Wk25 MacroTechnicals - Sticky Landing

Deal-on Risk-on is back, yields lower, but don't think the market will be Warshing away hiking risks too soon

This week I share the Macro section publicly in full as I'd like to offer my thoughts on the mispriced STIR (short-term interest rate) discussions. I'm also going to avoid the geopolitics in this note since the newsflow is pointing in the direction of 'progress', however meaningless or believable that is - it's the direction that matters and that is what drives my strategy views regardless of what I think or have previously gamed out.

In the Technicals section we cover how our framework shapes up against the charts and what our new strategy views are based on that process. This section is reserved for premium members however. If you're not a premium member and would like to see those plans in action, as well as stay on top of what's driving the market in real-time, consider upgrading to Premium and join us in the discord.

Macro

INFLATION & MISPRICINGS

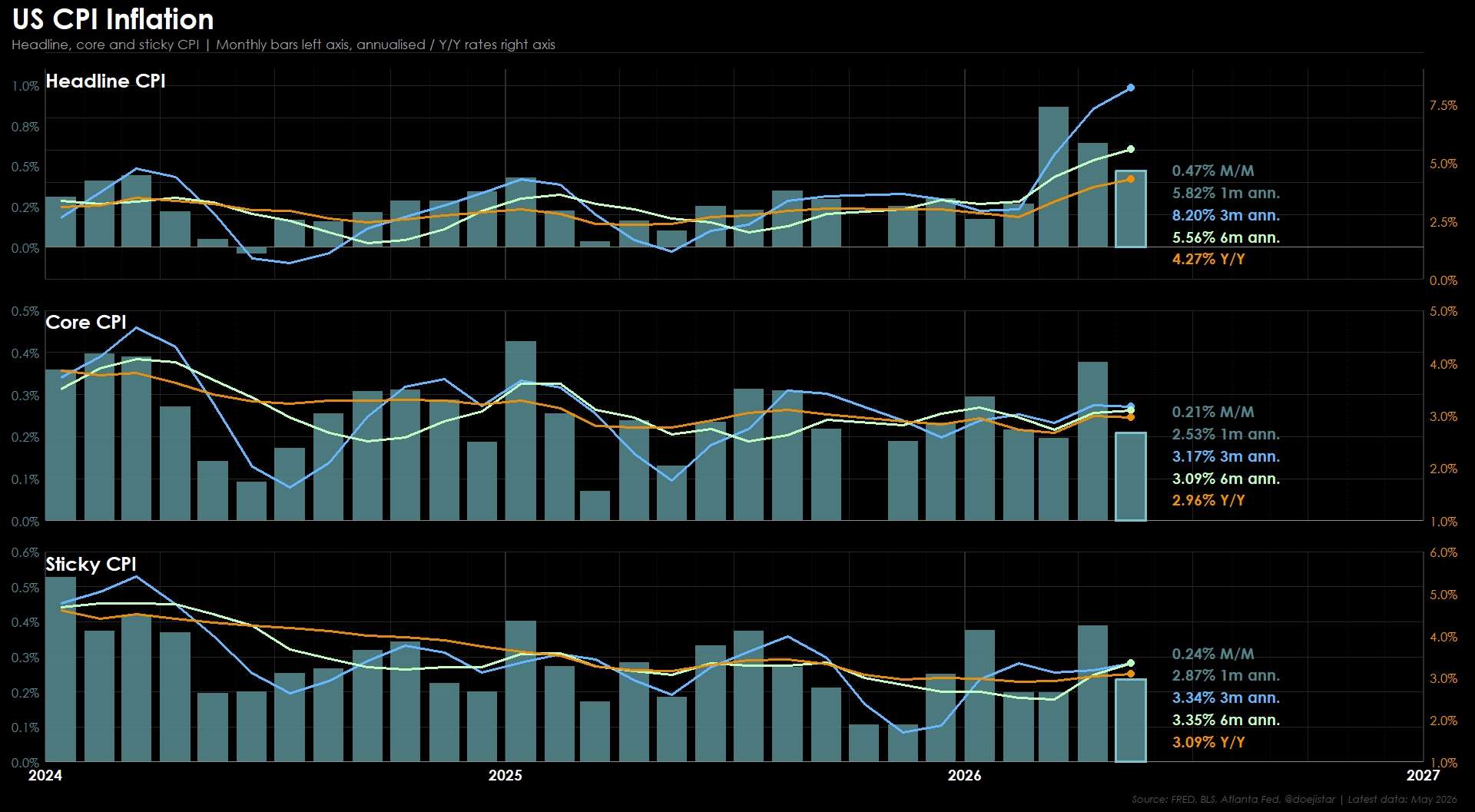

There is much discussion on the energy-led inflation shock being transitory, and thus the market is mispricing policy expectations. But what the discussion lacks, in my view, is how sticky inflation could prove to be given how energy markets will be tight over the medium term, as well as the massive AI investment boom underpinning a very resilient economy. Let's review the inflation data - May CPI was on the soft side with Headline printing 0.47% (vs 0.5% expected) and Core was 0.21% (versus 0.3% expected).

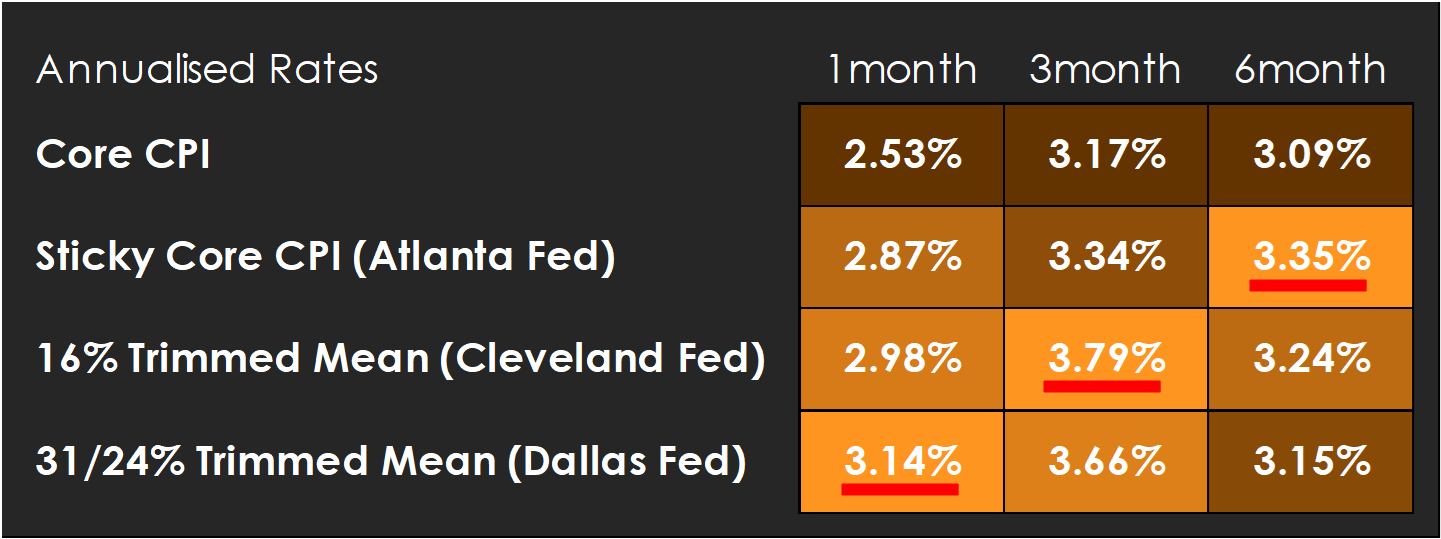

Despite some cooling, the longer-term rates are elevated with trends pointing upwards - so it will require a few more softer prints before the market can start to feel comfortable about policy expectations normalising from the currently mild hiking bias. What I find particularly interesting in the meantime is that the Atlanta Fed's Sticky Core CPI as well as the Trimmed Mean CPI measures are all running hotter than the main Core. The often discussed Dallas Fed version, which eliminates more of the strongest inflation readings and less of the weakest (in an attempt to get a "truer" read on underlying inflation) was the strongest in May.

Ironically, these alternative measures were thought to buy Kevin Warsh time by helping his case to argue against elevated inflation not being reflected in these 'underlying inflation' measures. Barely into his new tenure as chairman and his plans of looking at inflation differently has already backfired.

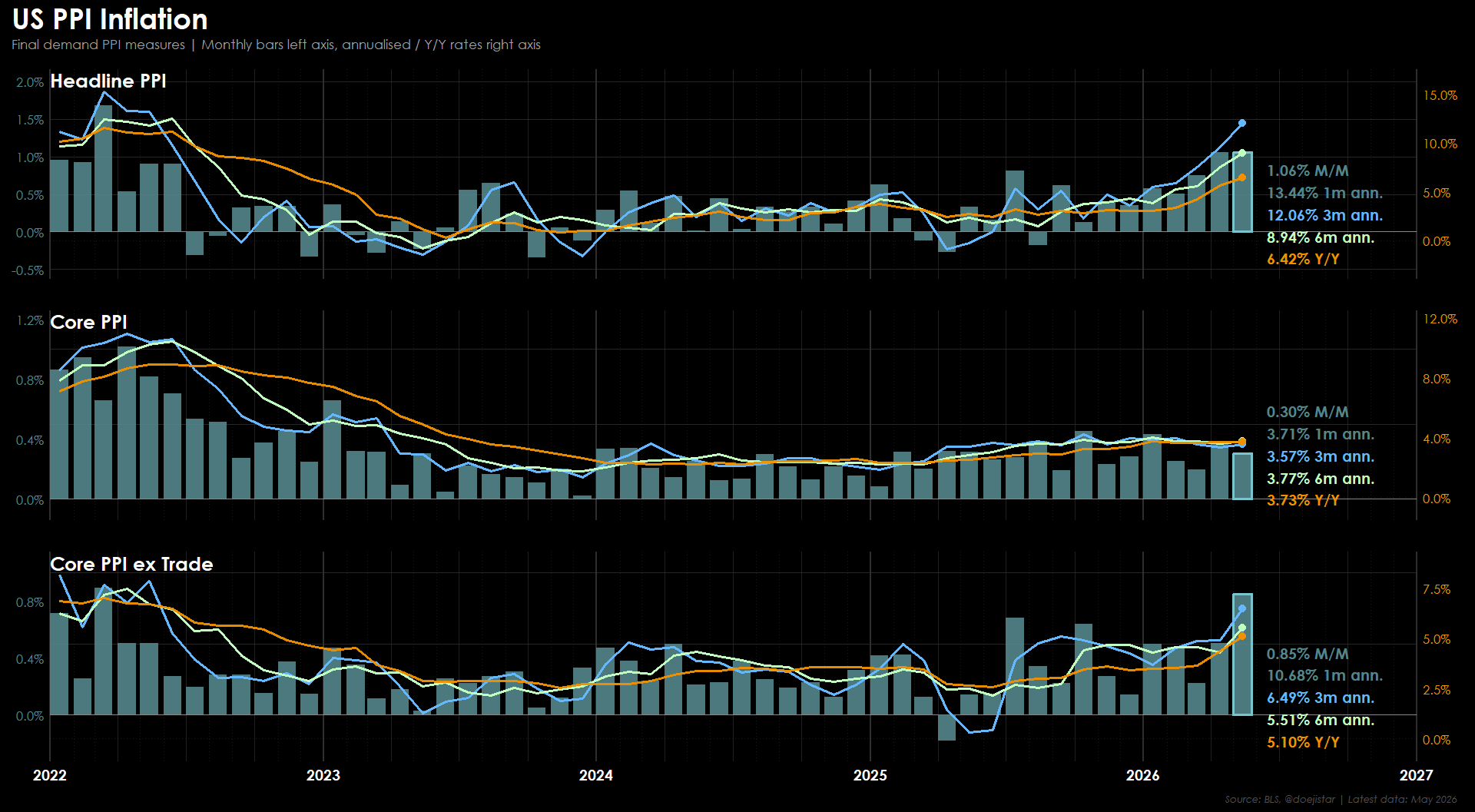

Another point to challenge the transitory inflation argument is the rapid inflation at the wholesale/producer level. Headline and the Supercore (ex Trade) PPI are seeing the fastest increases since the last energy shock of 2022.

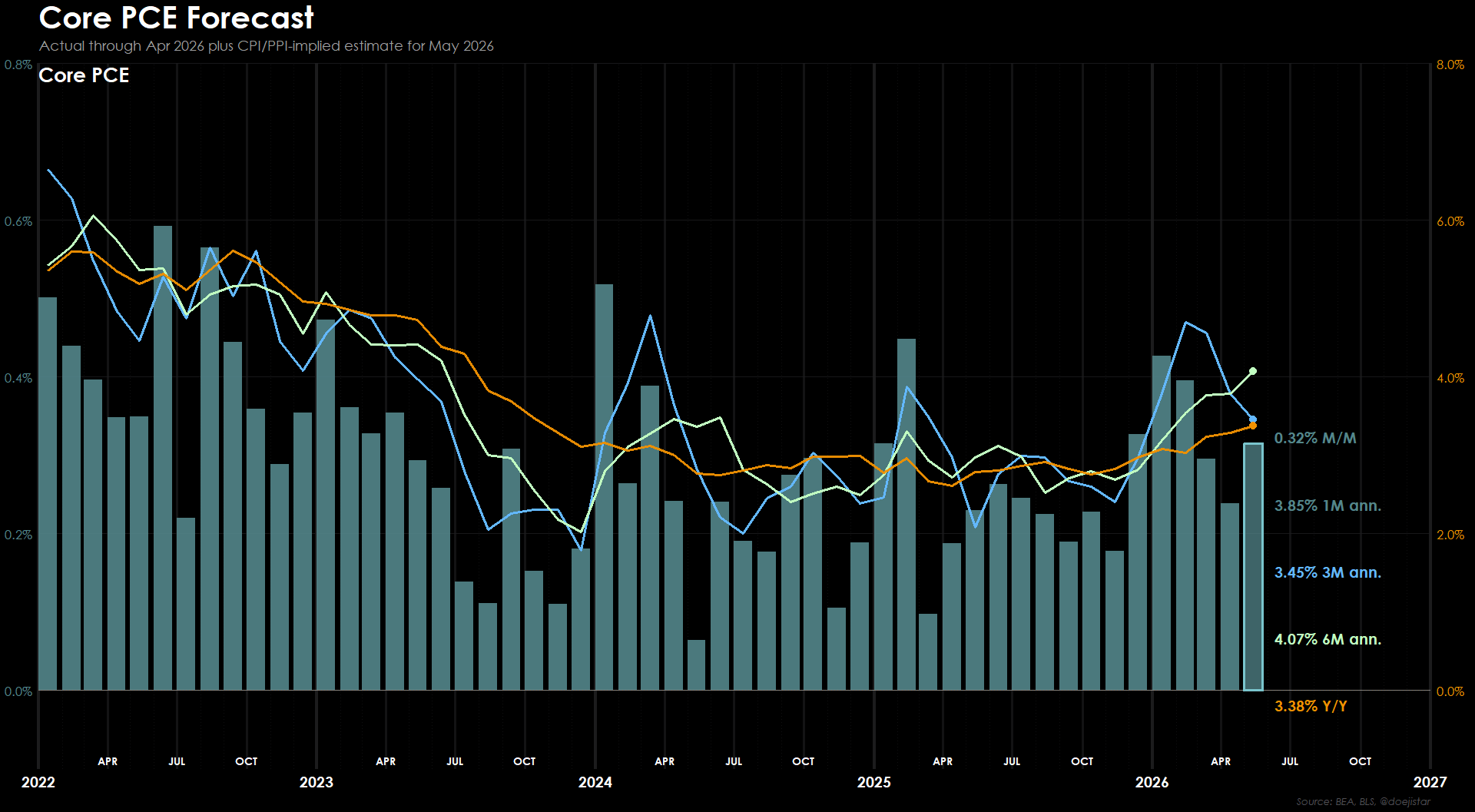

To return to the more comfortable 3% Core PCE levels, we would need to see monthly readings to average 0.25%. But even before energy prices spiked in March, it was averaging around 0.3% if not greater. Modelling Core PCE from both CPI and PPI reports, it is expected to be 0.32%, and 6-month annualised and YoY rates would see new cycle highs and the highest levels in over 3-years.

The key question is whether these significant cost pressures in reports such as these and PMIs will be passed on to consumers, and whether the economy is able to absorb these higher cost pressures or not on the whole. These considerations are what I think that the 'transitory-inflation and hike mispricing' discussions were lacking. Companies and households alike have expressed plenty of cost concerns but thus far - consumer spending (at the headline-level, ignoring the k-shaped perspectives for the broader argument), services activity, manufacturing production, jobs growth - all holding up relatively well. All in all, these are not signs of an economy slowing meaningfully enough to offset higher cost inflation. Add AI capex investment on a scale comparable with major historical economic booms, and I find it difficult to argue that these cost pressures will not be absorbed and supported by the economy over time. This is the reason I see a stickier inflation outlook than many rates mispricing comments would suggest and would therefore deem the slight hiking bias in the forward rates curve being fair.

THIS IS FINE...

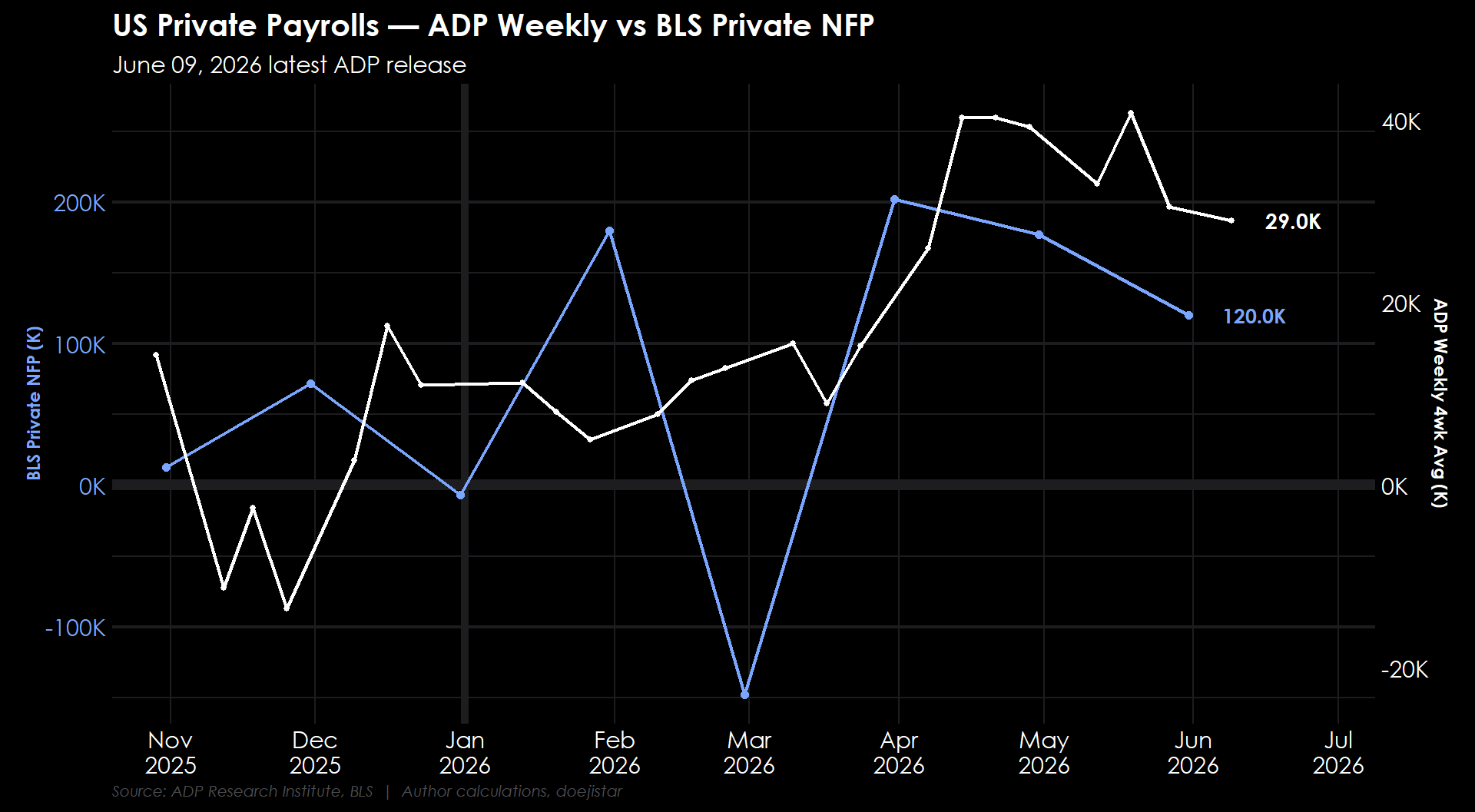

Let's review some other data points, starting with payrolls. We've seen a slight slowing in private payrolls but the year-to-date on a cumulative basis looks 'fine'. Nothing to write home about, but certainly not a weak picture.

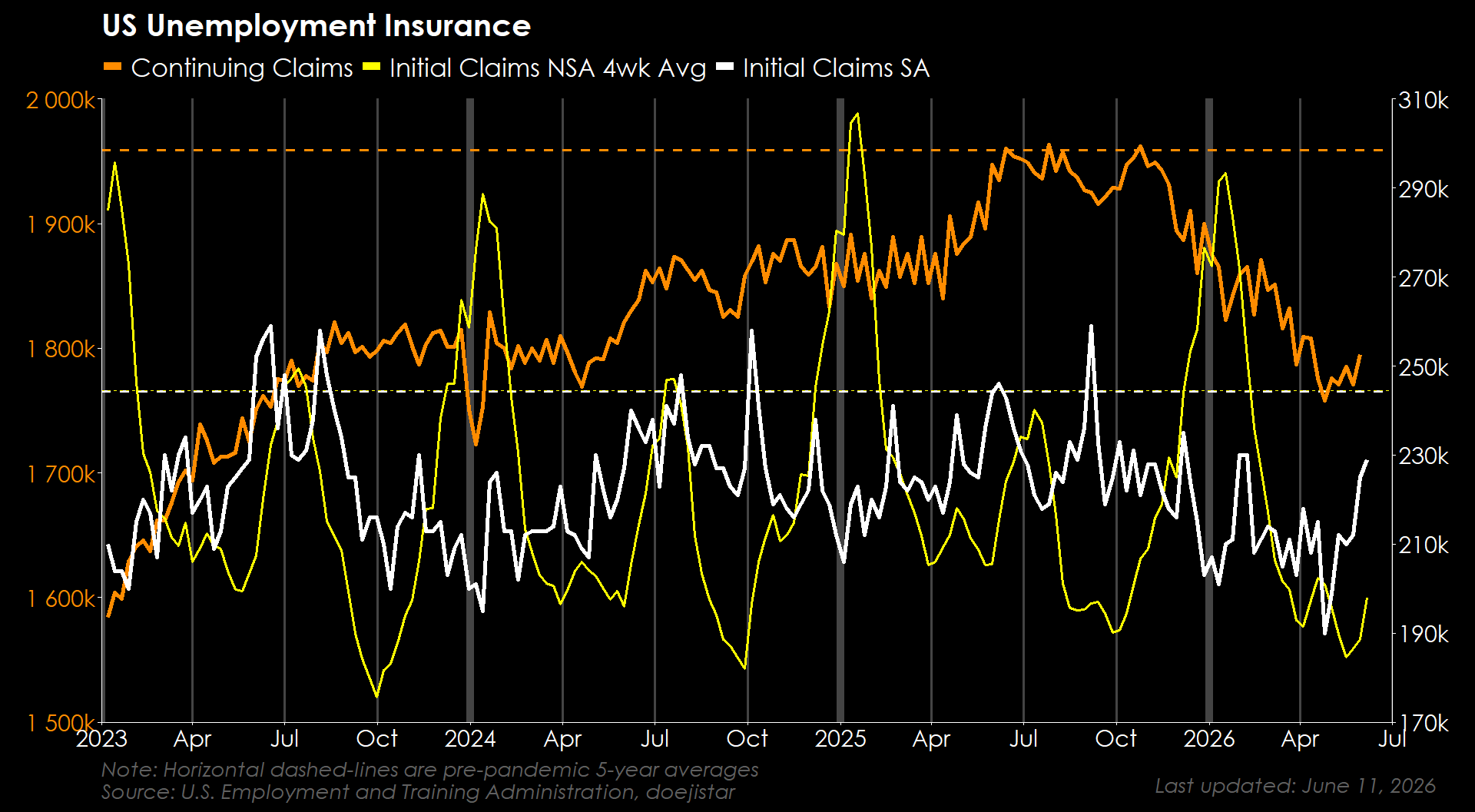

Unemployment claims are rebounding but it looks to be seasonal residuals for the most part and not really flagging anything in the grand scheme. 'Fine'.

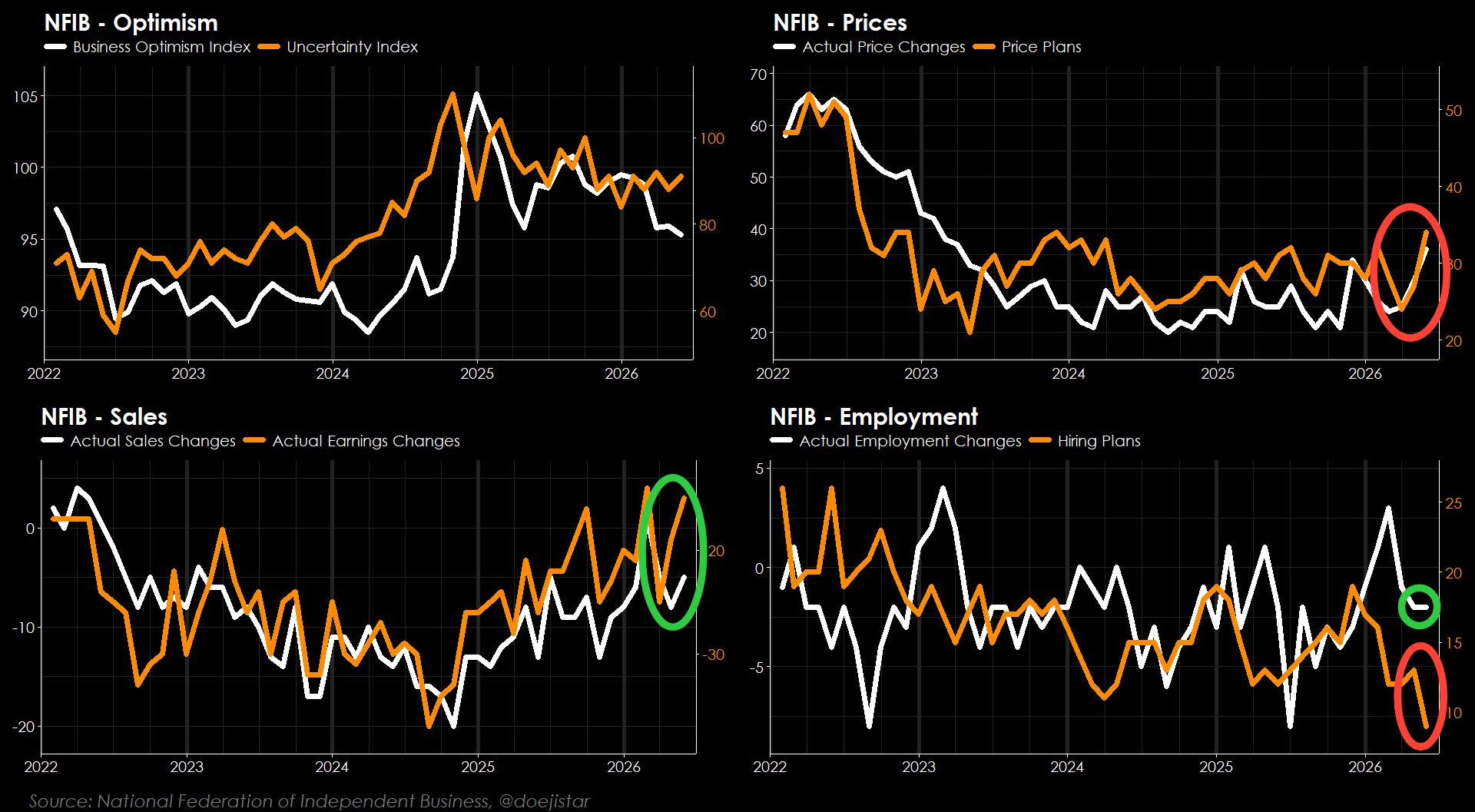

NFIB showed stagflationary details with Price Changes and Plans to increase prices rebounding strongly while Hiring plans plummeted to pandemic-levels (May of 2020). Seeing that Sales and Earnings have rebounded, higher prices appear to be accepted by customers, while businesses appear to be cautious about expanding headcount even as the bottom-line is going up. 'This Is Fine'.

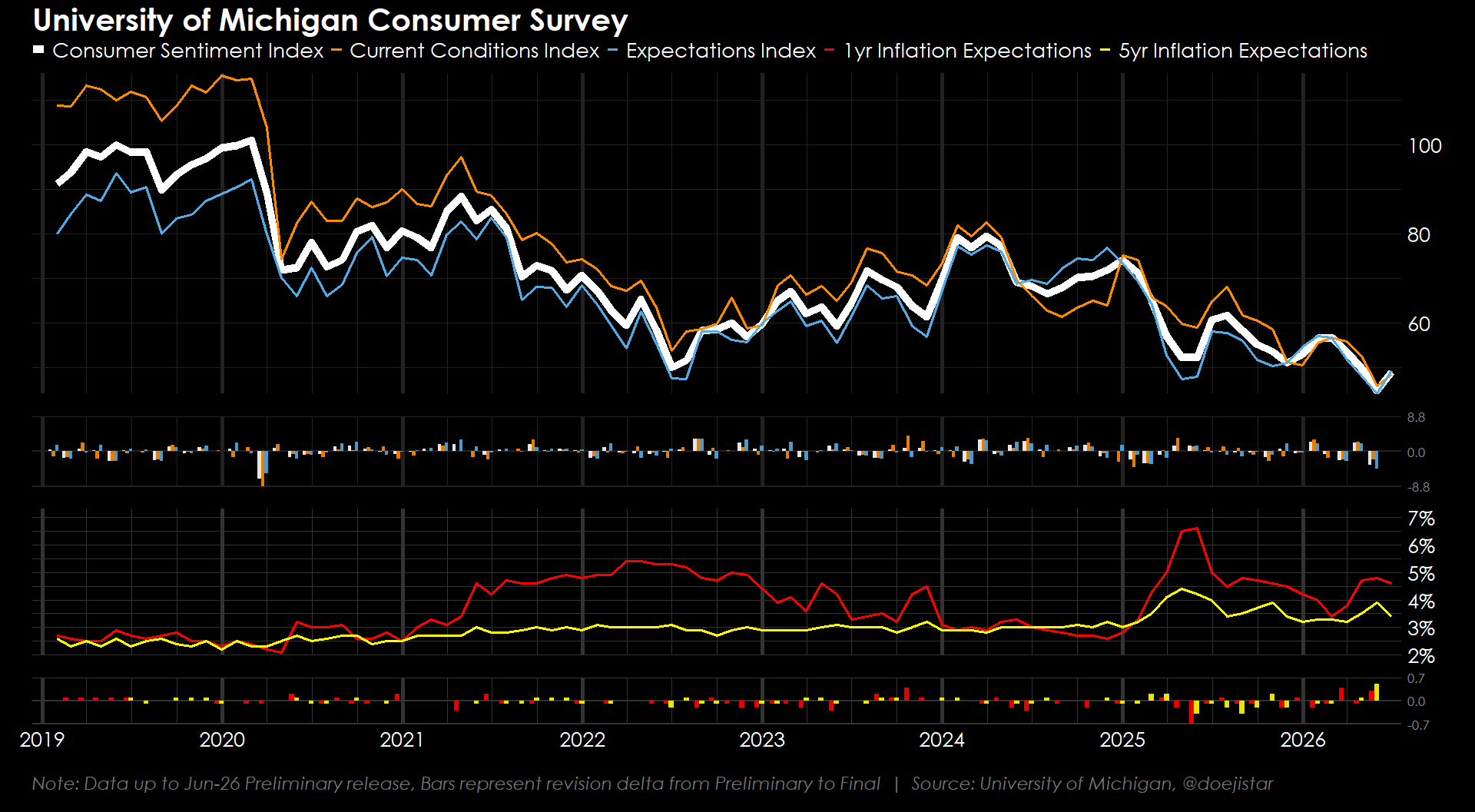

Consumer confidence, understandably, is extremely pessimistic given that it has never recovered from Trump's tariffs just over a year ago, and then the Iran war added to further pessimism with inflation on the rebound.

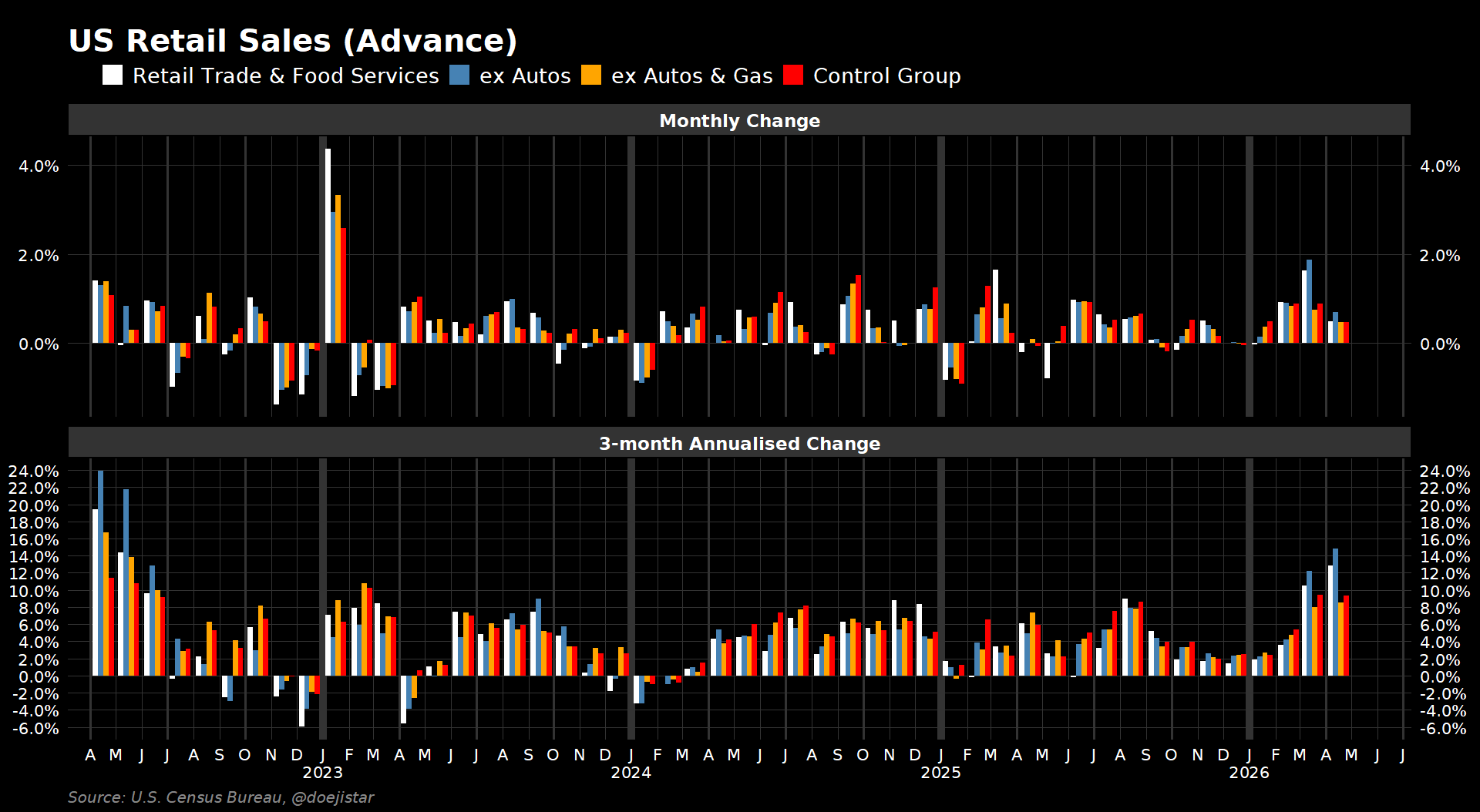

And yet, consumer spending proved resilient even as confidence/sentiment was treading lower. We will be on watch to see if that story continues into the May numbers on Wednesday, but the broader story is that spending has not been materially dented during the oil spike, and I think that's important to keep in mind. Again, 'Fine'.

LOOKING AHEAD

Although there is plenty to digest from the economic calendar this week, I will preface this with my view that it will be deal-sentiment driving markets this week, so I wouldn't read too much into individual events and would rather look at them as short-term opportunities to take a trade in the prevailing direction.

The main focus this week will be Wednesday’s US Retail Sales, followed by the FOMC later that day marking Kevin Warsh’s first appearance as Fed Chair. Beyond that, UK and Canadian Retail Sales is released on Friday, the same day that Trump said the deal would be signed - could make for some interesting sentiment-turn trade setups.