Wk14 MacroTechnicals - Contextual Insights

Oil shocks do not land the same way in every cycle. We compare 1979, 1990 and 2022 to today’s 2026 backdrop to assess whether equities are nearing a durable relief rally — or facing a more persistent stagflationary squeeze.

“Risk comes from not knowing what you’re doing.”

Warren Buffett

Markets have spent weeks trying to trade an oil shock as though it were just another headline-driven wobble. But history suggests the bigger question is not simply how high oil goes, but what kind of macro backdrop it hits. In this piece, we look at the closest historical parallels, why 2026 appears to sit somewhere between 1990 and 2022, and why that distinction may determine whether relief rallies in equities prove durable — or fade into a more difficult stagflationary regime.

Evolution of views

I'd first like to start by giving our non-premium members a glimpse of how we helped traders navigate these challenging trading conditions, then provide a few insights on how to think about the macro going forward. If you think our views and insights will help you better navigate markets, check out our info pages and consider being a premium-member.

The long USD thesis first started on the view that the market was overly pessimistic on the labour market, inflation heading in the wrong direction while growth was strong and likely to stay strong via massive tax refunds under the OBBBA.

I also became bearish on the risk assets and as I thought policy rate expectations were too dovish for the aforementioned reasons, while bullish catalysts were clearly lacking amid AI-capex/disruption concerns with geopolitical risks brewing in the background.

It's been choppy, but there were plenty of opportunities to trade around those views, as well as trading tactically against price extremes and those views given the volatility regime we were in. By this point, we also had very strong conviction about the Dollar given that the many losers from higher oil prices would drive the dollar even higher as the clear winner.

Crude longs paid well, and continue to do so, Natgas, however, has proved challenging as it struggled to maintain trend, despite some very nice rallies during that period. But as I expected the rallies to hold much better than it did, I was unable to make the most of those swings in the end. It's now looking like it's getting going again!

Since the end of that first week of Israel/US airstrikes on Iran, our views have not changed, while we have attempted to understand the goals and motivations of all sides to take a view on the escalations with reasonable conviction, and of which has helped us sift through the barrage of noise.

We then studied game theory mechanics in more detail two weeks ago to build a more concrete framework that helped to elevate our understanding of the various outcomes and how to make a call on speculations about a deal/ceasefire. The details of that we outlined in Wk13 MacroTechnicals - Echoes of 2022 which is available for all to read.

Lessons of the past

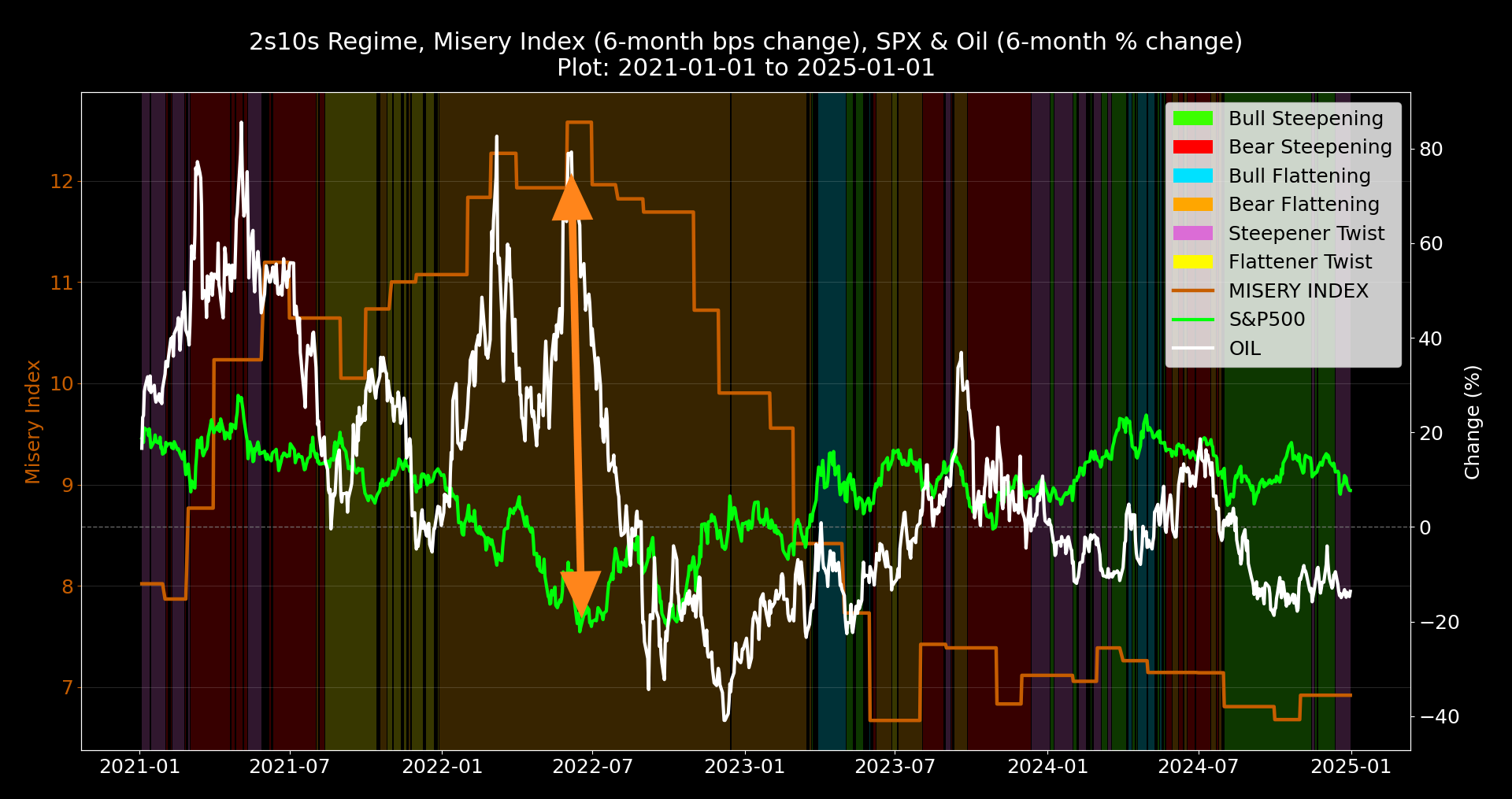

In recent weeks I have been commenting that I don't think many/most appreciate the possibility of a deep drawdown or even a potential bear market this year which, in the absence of a resolution to the Iran-conflict, is a risk that is incrementally rising by the day. I've seen numerous comments and statistical work this past week in the context of the current drawdown in equities and Oil price shocks, but where I think these studies are greatly lacking is that not only is the sample size very small, they also lack some very important macro context. Just as we touched on last week, we attempt to draw on lessons of the past in a bit more detail to find contextual patterns that could be applied to our current environment.

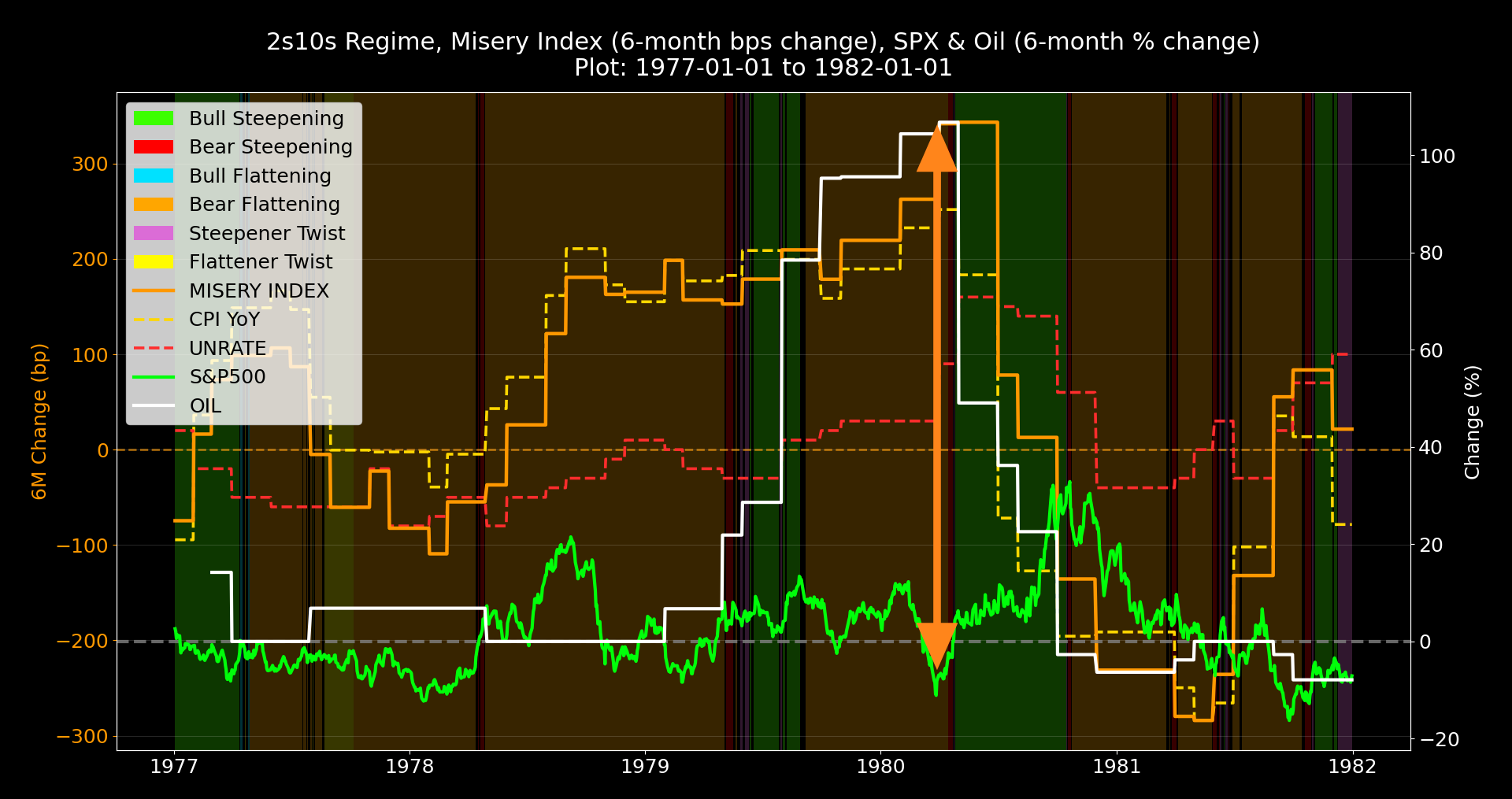

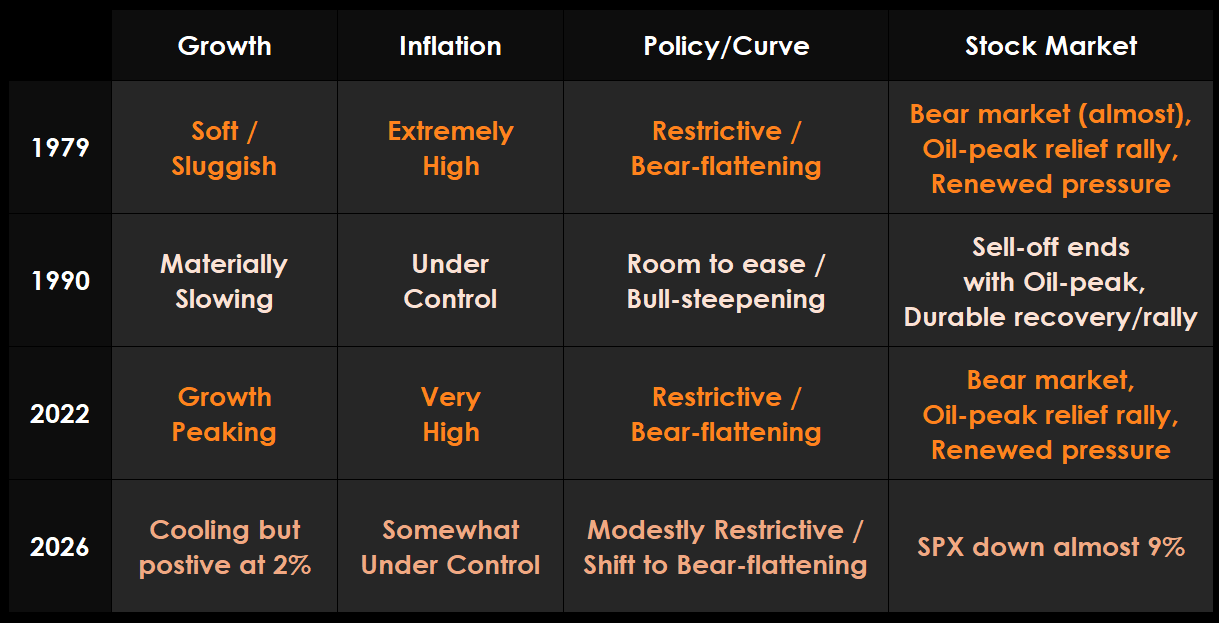

1970s saw two oil price shocks. The first followed an Arab oil embargo in October 1973 causing oil prices to quadruple within the space of a few months, and the second followed a regime change in Iran in 1979. Without going into the specifics, inflation was left undefeated into the second price shock and a bear-flattening regime dominated through the late 70s and early 80s. Stocks reacted favourably to the end of the initial inflation shock, but later had to reckon with policy staying aggressively restrictive as a result of inflation expectations staying high. A tumultuous period for stock markets at the turn of the decade and in the initial years of the 80s.

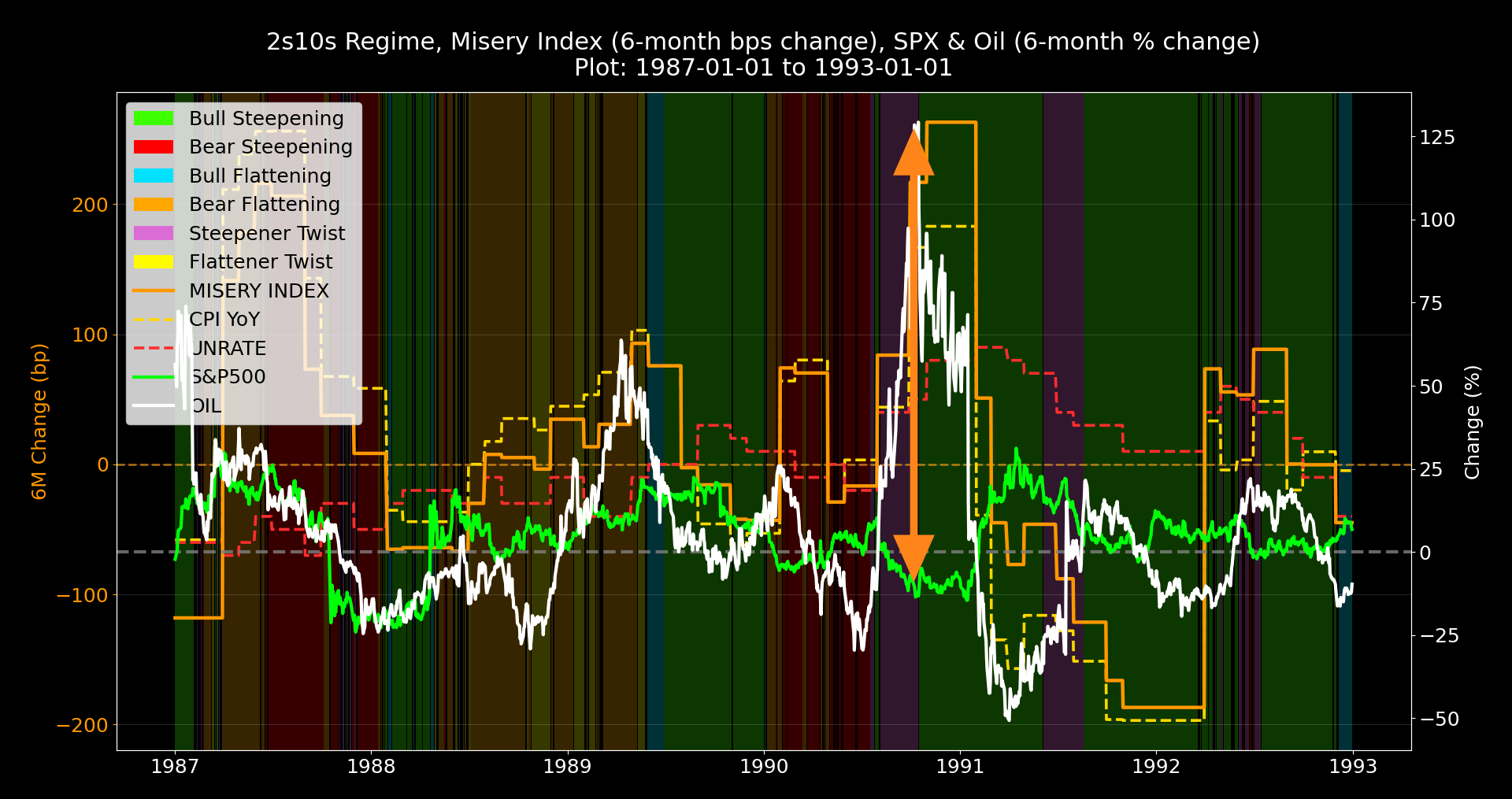

1990 oil shock came after Iraq's invasion of Kuwait, and at a time inflation was relatively under control by policymakers, as well as some slowing in global growth. The key takeaway is that a softer inflation/growth backdrop helped to absorb the inflation shock and keep rates in an accommodative (bull-steepening) regime.

2022 as covered last week followed the Ukraine invasion where we had a macro backdrop of high inflation and the Fed embarking on a hiking cycle, which is contextually similar to the late 70s where an aggressive policy stance dominated to bring down inflation (bear-flattening). Stocks went into a bear market but soon reacted favourably to the peak in Oil in June, before having to reckon with lingering growth concerns amid ongoing tightening in monetary policy.

2026 = 1990 or 2022?

The yield curve has transitioned into a bear-flattening after starting with expectations for 3 cuts this year, to now pricing in none. Growth remains fairly positive and inflation partially contained, so far. Contextually, I think this makes our current environment somewhere between 1990 where policy had gone on an easing-cycle, and 2022 where policy was embarking on a tightening-cycle.

The clearest historical pattern is an initial sell-off in equities that finds relief when the surge in oil prices peaks, so the question for 2026 is whether the initial relief behaves more like 1990 where weak growth had kept inflationary pressures short-lived, or whether it becomes more like 2022 because sticky inflation and the need for restrictive policy dominates. I'm leaning towards 2022 for two reasons.

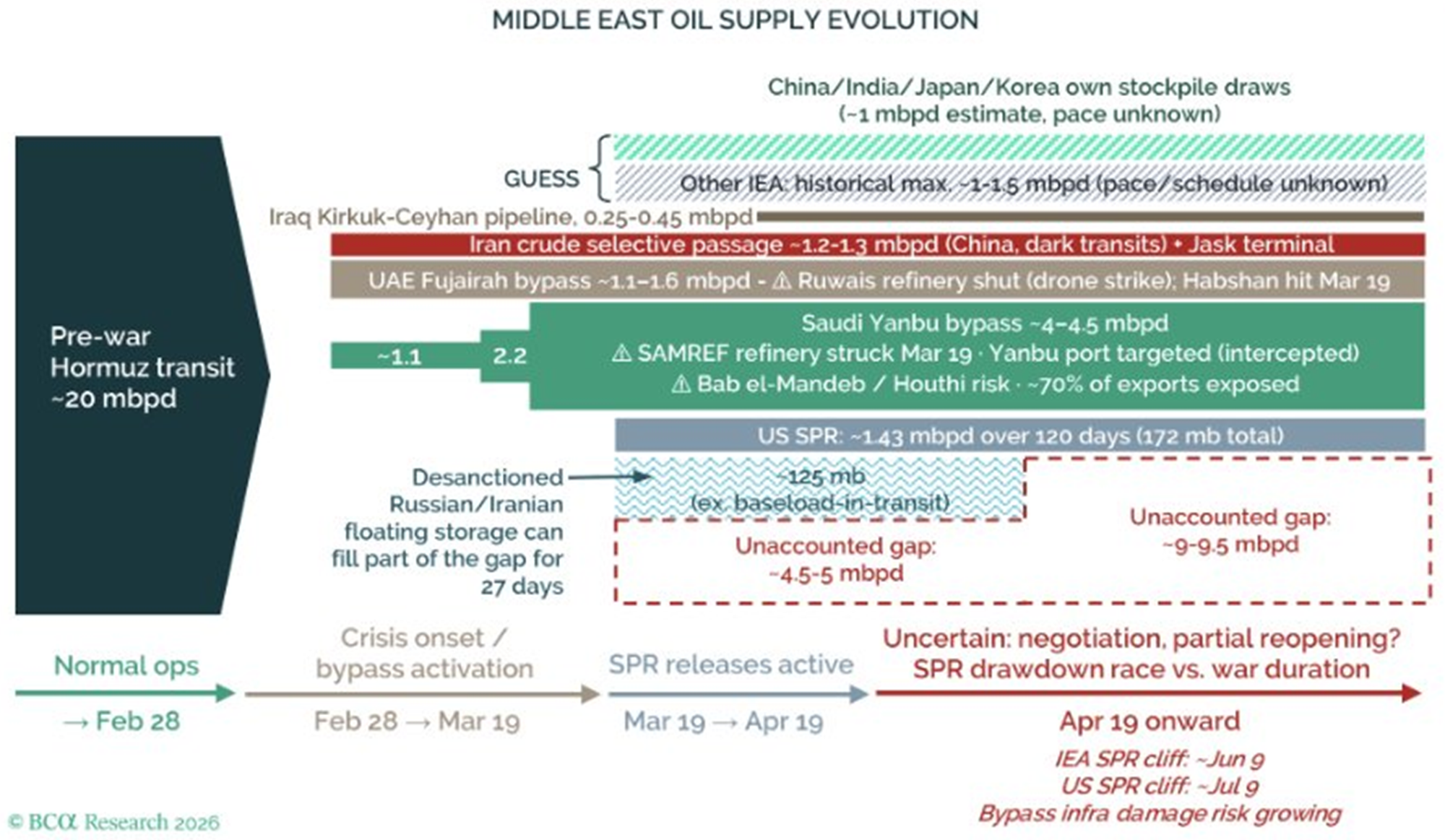

The first is that it will take time for supply to recover with forecasts showing the global energy market is currently undersupplied by 4.5–5 mbpd according to BCA, with some, such as Rory Johnston estimating as much as 6mbpd. And in the absence of a swift resolution, that supply deficit is likely to get worse over time.

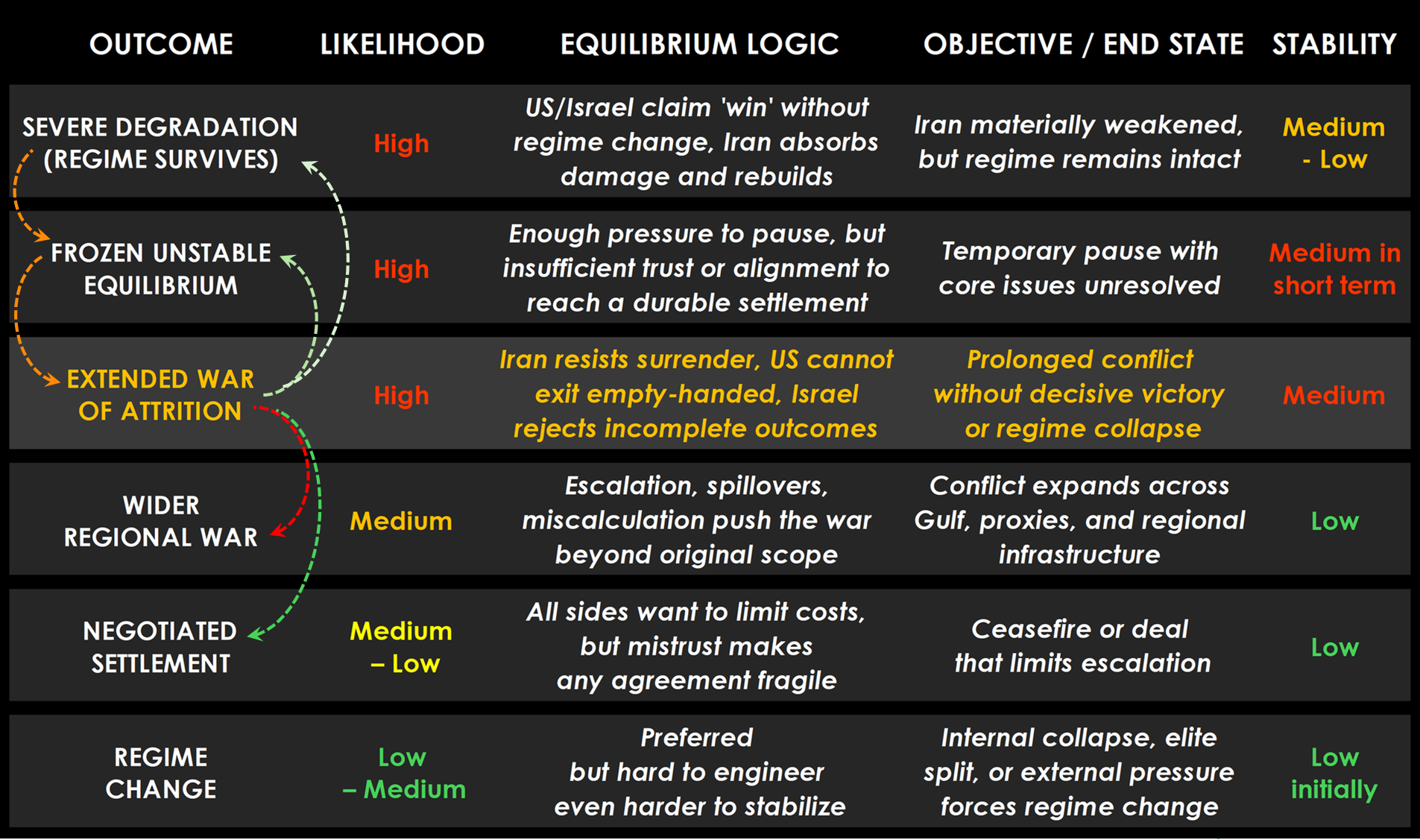

Second, our base case is for the current state of "attrition" to continue due to a lack of common ground for a deal to be agreed upon by both sides - US demands too much while Iran plays the victim card and doesn’t want to concede on demands it largely views as unjust. Meanwhile, other likely scenarios of a 'frozen but unstable equilibrium' and 'severe degradation' point to an extended military campaign in the Middle East that is short of a full escalation which suggests geopolitical premiums will stay elevated due to the constant threat of extended regional supply disruptions.

Put together, that leaves me leaning progressively towards 2022 as the better guide for what comes next. With the supply outlook already in a precarious situation, the longer the conflict remains unresolved, the less likely it is that this proves to be a short-lived inflation shock seen in 1990, making relief rallies vulnerable to fading as investors are forced to reckon with policy needing to stay restrictive for longer.

Where We Stand

The overarching tone is one of escalation, uncertainty, and growing macro strain. What began as a geopolitical flashpoint is increasingly feeding into a broader stagflationary theme through higher energy costs, renewed inflation risks, and a policy outlook that is shifting away from growth and labour market concerns and back towards inflation.

US-Iran Conflict

Iran Sets High Bar in Cease-Fire Talks. Talks won't happen until the five conditions are met.

- Iranian Representatives via WSJ & PressTV

Iran distrusts US intentions, calling the negotiations a 'deception' aimed at shaping global opinion, keeping oil prices low, and buying time for potential further military action.

- Tasnim News Agency

Iran’s assessment is that it is one-sided and unfair, serving only U.S., Israel interests, the proposal lacks the minimum requirements for success, there is still no arrangement for negotiations, no plan for talks appears realistic at this stage, diplomacy has not stopped, and if realism prevails in Washington, a path forward may still be found.

- Senior Iranian Official via Reuters

Markets

"I'm concerned that recession risks are uncomfortably high and on the rise. Recession is a real threat here."

- Moody's Chief Economist

Goldman raises recession odds to 30% on higher inflation, lower GDP outlook as oil prices surge

- Fortune

Investors Flee To Cash as Uncertainty Surges. Investors are shifting back to cash in a move reminiscent of 2022 as geopolitical tensions and policy risks rise.

- Panigirtzoglou, JP Morgan

"A spot energy crunch creates a sustained bid for dollars, as the immediate need for physical barrels translates directly into immediate demand for USD to transact"

- Bloomberg, Brendan Fagan

Short dollar positions of early 2026 were caught offsides. EURUSD to reach 1.12 by year-end.

- Englander, Standard Chartered

Central Banks

FED Cook: “balance of risks has shifted more to inflation.”

FED Barr: “particularly concerned another price shock could increase longer-term inflation expectations.”

FED Miran: "I raised my projection for the Fed rate due to inflation data"

ECB Lagarde: "The shock is probably beyond what we can imagine right now. We are facing a real shock. The markets are maybe overly optimistic. Energy disruptions may last years, economic consequences will emerge only gradually. It might take years to restore the damage from the Iran war."

ECB Nagel: 'April rate hike an option'

BoE Taylor: "Rates should be held until war impact on economy is clearer"

BOE Pill: “I see the upside risks to price stability mounting as a result of events in the Gulf.

The fundamental outlook is becoming clearer with time and clearly heading in the wrong direction. Against that backdrop, we stick with our core themes of short equities and metals, long crude and dollars. That changes until a concrete deal is formally announced, and til then, I see absolutely no reason to fully cover thos thematic trade positions.