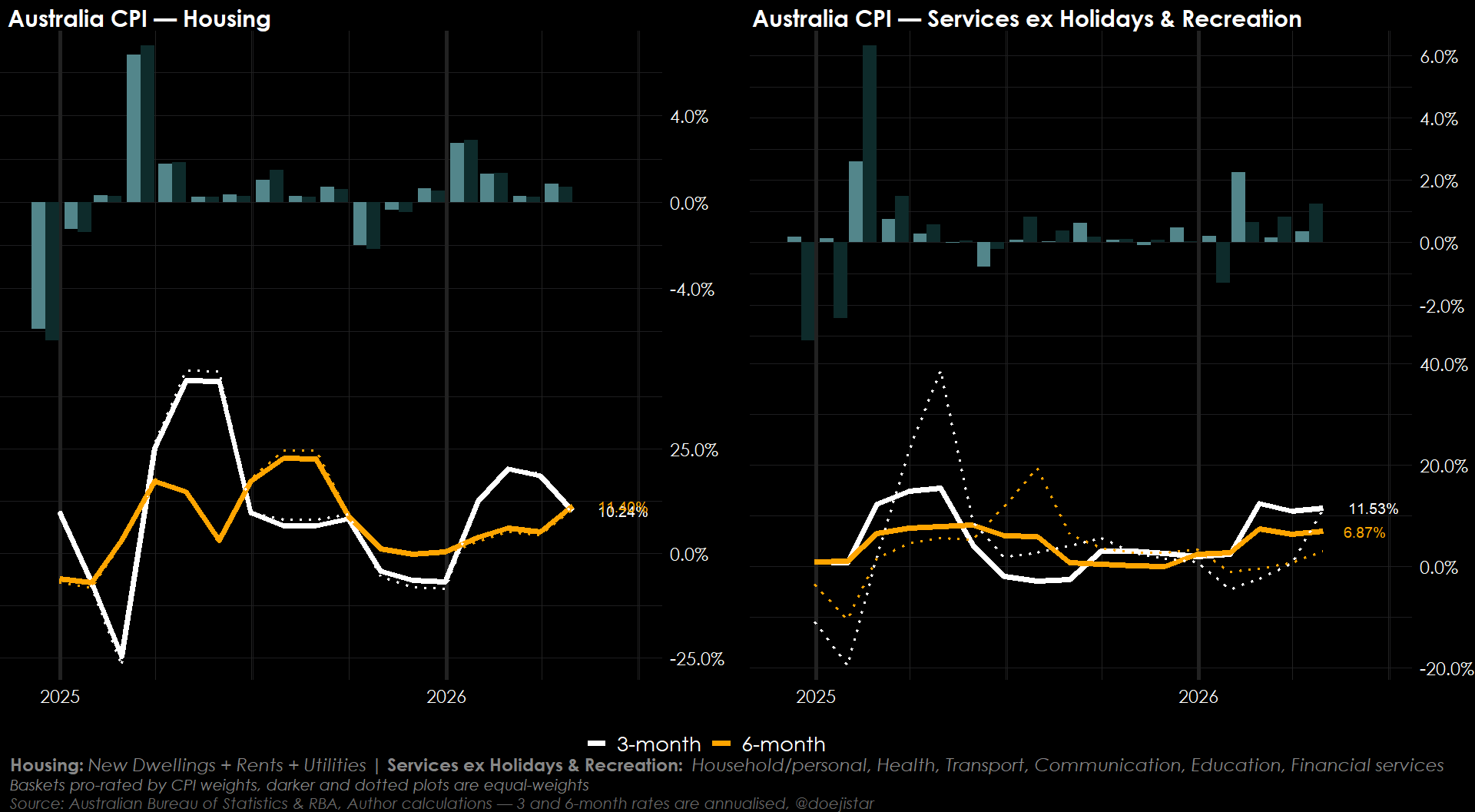

Closely watched Housing inflation sloping off after the rapid acceleration at the start of the year will also have helped to temper further hiking expectations.

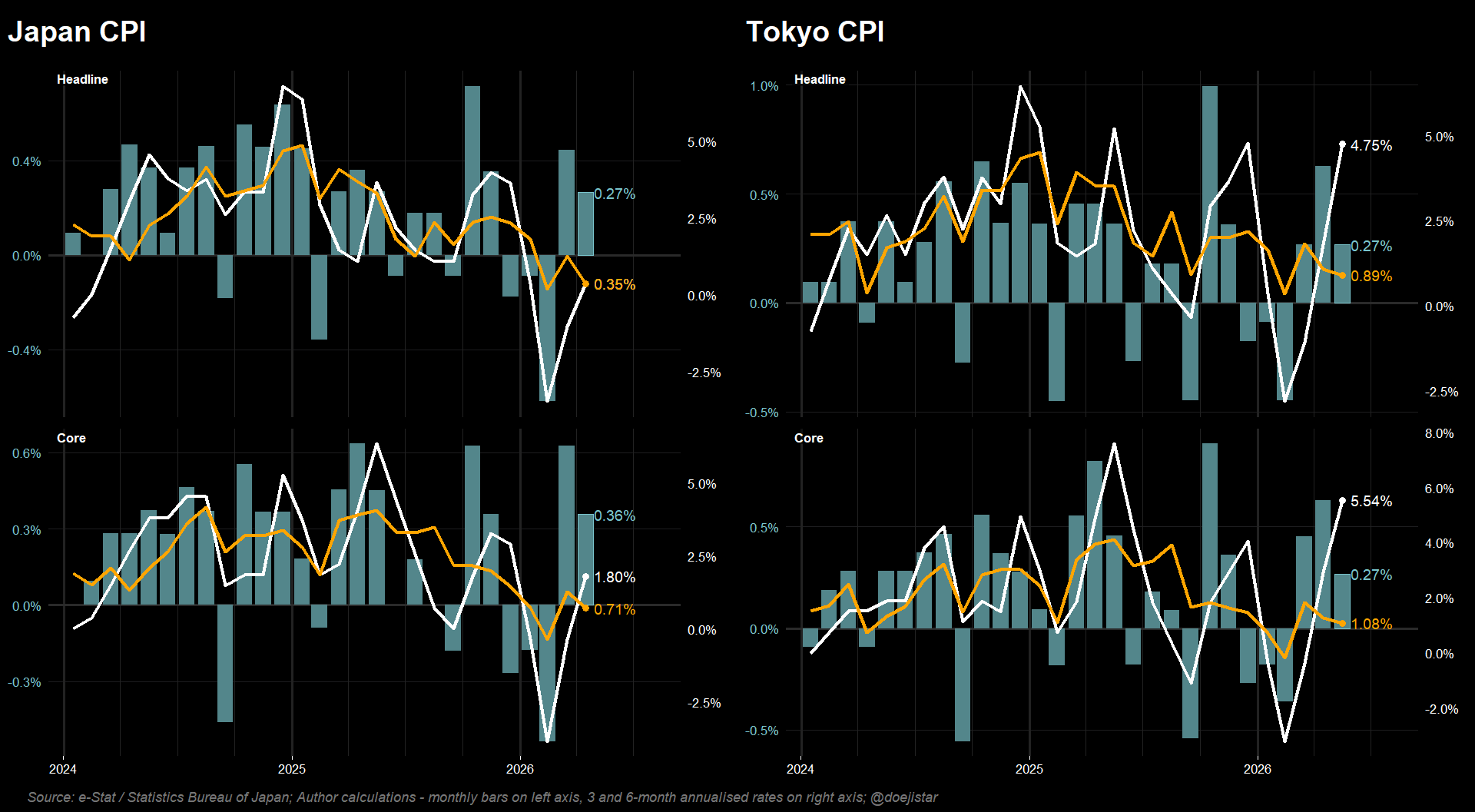

Tokyo core CPI was 1.3%, below the expected and previous month print of 1.5% to keep the 6-month annualised rate steady at 0.9% and 1.1% for core.

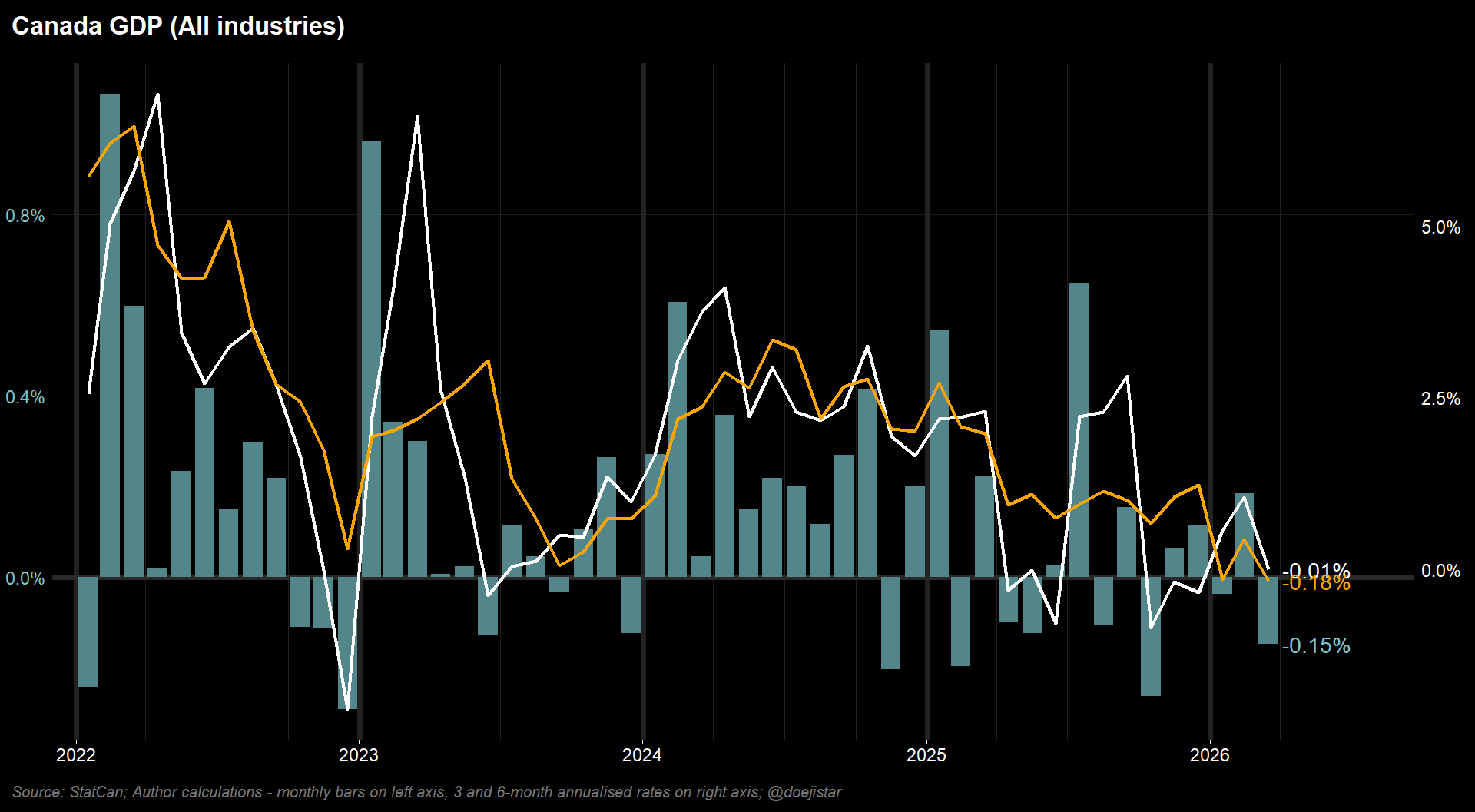

Canada posted a negative monthly GDP print at -0.15% to bring the longer term rates into negative and the economy teetering on recession, again.

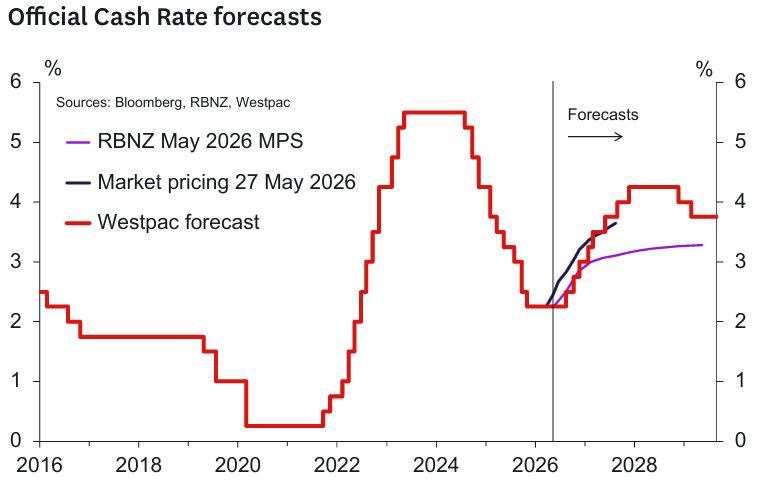

RBNZ

RBNZ meeting was hawkish as they signaled 3 hikes by the end of the year despite a weaker growth outlook and downside risks. Westpac expects hikes in September, October and December with the OCR ultimately reaching 4.25% with risks of the RBNZ falling further behind the inflation curve.

Subscribe to stay in the loop, if you haven't already. Premium members also get real-time reactive analysis, opportunistic trade ideas, via our highly active Discord server.

Later this year, we’ll launch our MacroTechnicals course, covering both macro and technical frameworks we use across swing and day trading the market, as well as aiding management of our stock portfolios. Existing Premium members will receive it for free, so take advantage now to lock in access before it launches as a much higher-priced standalone product.

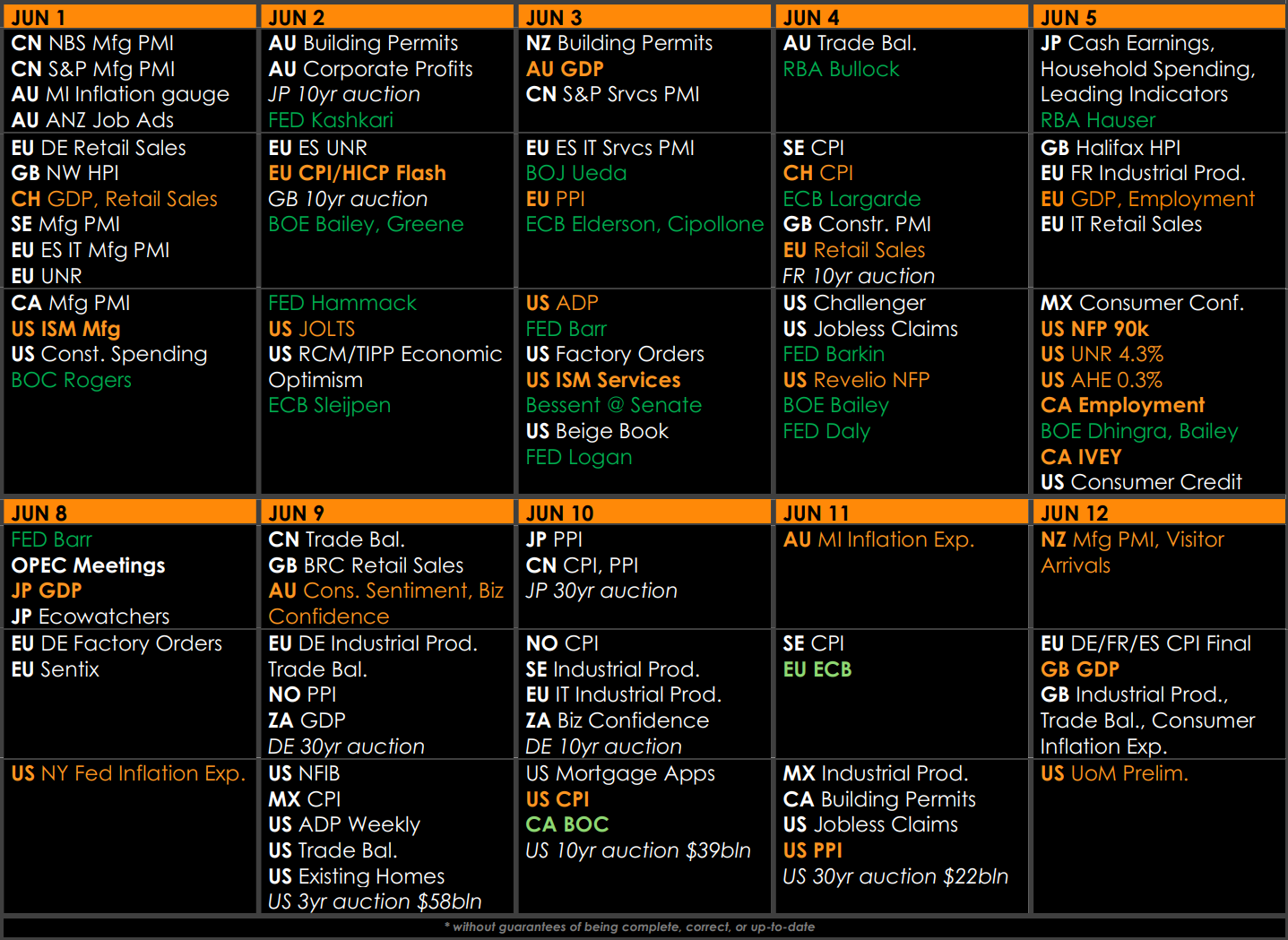

LOOKING AHEAD

Macro focus this week:

- AU GDP - looking out for slowdown risks developing

- EU inflation - whether it affirms aggressive rate hiking expectations ahead of ECB in the following week

- US ISMs and NFP - will it further shift the Fed in a hawkish direction?

- CA Employment and IVEY - soft data would add recession risks

- UK data and BOE - soft UK data would soften up rate hiking expectations, and looking out for dovish tones from the BOE to flag growth concerns with policy rate already at a high starting point.