Wk15 MacroTechnicals - Dead Cat Bounce

Durable bottom or just a dead-cat bounce?

This week, I'm focused on the recent optimism displayed by last week's price action, but first, I'll share a little about my rather relaxing trip to Jeju Island, a large volcanic island off Korea's southern tip.

Breathtaking views and delicious food. Jeju is renowned for its stunning lava-formed coastlines, rock structures, valleys and caves, as well as fresh seafood, quality spring water, fruit, and pork from natively reared black pigs.

Cherry blossoms also adorn the streets, pathways, and roadsides in full, vibrant bloom in Jeju and all over Korea. It's only for a 2-3 week stretch before they start shedding which is stunning in itself, but it really is the best time to take in the scenes in Korea, if you ever want to visit.

Macro

BUSINESSES

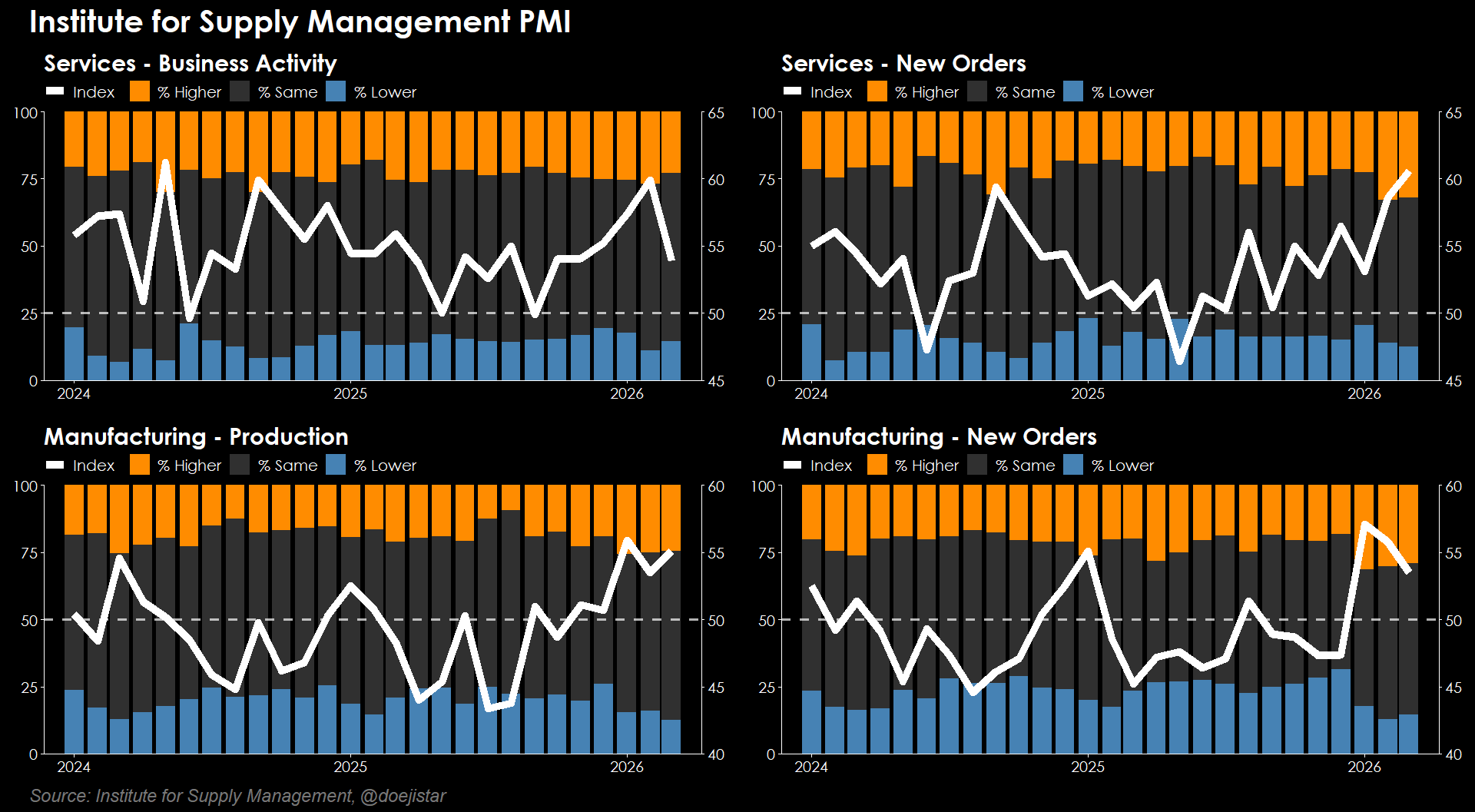

ISM reports for March showed a larger-than-expected decline in Services from 56.1 to 54.0 driven by the drop in Business Activity, while the Manufacturing index edged higher and slightly beat expectations.

New Orders point to resilient business outlooks - Services reached the highest level in 3-years and Manufacturing stayed firm though decelerating for a 2nd month.

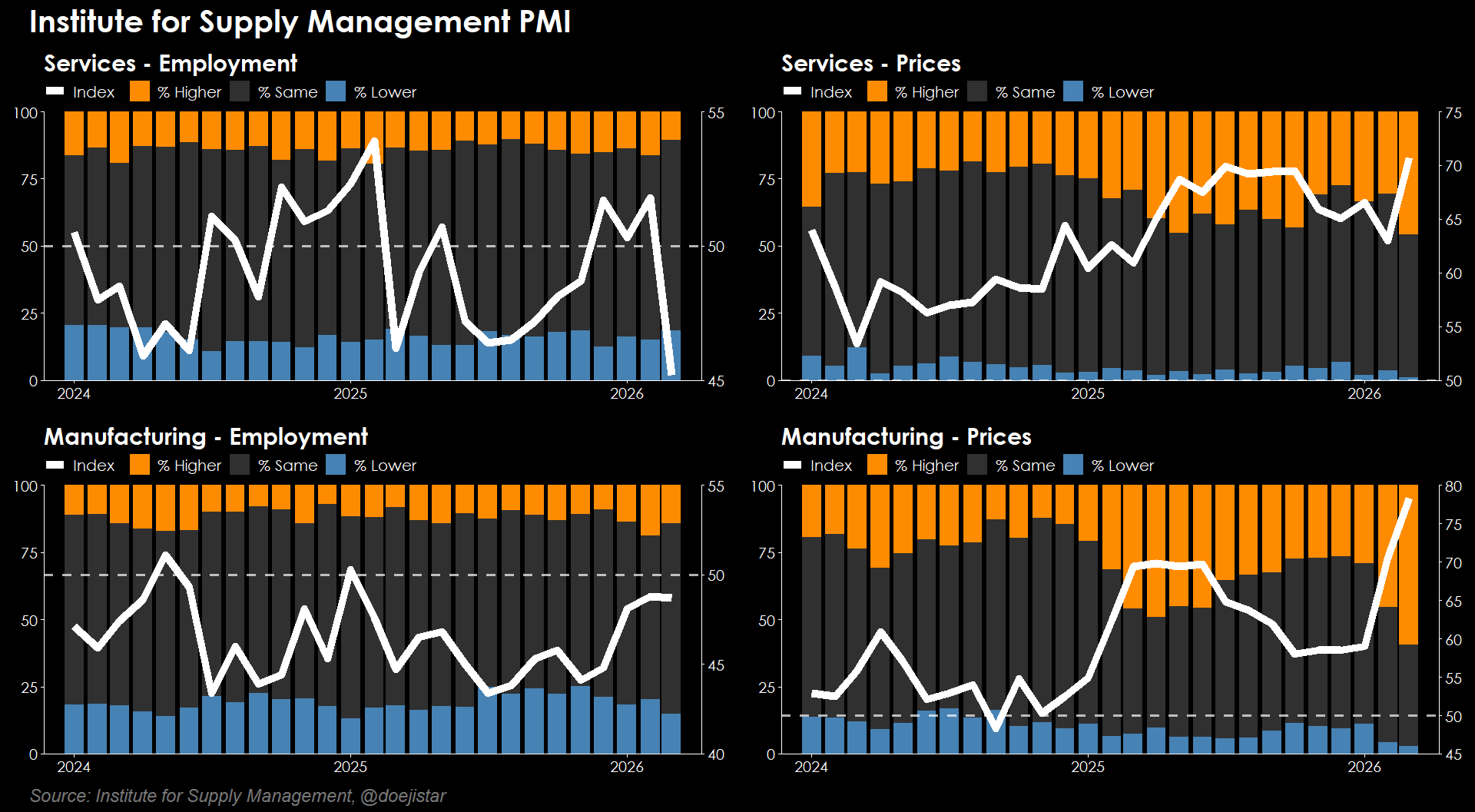

Despite the headline resilience, the most important components - Employment and Prices paid, are already showing strong cause for concern. Employment index for Services is the lowest since December of 2023 and the recovery in Manufacturing has stalled short of reaching expansion. Prices paid for both Services and Manufacturing is the highest since the Ukraine invasion of 2022.

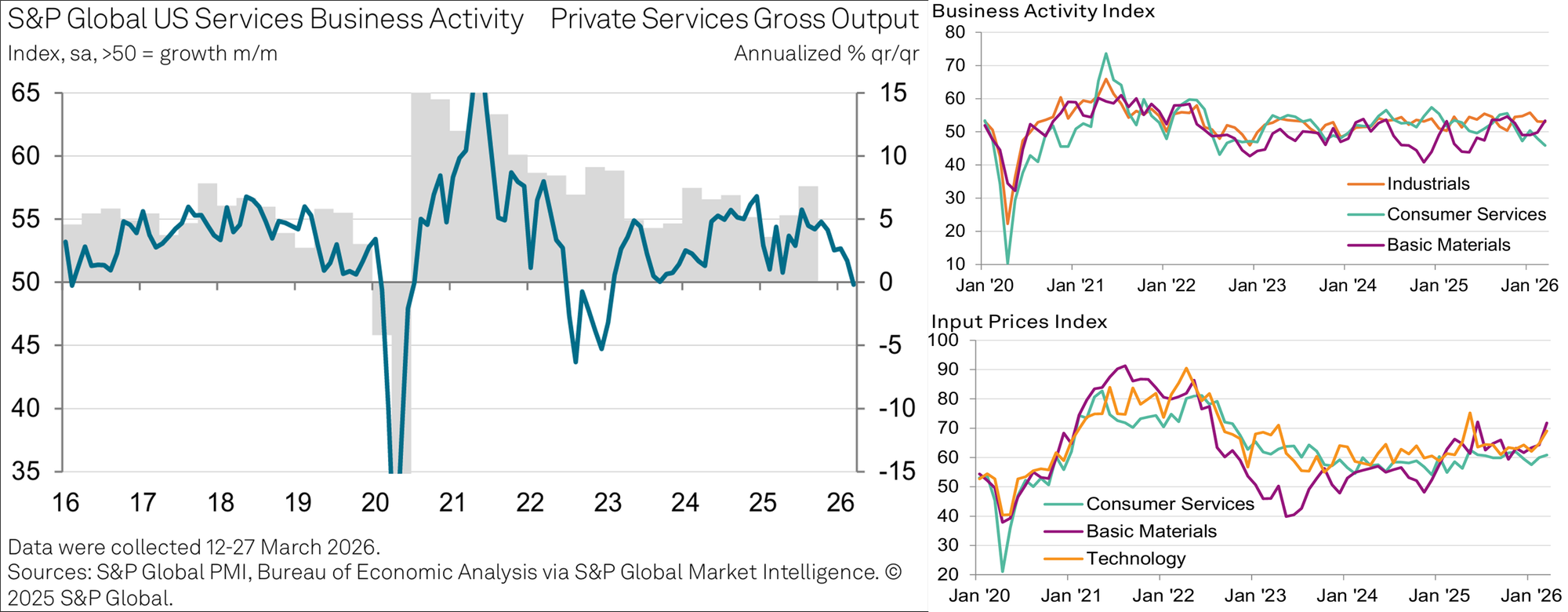

S&P Global's US PMI also highlighted stagflationary concerns with Services Activity dropping into decline for the first time since January of 2023, while both input and output prices accelerated in March.

CONSUMER

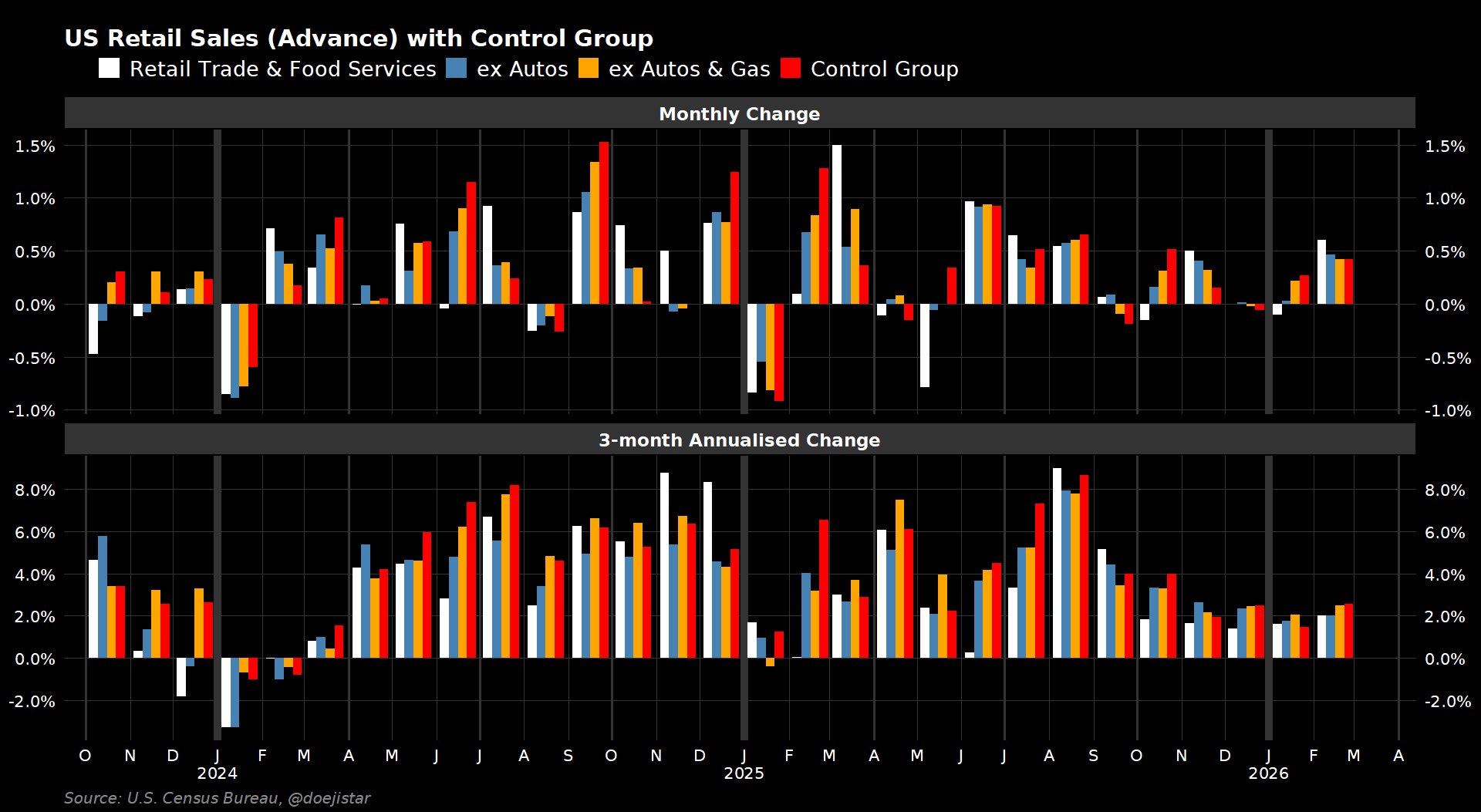

Retail Sales is saying that the consumer has been resilient through February with beats across headline, core and control group components.

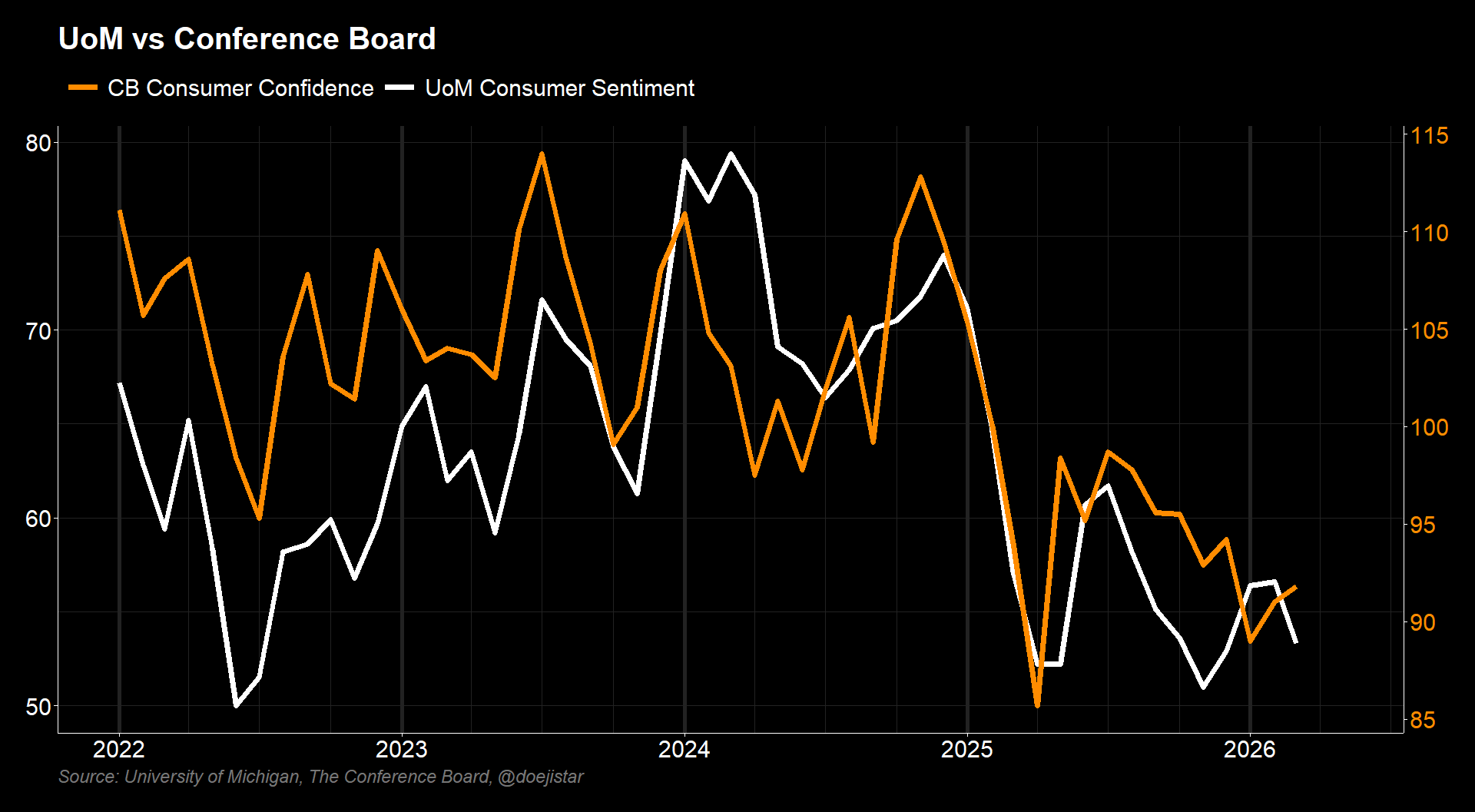

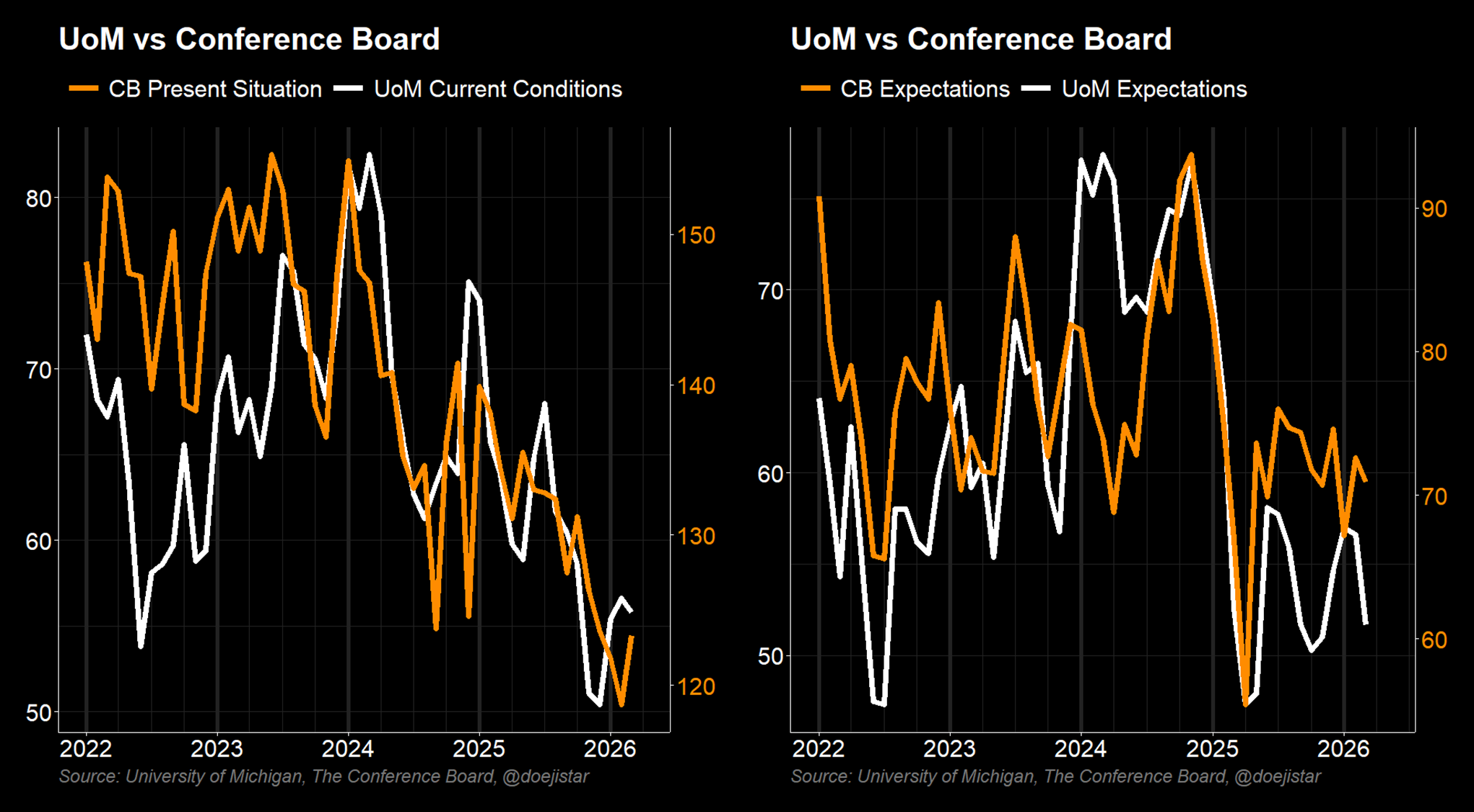

CB Consumer Confidence held up much better than expected but I would not at all be surprised if it gets revised down next month.

Headline resilience is masked by the greater rebound in the Present Situation index versus a very slight decline in future expectations. CB economist notes that consumers' write-in responses remained distinctly pessimistic.

Not visible in headline numbers is the rising tariff passthrough and the oil shocks with 1-year inflation and cost of living expectations moved higher and 1-year stock market expectations plunging.

While some resilience in consumer data from early tax refunds was expected, I would expect spending and confidence to get worse with the surge in fuel prices to start being reflected in the data.

LABOUR MARKET

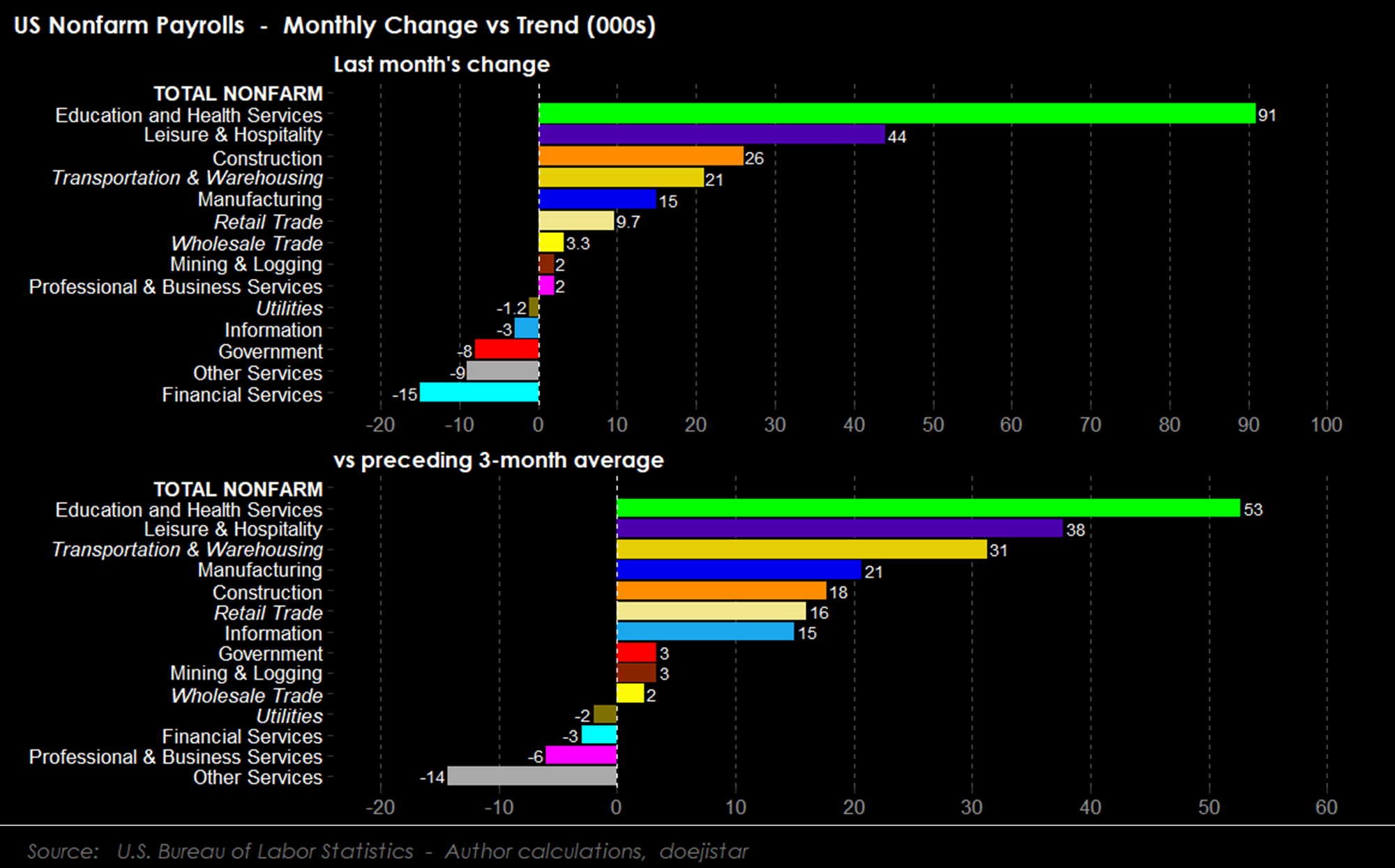

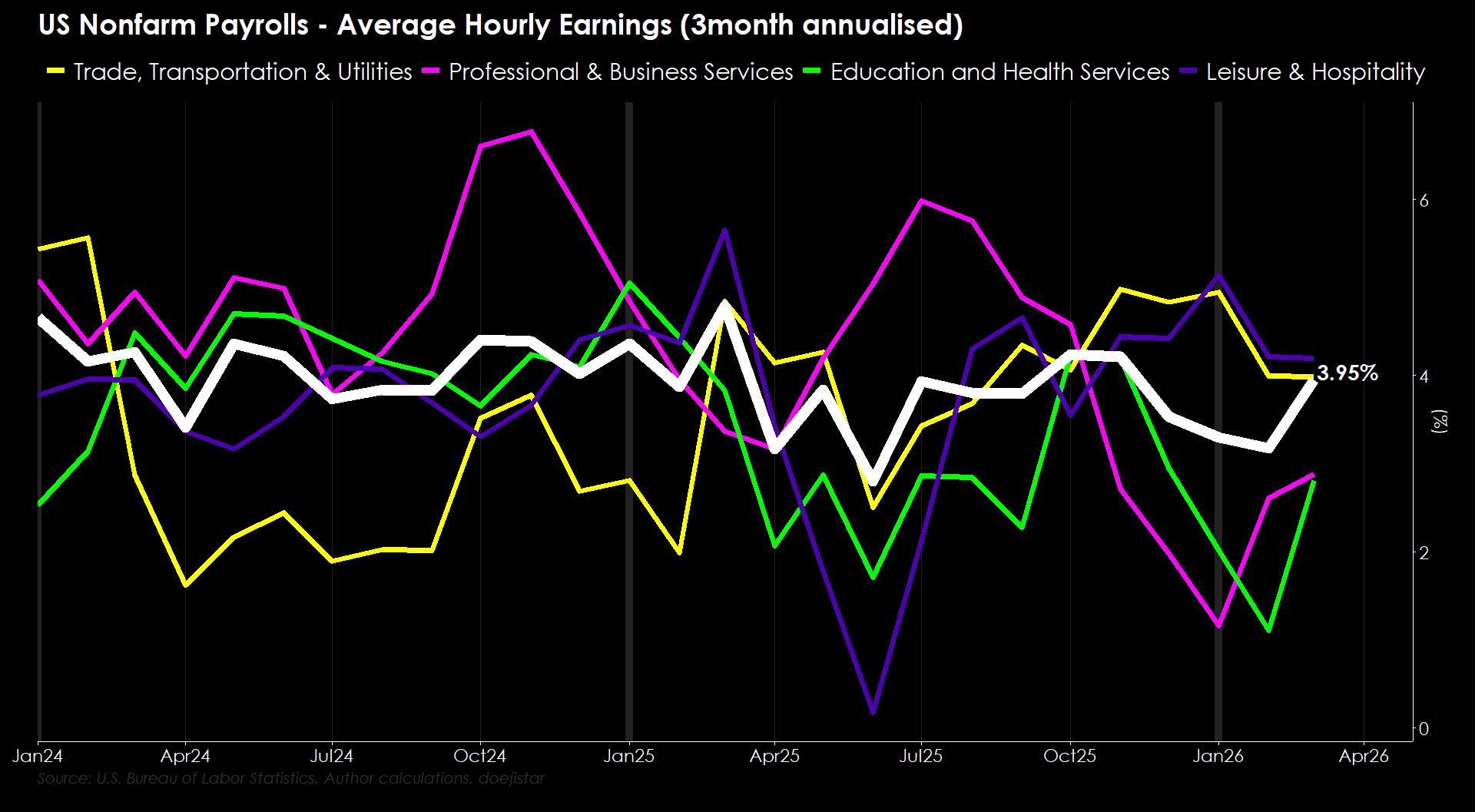

March NFP printed a whopping 175k beat versus 65k expected, but the revision to the prior month widened the deficit by 41k from -92k to -133k. The biggest contributions to overall job gains came from the Education & Health sector, Leisure & Hospitality, and Trade Transportation and Warehousing.

AHE was 0.2% (0.241% unrounded), missing expectations and below the prior month's 0.4% reading. The 3-month annualised reading however shows wage growth to have accelerated over the first few months of the year to 3.95%.

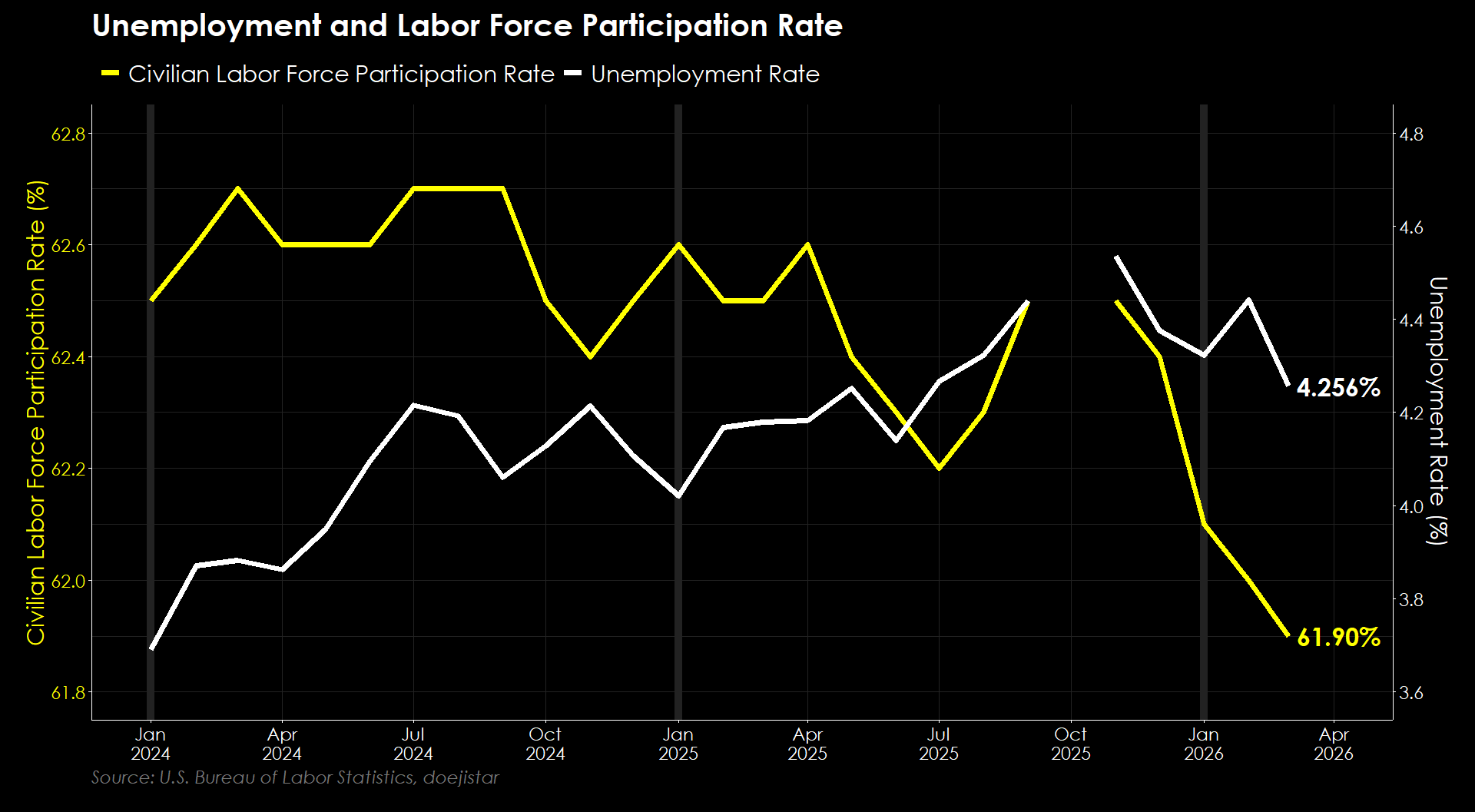

The unemployment rate unexpectedly dropped from 4.4% to 4.3% which appears to have been driven, at least in part, by a decline in labour force participation.

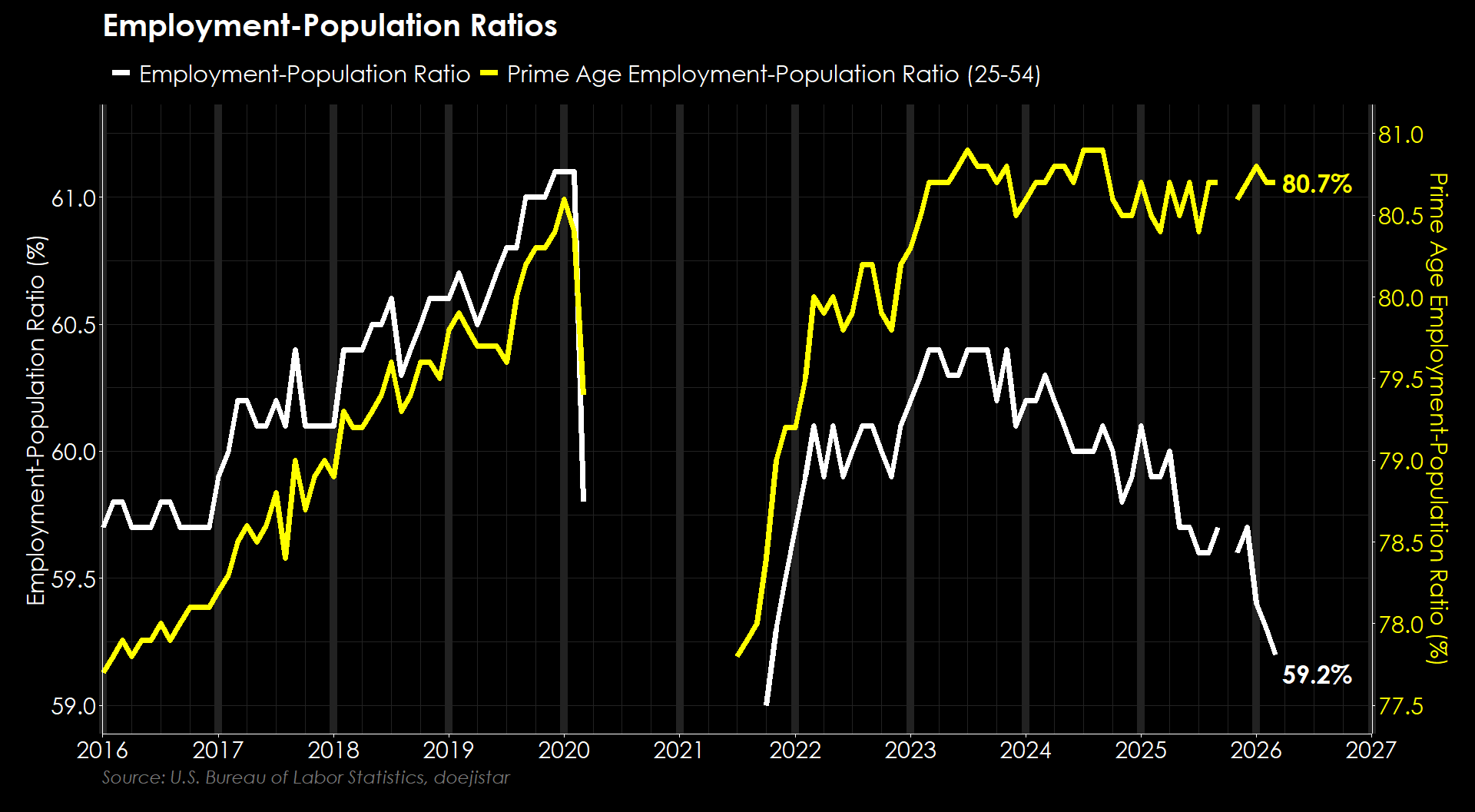

Looking at the Employment/Population ratio however, unemployment is still looking elevated overall despite prime-age employment holding firm.

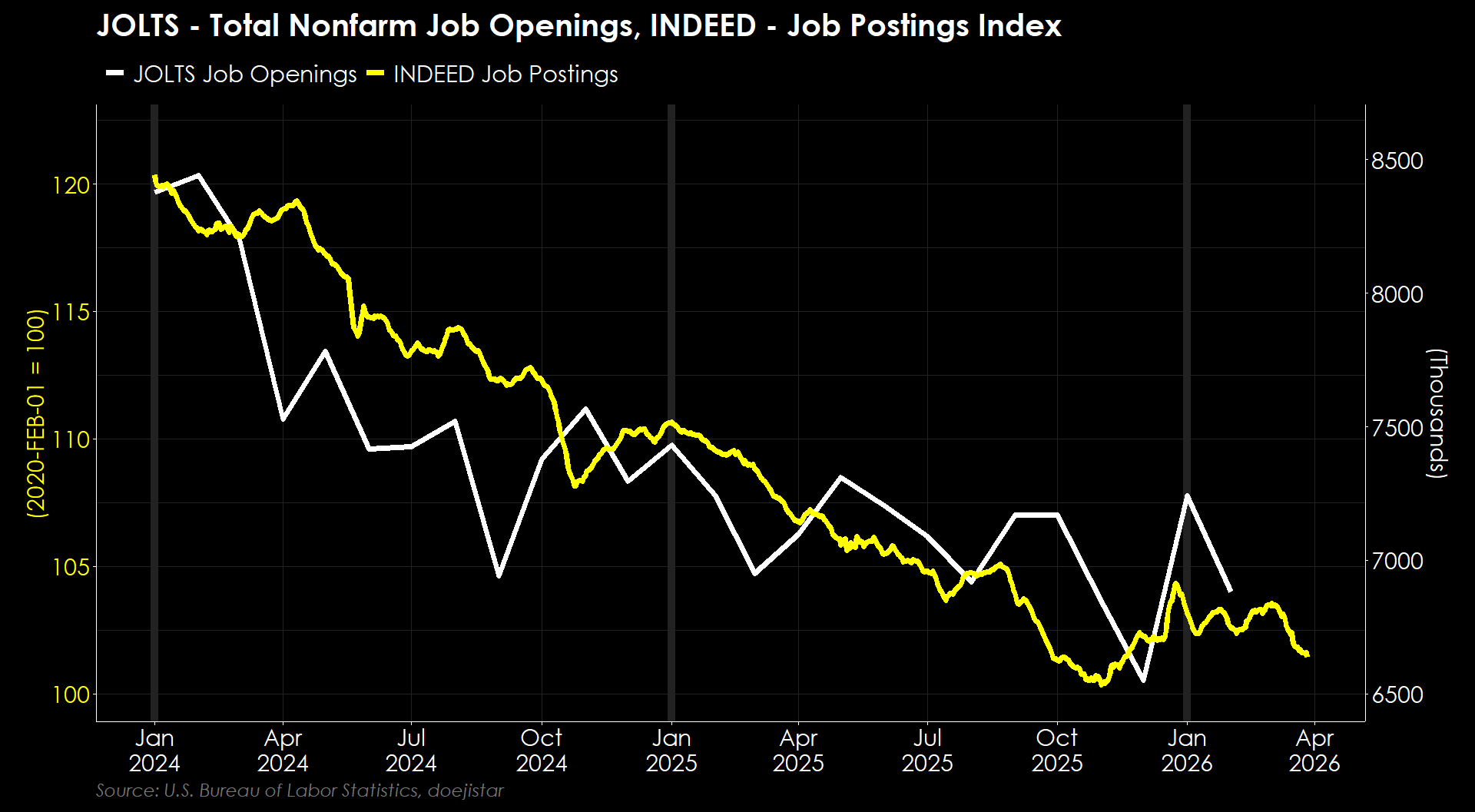

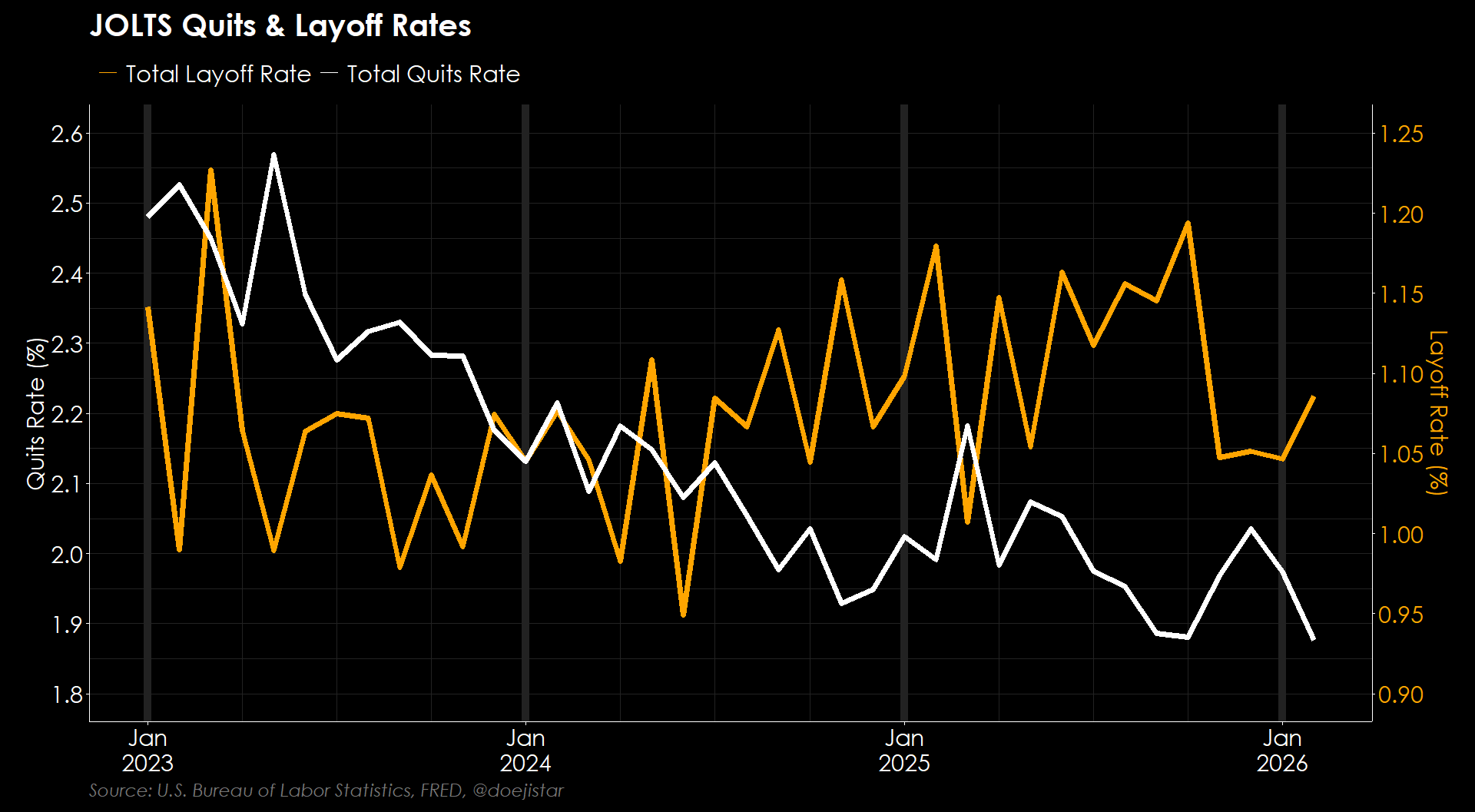

Latest JOLTS data also show signs that labour market demand remains weak, especially with the Indeed index at the lowest level so far this year, and Quits and Layoffs heading in a weaker direction.

The pickup in Layoffs while Quits have fallen continues to suggest weak demand and low confidence among workers to switch jobs voluntarily.

IRAN CONFLICT

We'll be watching yet another extended deadline for Iran to agree to US terms at 8pm EST today. While the situation remains highly fluid, the crux of the issues at hand is whether there has been any change in behaviour from either side that could change the calculus of our gamed-out scenarios.

Other than Trump attempting to give Iran more time to make a deal, and Iran allowing 'some' traffic through the Strait of Hormuz in an effort to gain sympathy, I suspect, there has been no significant change. I therefore still see the possibility of deviating from the scenarios that would lead to a lasting stable outcome to remain quite low, since Trump remains unyielding on his terms and Iran is not prepared to concede any more than their nuclear enrichment programme while also making counter-demands.

Technicals

Technicals for stocks are signalling a durable bottom, while there are plenty of geopolitical and macro questions without a resolution to the Iran conflict which I feel is a key part to determining where equity markets have put in a durable bottom, or whether it is simply a dead-cat bounce from deeply oversold conditions.

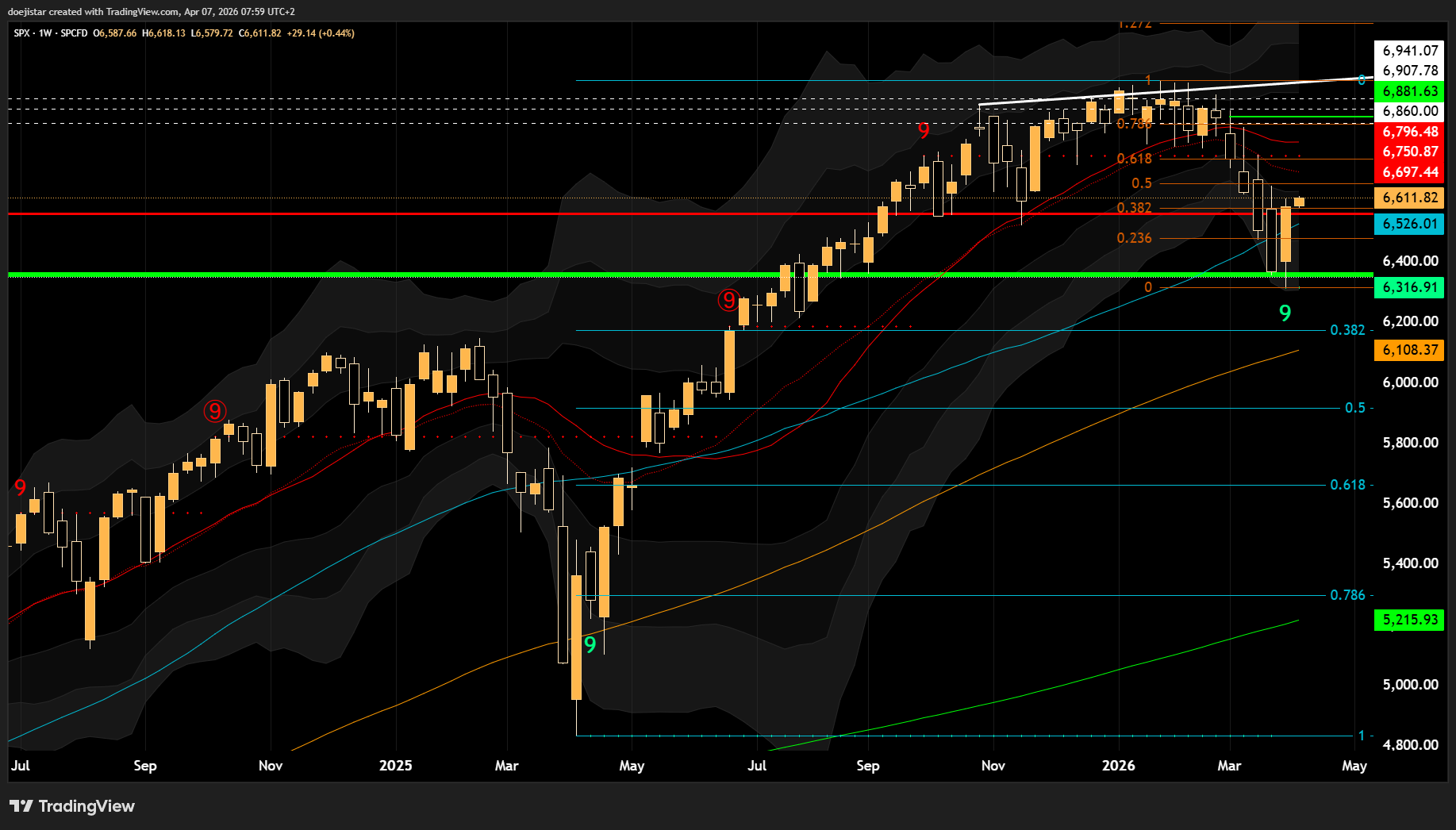

SPX rebounded from my tactical buy level last week to finish above the sell-level in the mid-6500s to close at 6611 yesterday. This weekly reversal is already strong grounds to conclude that a high-probability rebound is underway, along with the 9 buy-setup and low printing right at the weekly 3sd band to add to that signal.

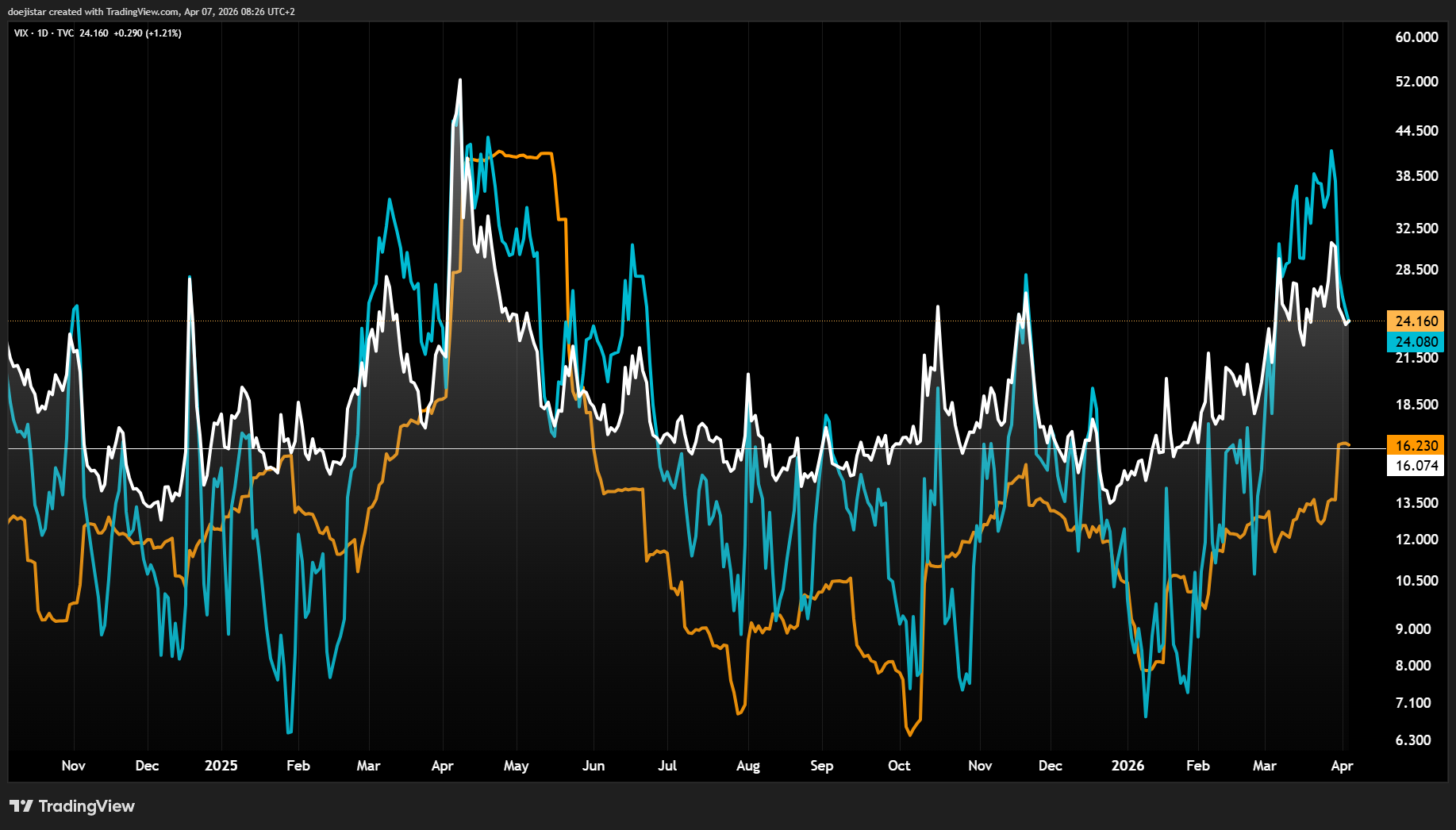

While both the VIX and implied correlation pulled back sharply, they remain very elevated and realized volatility is still pointing in an upward direction.

Gamma Exposure data (using data from SqueezeMetrics) was also extremely negative at the end of March, almost matching the extreme of 2022. This is essentially saying that market-makers were under extreme selling pressure to hedge against the market’s bearish positioning in the options market, and being at the extremes provided ample fuel for the market to produce a v-shaped bounce.

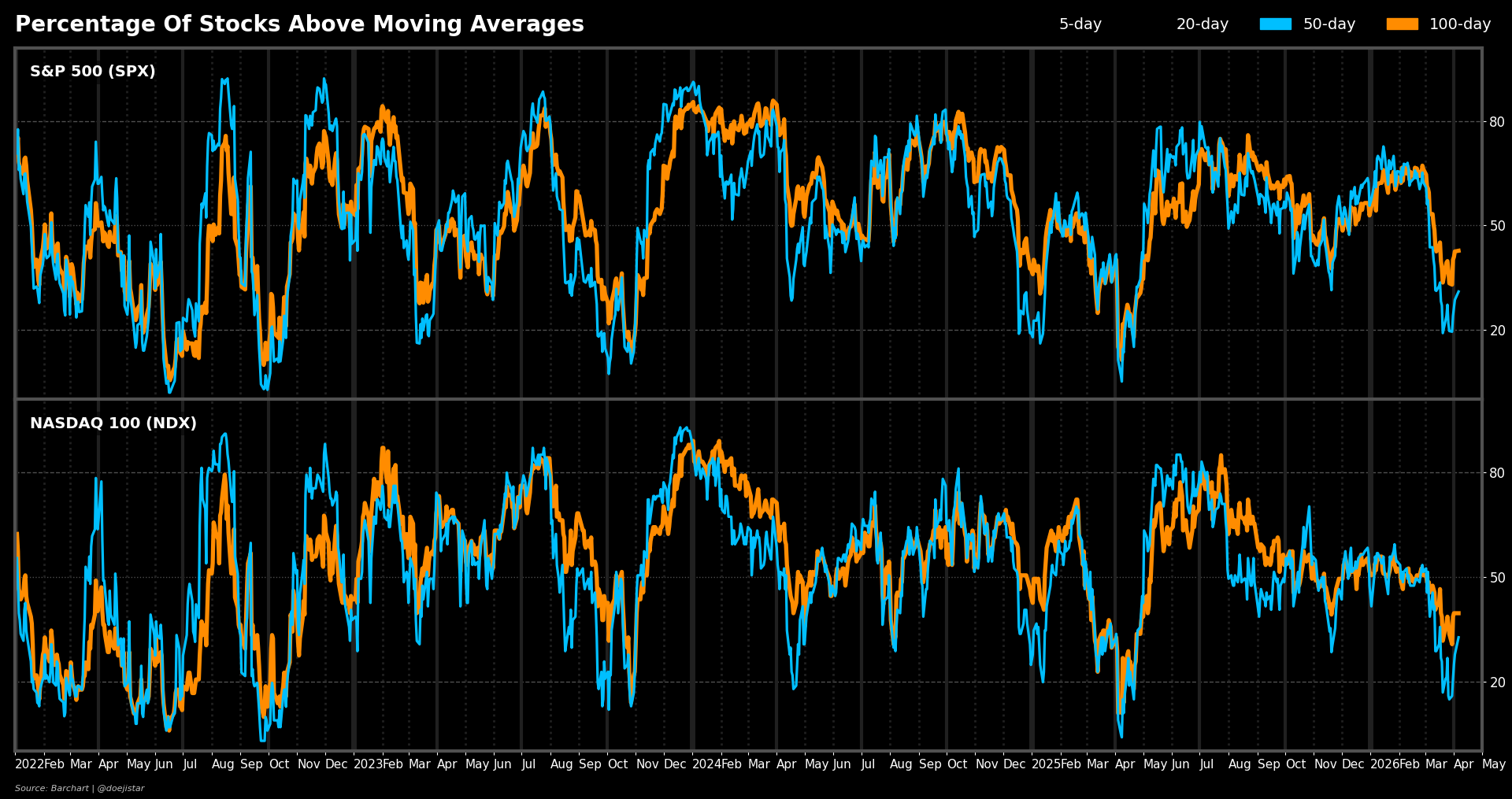

There is no question that equity markets have gotten oversold in a short period and a relief rally is in some sense a natural outcome of such conditions. Historically, however, durable bottoms in stocks have tended to be of much greater conviction where 80% or more of stocks have traded below the 100dma - this condition hasn't been reached this time around.

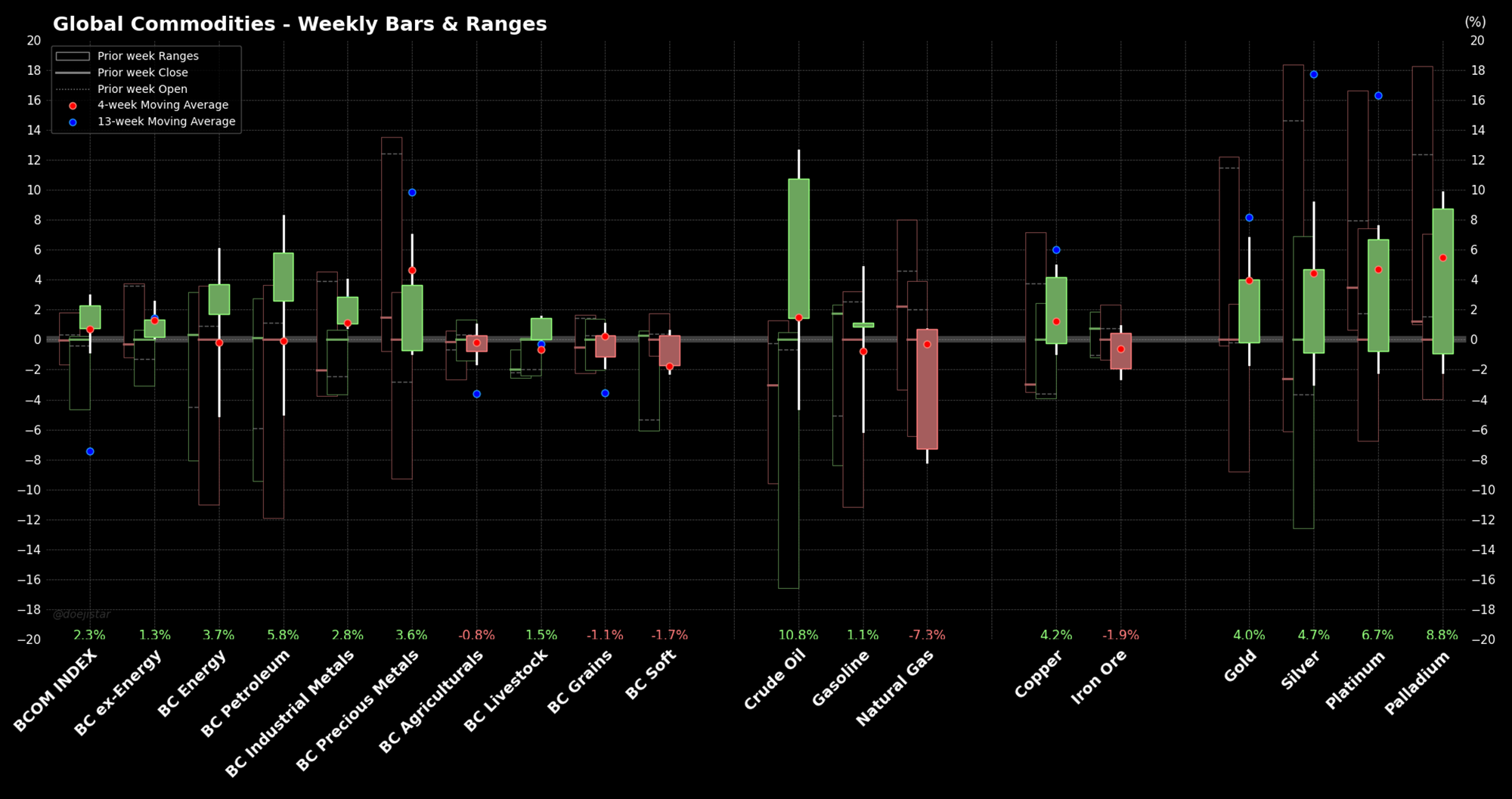

The conditions for a tactical short squeeze were clearly there, but it is difficult to believe there is anything beyond that without a fundamental catalyst, that being - a resolution around Iran, and while Energy prices continued to rip - the Petroleum index being the strongest of the Bloomberg commodity sub-indices last week.

Final words

Despite last week’s optimistic price action, the underlying backdrop still looks fragile. Iran tensions remain unresolved, and there is strong reason to believe they will stay that way, as nothing has materially changed to alter the calculus in our gamed-out scenarios. That suggests continued upward pressure on energy and other commodity prices, while economic data are already flashing stagflationary signals, with some underlying details showing more weakness than the headline prints imply. Taken together, the balance of evidence suggests that last week’s risk rebound was a dead-cat bounce rather than the start of a durable bottom.

A dead cat bounce is a temporary, short-lived recovery of asset prices from a prolonged decline or a bear market that is followed by the continuation of the downtrend. Frequently, downtrends are interrupted by brief periods of recovery—or small rallies—during which prices temporarily rise.

The name "dead cat bounce" is based on the notion that even a dead cat will bounce if it falls far enough and fast enough. It is an example of a sucker's rally. - Investopedia

We'll be looking at this relief rally for opportunities to engage in our usual themes of long Energy and Dollar, short cyclical assets. My current preferences are:

- Short Russell (Long NQ vs Short RTY as a spread is also worth considering)

- Long Crude vs Short Copper

- Long USD vs EUR SEK AUD

That's all for now, good luck trading!