Wk8 MacroTechnicals - Mood Swings

Weaker breadth, elevated vol, and a negative-gamma tape spells more choppy trading

"Cut your losses short and let your winners run"

- Jesse Livermore

The well-known trading axiom comes to mind this week as I contemplate whether to cut some of my long Dollar positions should the USD continue to trade on the weak side this week, or to commit to my view of a comeback moment for the Dollar — of which I have relatively high conviction about being a potential winner that can run, but not so much on timing. Thus in this week's Macro, I review the data to show why there’s plenty to be encouraged about despite some recent cooling, and why I see this period as being an opportune moment to buy into the weakness in US yields and Dollar of which we'll explore in the Technicals section, along with other tactically strong themes such as what thinner breadth, elevated volatility, and negative-gamma type environments means for our trading biases in equities, as well as other ideas to have in mind in view of another busy calendar week.

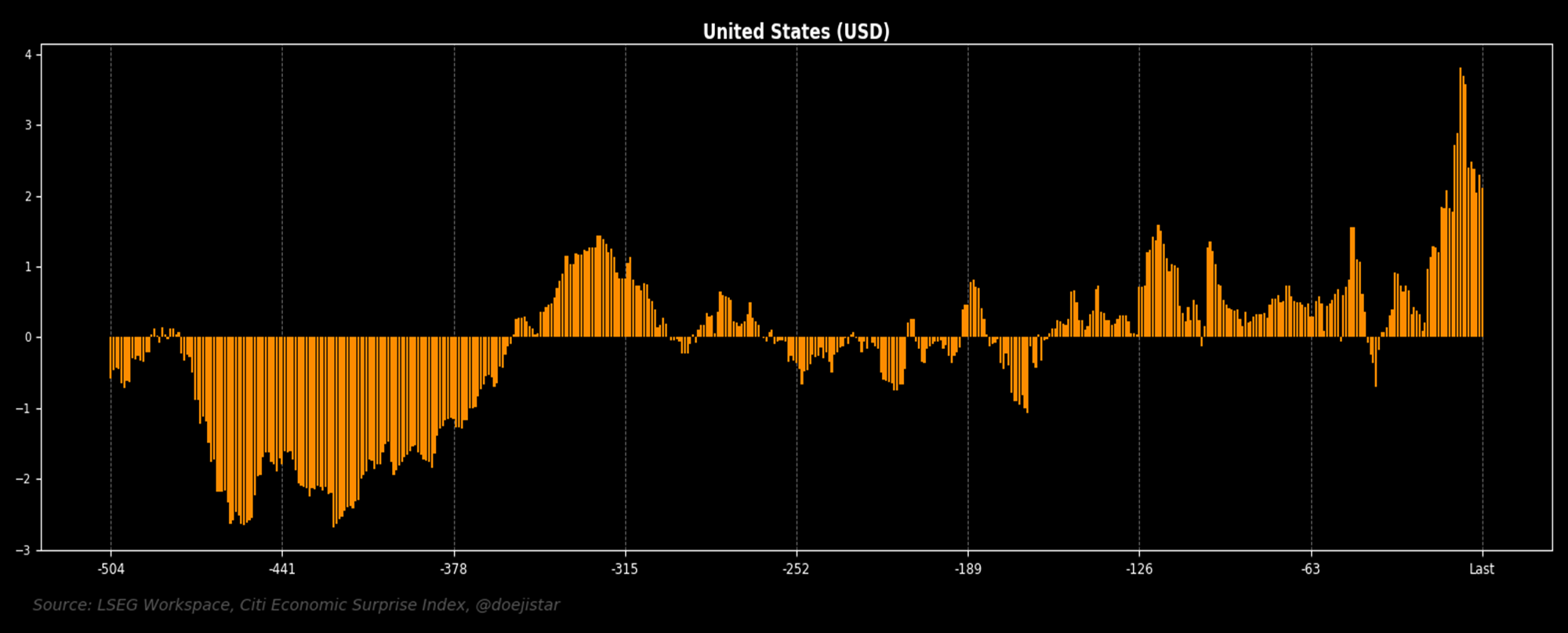

To set the scene for this week's notes, we start by looking at the US Economic Surprise Index, and if it is any decent gauge of economic momentum, the US economy has made an impressive start to the new year. The above shows a standardised version of the surprise index over the last 2-years, of which has risen to nearly 4sd at the end of January and currently settles at roughly +2sd above its trailing 1-year average.

It is possible that the data over the coming month goes through a soft patch due to winter-storm impacts, but I do see this period being an opportune moment to pounce on the weakness in Treasury yields and the Dollar with significant upside risks coming into play for the US economy.

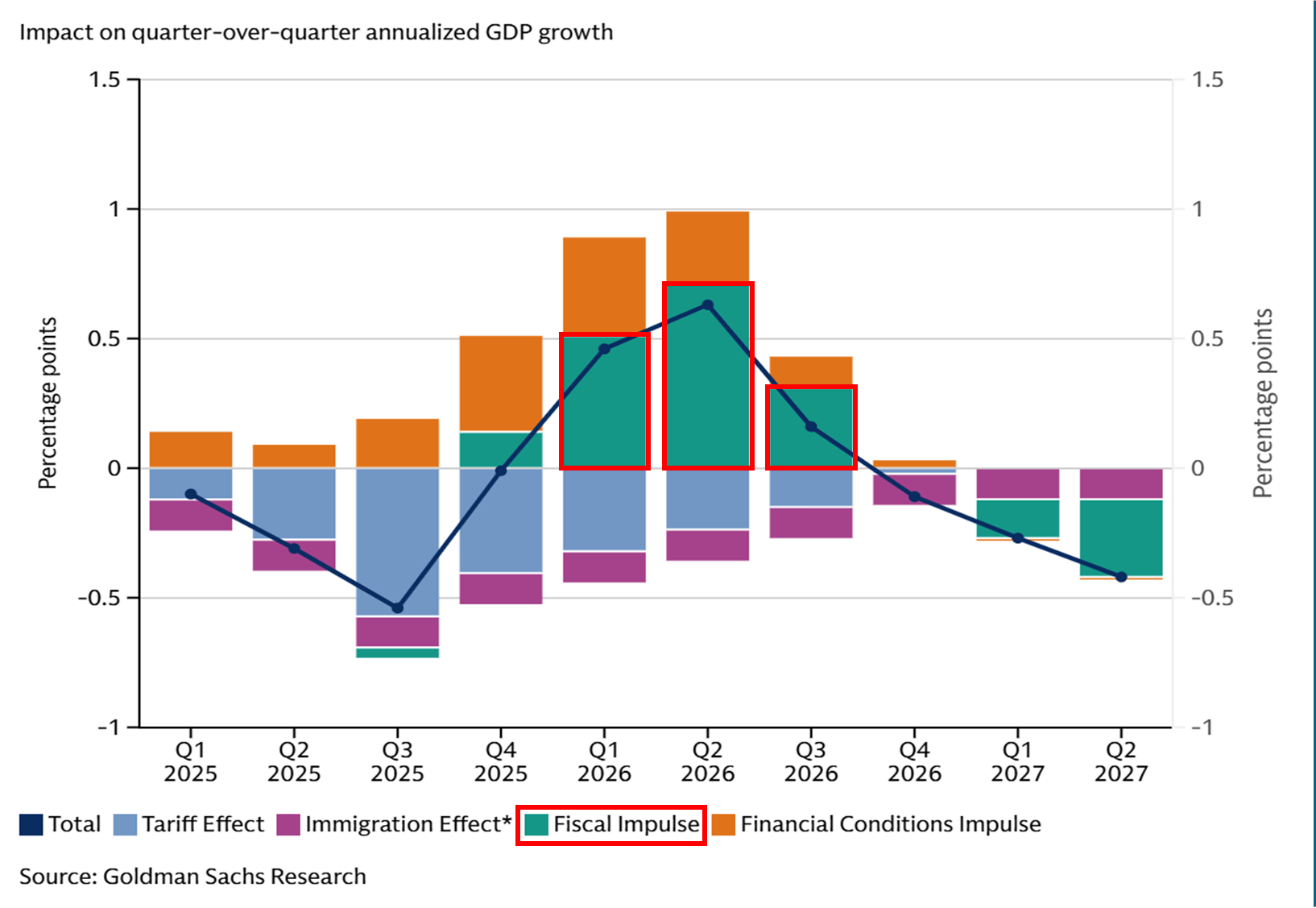

- Massive tax benefits: Drags from tariffs giving way to a massive fiscal boost coming from the One Big Beautiful Bill Act's tax refunds in the coming February-March tax season will help to expand disposable incomes of households, as well as investment capital via accelerated depreciation measures for companies making new investments (i.e. immediate full cost tax deductions for new equipment, factories etc.) which would be a huge boon for growth.

- Easing of longer-term financial conditions: There are a lot of discussions around the Warsh-Bessent (Fed-Treasury) coordination relieving pressure on bond yields. Efforts to reduce the average maturity of Treasury debt holdings isn't new since prior Treasury Secretary Janet Yellen shifted debt issuance into bills, but their efforts should nonetheless help to ease long-end yield and mortgage rate pressures, thus being incrementally supportive for housing affordability and longer-term wealth effects.

The downstream effects on the economy from that fiscal impulse is immense and though all very well-known, putting this into the context of where US yields and the Dollar currently sits, it now looks as though the market has overly discounted the scenario of an economic resurgence through the first half of 2026, and how that shapes the balance of risks for the 2nd half of the year.