Wk9 MacroTechnicals - Trading Ranges, not Dollar Places

Dollar debate is just noise, tactical playbook for a choppy SPX/ES tape and vol regime and how the latest data trends shapes my views

"Trade the range, not the breakout dream" – Adam Khoo.

As discussed in recent weeks, this is an environment (specifically referring to SPX, ES) that will struggle to find a direction, and the strategy that has been working well in recent sessions is to trade the ranges, book profits at next major pivot levels, and avoid holding trades in an attempt to 'let the winners run'. So for today’s weekly, I cover the case for staying tactical in a range-bound market, touching on the current geopol backdrop, as well as the usual key macro takeaways from the recent data and how that feeds into my current views.

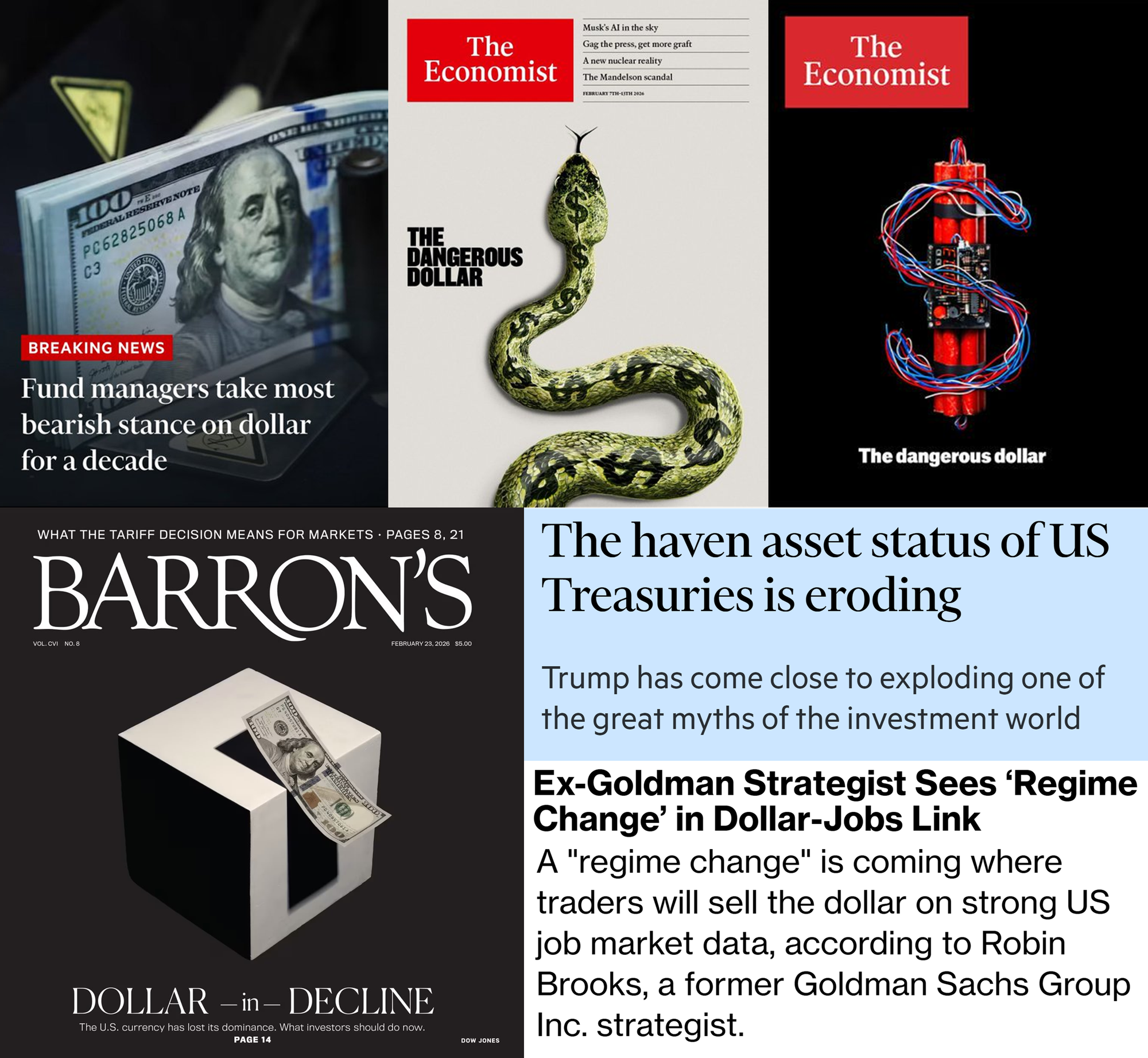

Before we get into all of that, I do want to talk a little about the Dollar which has been a bit of a hot topic in financial news media every since Trump’s Liberation Day tariffs caused an apparent distrust in US policies, and therefore its assets.

Over that time, I've been quite clear about my view that the Dollar simply cannot be replaced, because there is no other system to rival the Dollar. Global debt markets are dominated by the Dollar, and no other currency comes close. Global FX markets (i.e. Global commodities, goods and services trade) are dominated by the Dollar and again, no others come close. And the argument that the Dollar is losing it's safe haven appeal fails to appreciate the aforementioned facts about the global financial system being completely reliant on the Dollar, in other words, in times of stress and liquidity becomes less abundant and any entity needs to ensure they can transact for their very own survival, they will need - you guessed it, the Dollar.

We could go into a multitude of other reasons such as the US role in the maintaining global order through its defense and even economic capabilities, but the long and short of it is that there is no rival. And where there is no rival, these claims that the Dollar has lost its dominance and safe-haven appeal is the financial equivalent of the flat-earth theory. (sorry flat-earthers)

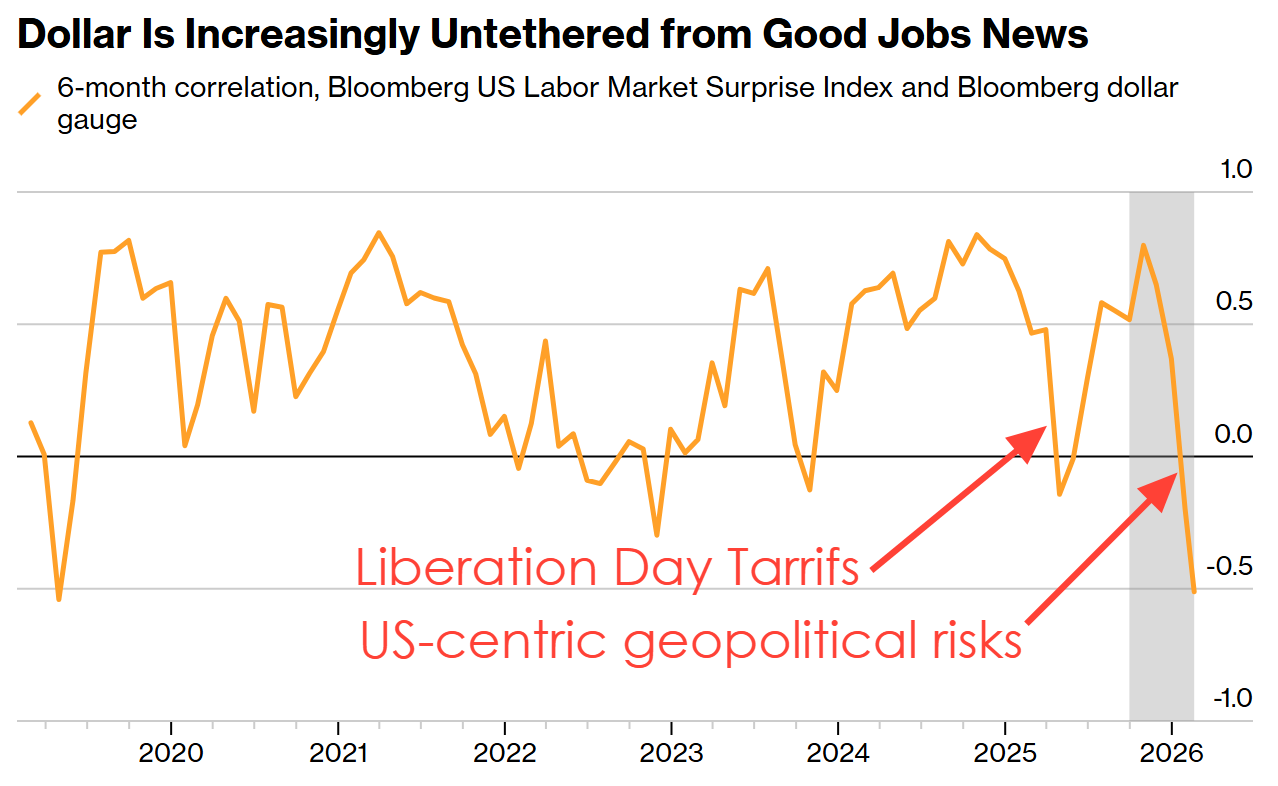

We then come to the idea that the Dollar regime is changing, which has been spoken about by Robin Brooks. It's hard to dismiss the evidence such as the chart below that the Dollar is no longer reacting to the macro data, and is instead tied to the risks associated with Trump's policies.

But is this the death of the Dollar and the start of prolonged regime change? Most likely not. In fact, given what we know about the Dollar's role and dominance in the global economy, it's more than reasonable to believe that this will be temporary. To take that a step further, there are macroeconomic reasons to believe that the Dollar can certainly maintain its dominance, some of which I have covered in prior notes such as last year's Week44 MacroTechnicals - Relative Exceptionalism, and I would say that most of those arguments still hold true to a large extent.

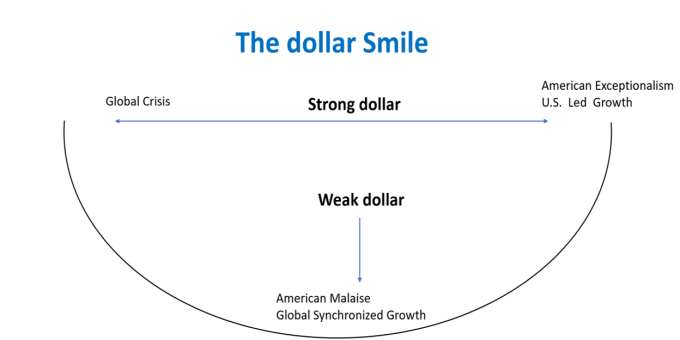

Global growth has been improving recently while the US economy, though strong, has lost some of its momentum of recent years, and even from recent decades of tech-dominated TINA (there-is-no-alternative) as a result of the AI-induced Saaspocalypse. Europe is benefitting from their fiscal defense and infrastructure bazooka announced last year, Emerging markets are enjoying their best period in almost 10 years (check out EEM/EFA or EEM/SPX) and global capital markets have now been presented with 'alternatives' to diversify away from TINA. Politics aside, that has contributed to the Dollar declining to the lower part of the smile.

But if we think about what is about to come next for those recent trends, I think we can find a few reasons and scenarios that support the idea that the Dollar can once again prove its most ardent bears wrong. According to the popular Dollar Smile theory, the USD outperforms when 1) there is a global crisis/recession or elevated geopolitical tensions, and 2) when the US economy outperforms - of which I think can be interconnected since much of the global economy is sensitive to input cost pressures which is often a symptom of geopolitical tensions, and which creates a negative impact on global growth. Unlike emerging markets and much of Europe for example, the US is comparatively less reliant on goods and commodities trade being predominantly a services-based economy that happens to be a large producer of Energy and Food commodities. So, in an environment where geopol tensions become more elevated again, change in economic growth prospects would likely move in favour of those who are able to withstand disruptions of which one of them, just happens to be a country whose currency dominates the global financial system and with no close second.