Wk21 MacroTechnicals - Bloody Car Crash

Risk backdrop has shifted. Fed hike now priced by mid-2027, yields and dollar are moving higher, EMFX and metals started to crack, and equities are literally hanging by a thread of AI leadership

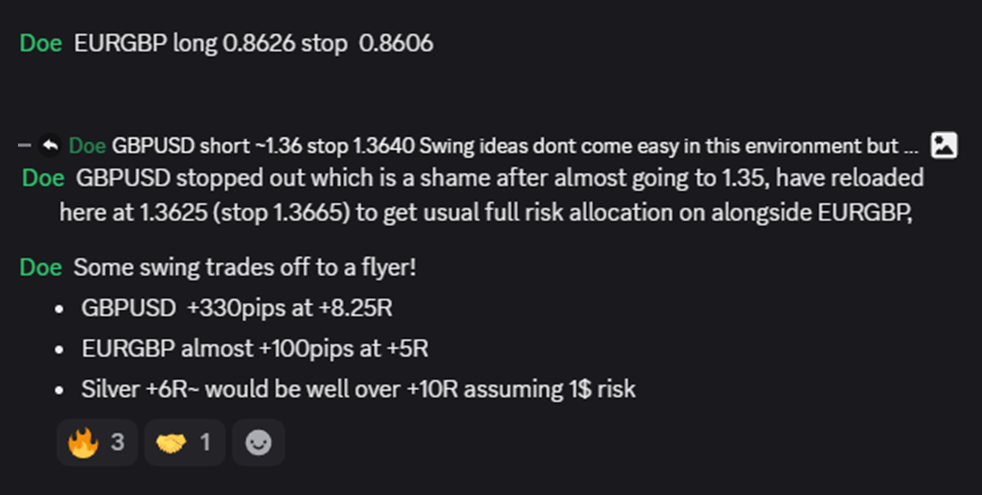

I want to start by briefly offering a preview of our Discord to non-premium subscribers. We've recently split the trading channels into two, one for day-trades and one for swing-trades, making trade idea discussions organised and easy to follow.

Nassy has seen some nice swings, as opposed to its big gaps followed by slow grinds, as we've taken advantage of in the day-trades channel.

We nailed Silver right at the peak of the rally, and the dip on Crude; a nice call on Gold levels which I lacked the conviction to take.

The first set of swing trades I've recommended in the new channel have also been a hit. I'm really excited about this channel and wonder why I haven't made separate channels like this sooner!

Already a close-knit and highly engaging group, it's genuinely fun to be in a community with people who share the same passion. If you're interested in joining us in the Discord, do consider becoming a premium member.

This, all of it,

is the scene of the bloody car crash,

minutes before it happens.

- Michael Burry, May 10th Substack

That line from Michael Burry has been sitting with me. Yes, I know the obvious criticism: Burry calls a lot of crashes, and most of them do not happen. But sometimes the value is not in treating every warning as a precise market-timing signal, but rather the value being in asking whether the market is becoming too comfortable ignoring a risk that is becoming increasingly obvious.

That is where I think we are now.

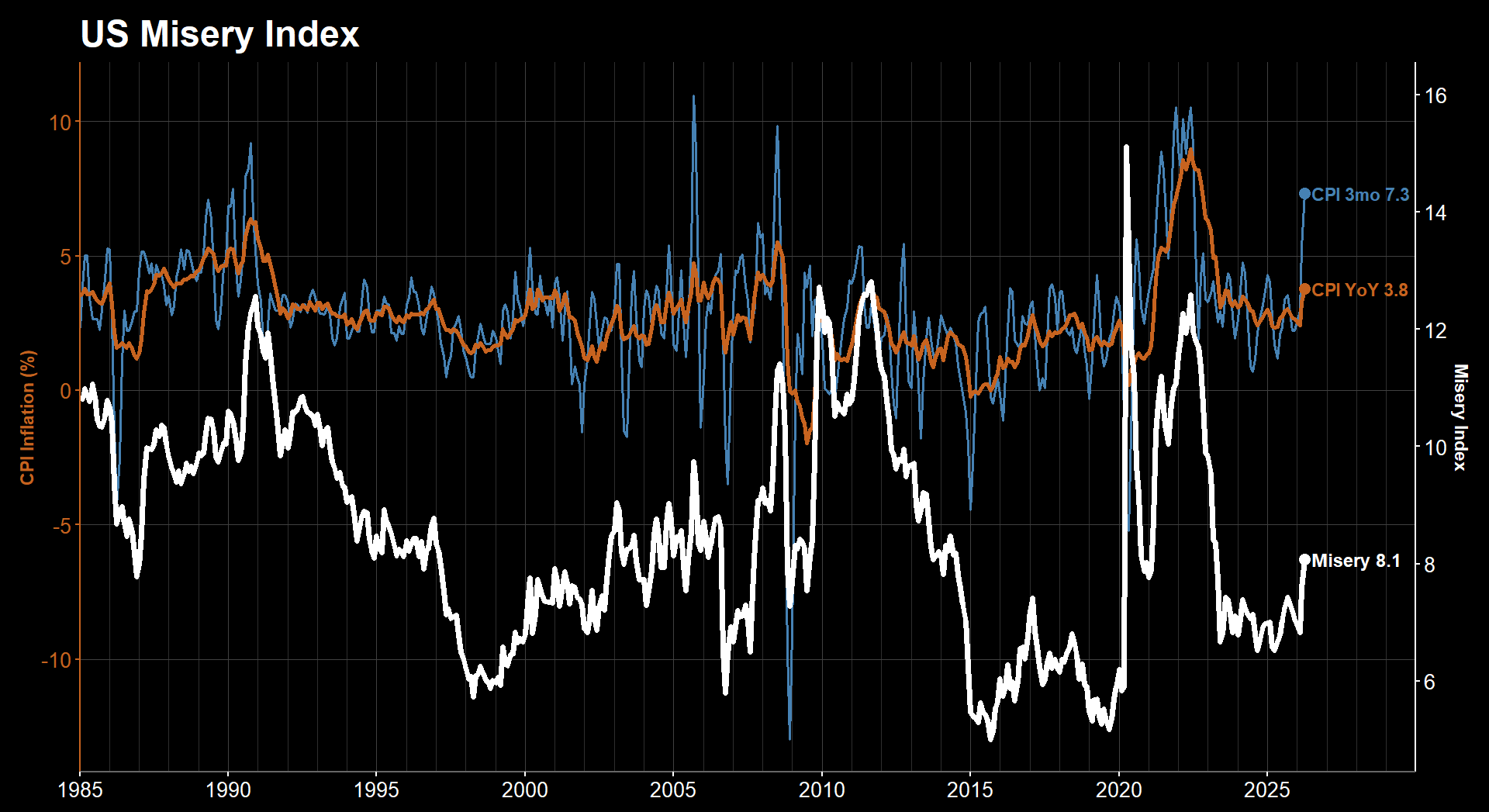

Over the past week, we have seen a combination of inflation data, business surveys, consumer indicators, rates repricing, equity breadth deterioration, and volatility complacency that all point in the same direction. The leading indicators are beginning to warn that the lagging data — employment, spending, growth, and inflation — may not remain as benign as the market is still priced for.

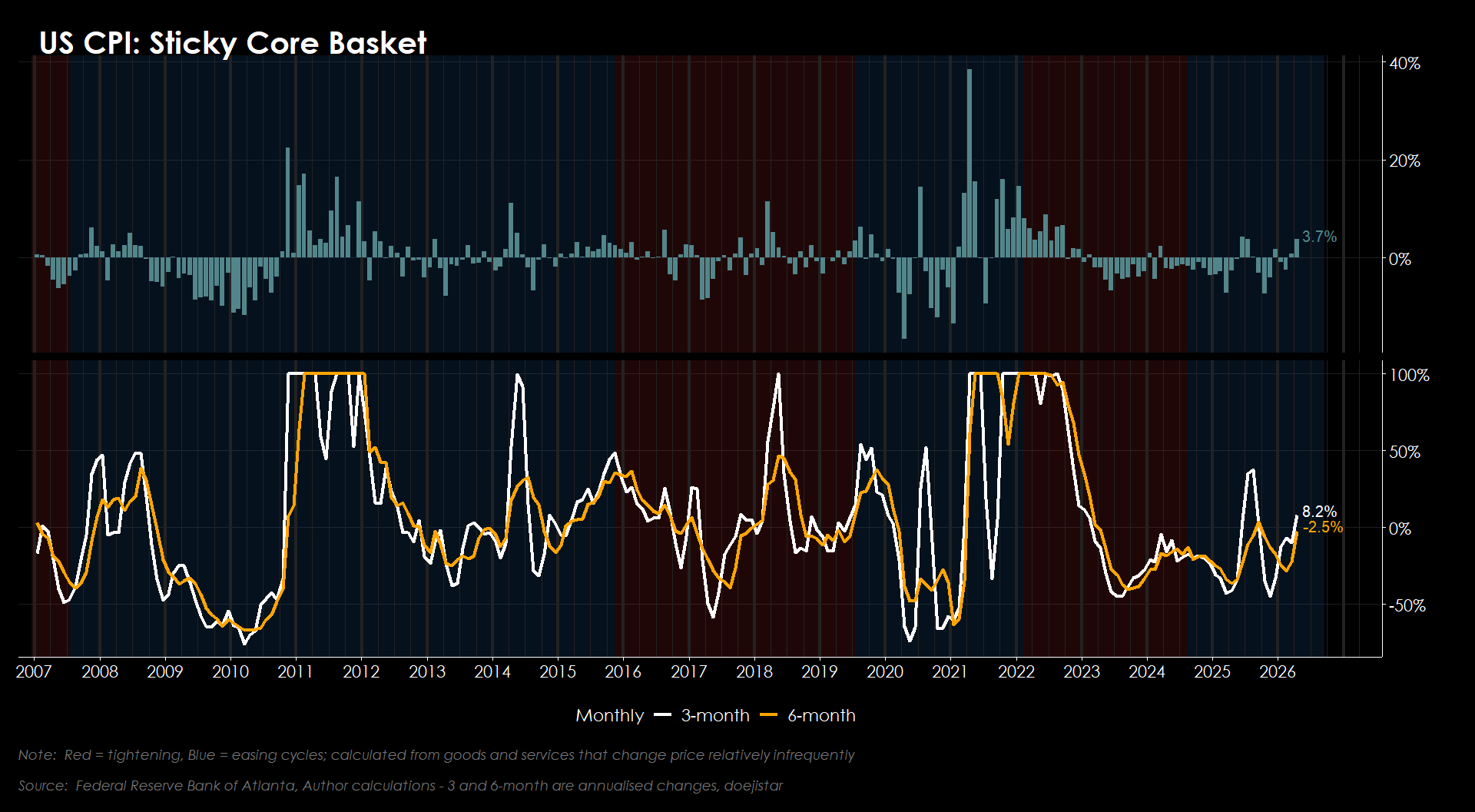

Inflation is accelerating rapidly, with the 3-month annualised CPI rate reaching 7.3%. Sticky CPI has also begun to accelerate sharply after a long period where many of its components had been relatively subdued. That matters because sticky inflation measures are designed to capture prices that change less frequently and are therefore more likely to reflect a broader and more persistent inflation impulse. In other words, this is no longer just an energy story.

At the same time, financial conditions may be entering a tightening cycle. That is a major shift. The cutting narrative was a powerful tailwind for the bull market, so it seems reasonable to ask whether the opposite should now begin to matter. Yet the market’s attention remains overwhelmingly focused on AI and semis. To be fair, that leadership has been powerful enough to keep the index supported, and it remains the key risk to the bearish thesis. But there are moments when one theme, however strong, cannot indefinitely offset a broad macro impulse that affects rates, the dollar, inflation expectations, real yields, earnings multiples, and risk appetite across the entire market.

This is also happening at a time when equity markets are showing signs of complacency. Skew, put/call ratios, implied correlation, and other downside-hedging indicators have returned to levels that resemble the start of the year, almost as if nothing has changed. But a lot has changed. The macro backdrop is more inflationary, the rates market has become more hawkish, the dollar is strengthening, term premium is making new cycle highs, and breadth beneath the surface of the indices has continued to deteriorate.

So the question for this week’s note is simple: does the market’s current pricing still square with the economic and cross-asset evidence in front of us?

My concern is that it does not. And while that does not mean the crash is guaranteed, it does mean the scene is starting to look uncomfortably familiar, as it does to Michael Burry.