Wk6 MacroTechnicals - Debasement-trade Reversal Is Not Real

Positioning likely drove last week’s violent moves so taking chart-signals with a pinch of salt. USD confidence unlikely to have improved, Geopol premiums to stay elevated, PMs and Oil for re-entry longs, Equities show signs of fatigue, and FX/Rates signals messy with USD correlations breaking down.

"In the midst of chaos, there is always opportunity." – Sun Tzu

Some of last week’s moves look more like a positioning unwind than a durable change in market risks and narratives, so I'm not believing what the charts are telling me to believe. I also see the crude/gold dump as a potential opportunity rather than a trend-defining break. Macro focus shifts to the new Fed Chair (Warsh) while the week’s data flow (hotter PPI, softer confidence) keeps policy uncertainty elevated. Technically, equities are shaping up defensively and vulnerable to more chop and corrections, while rates/FX signals are messy with USD correlations breaking down—keeping FX views low conviction versus clearer setups in energy and metals.

Before we start reviewing the market, I'd like to start by thanking those who have taken interest in my analysis that started on Medium 5 years ago, before moving to the current macrotechnical platform. This has developed into a slowly growing community of like-minded and career-aspiring traders, with many exciting plans to roll out for resources, tools, and insights that will help everyone boost their edge as the community grows.

Today's Weekly note will also be the last of the period we've made publicly open, so if you're interested in seeing more, as well as our insights, resources, and tools we've created, check out the website and consider being a part of our growing community!

Macro

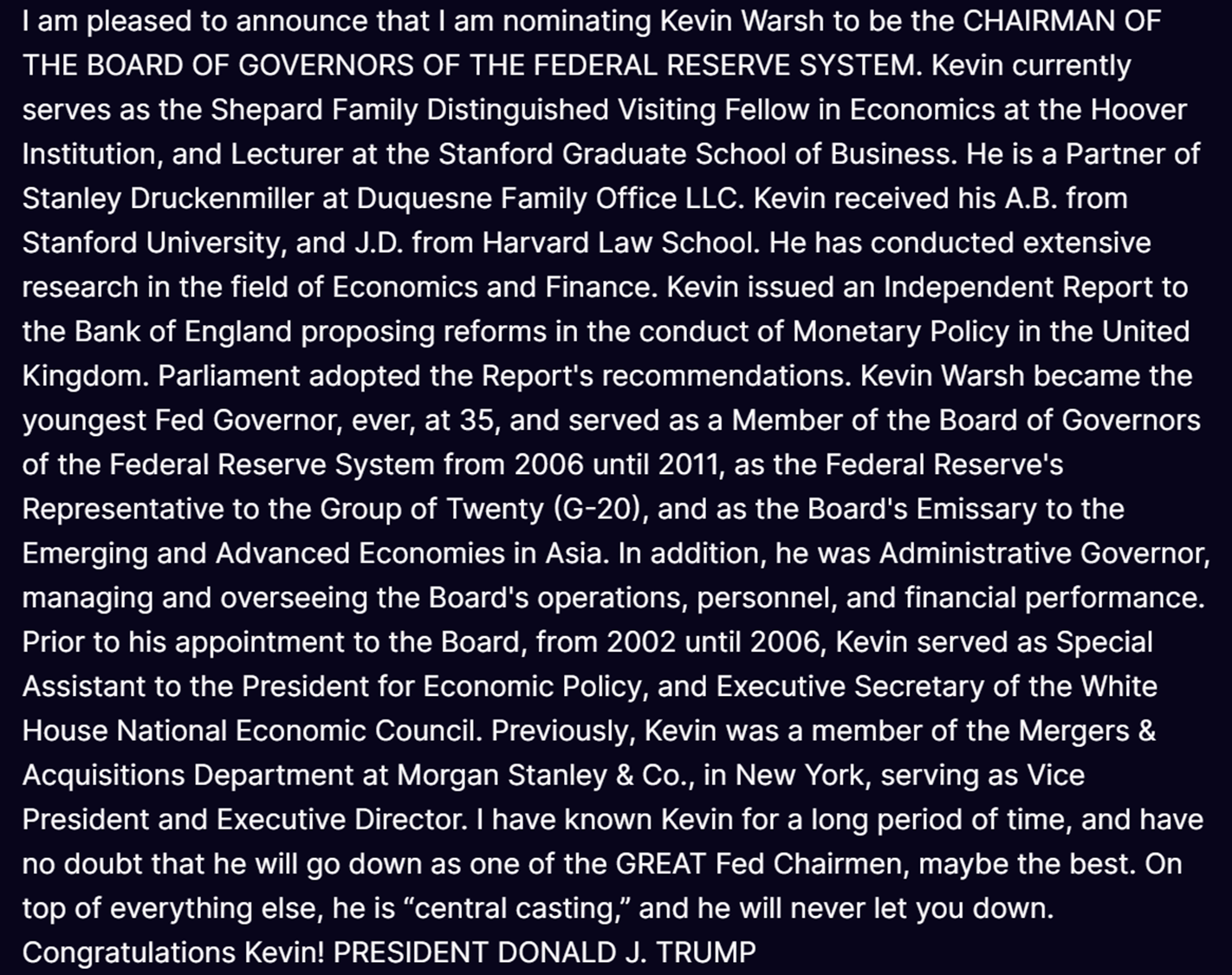

NEW FED CHAIR!

For financial market participants, this is the equivalent of hanging out in Saint Peter's square looking out for the white smoke coming out of the Sistine Chapel chimney signalling that a new Fed chair has been elected. And boy does this man have quite the resume...

AB from Stanford, JD from Harvard law, partner at the Drucks fund, worked with the BOE where UK parliament went on to adopt his recommendations, worked as a White House advisor on economic policy, for Morgan Stanley on M&A, and not to mention having served as the youngest ever Fed governor ever. A ridiculous resume. But does that make him a good Fed chair?

His policy views amid an economic fallout were completely wrong, and what's more is that it was during a period of an economic fallout. Note the numerous comments during 2007-2009 period that he was becoming more concerned about inflation risks when unemployment was surging to as much as 9% and core inflation collapsing from above 2% to 0.8%.

Di Martino Booth mentioned something of an 'inside creed' of not donating to political campaigns and not so much as having a bumper sticker if you plan on working for the Federal Reserve. But as Sonu Varghese points (link) - Warsh, has not displayed political independence with respect to his policy views "being a hard money to easy money guy in 2017, and again in Nov 2022", as well as having very strong familial ties to the Trump family.

So, will Warsh be a good Fed chair with good economic foresight and free from political interference or influence? The evidence says no, and quite emphatically. Claudia Sahm also has a piece on this for further reading (link).

CENTRAL BANKS

FOMC

While there was "broad support" to hold the rate steady, the event came off every so mildly hawkish as they saw downside risks to the labour market having reduced with "some signs of stabilisation" while inflation being "somewhat elevated".

Riksbank

The board held rates steady at 1.75% and expect it "to remain at this level for some time to come", noting stronger than expected activity, lower than expected inflation, and a labour market that it still considered to be weak but with increasingly clear signs of improvement.

SARB

Two members of the MPC favoured a 25bps while the other four preferred a hold. They noted the longest unbroken growth phase since 2018 and see growth moving higher with upside risks to their projections, and inflation to slow from here with longer-term inflation expectations at record lows with risks being balanced.

US ECONOMIC DATA

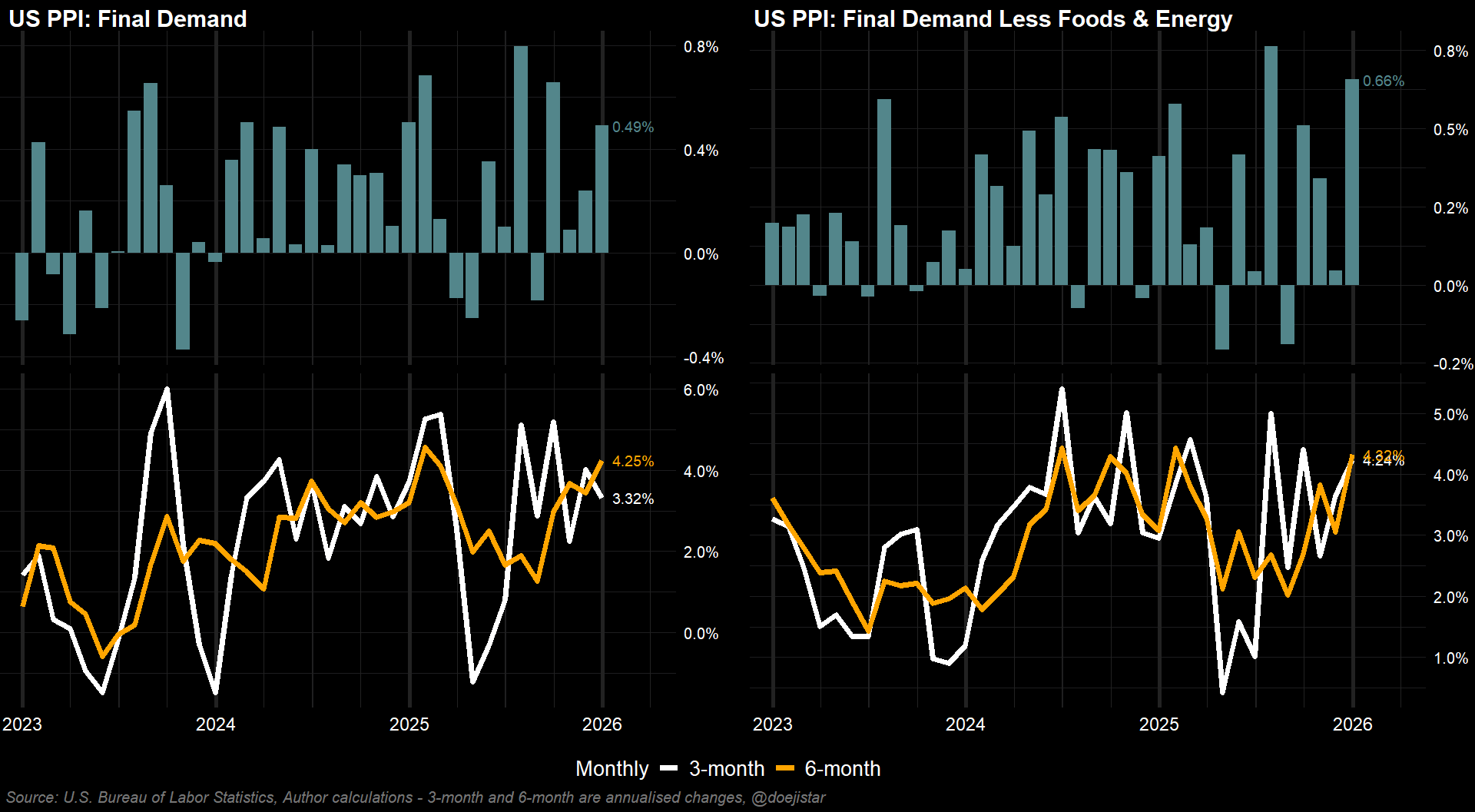

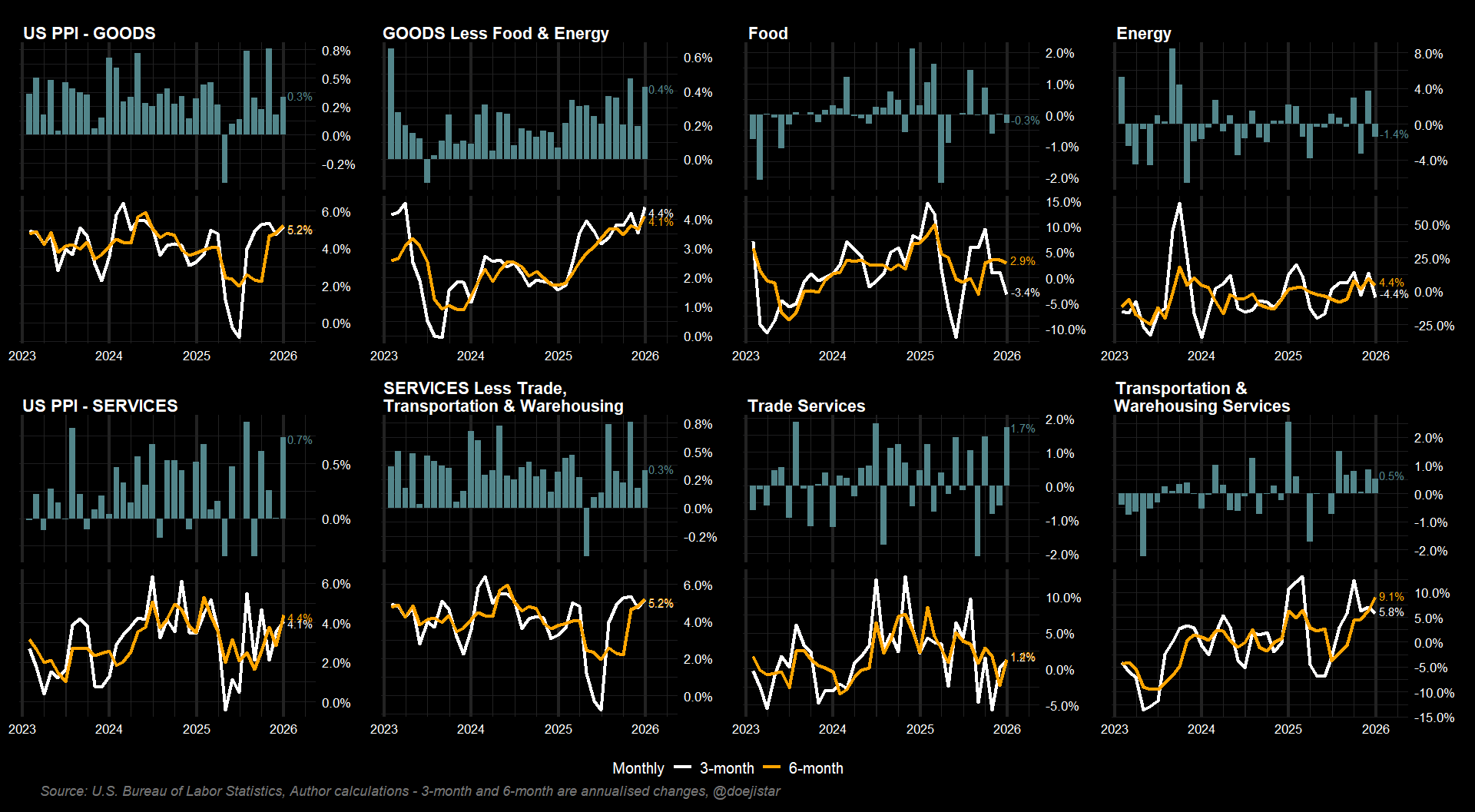

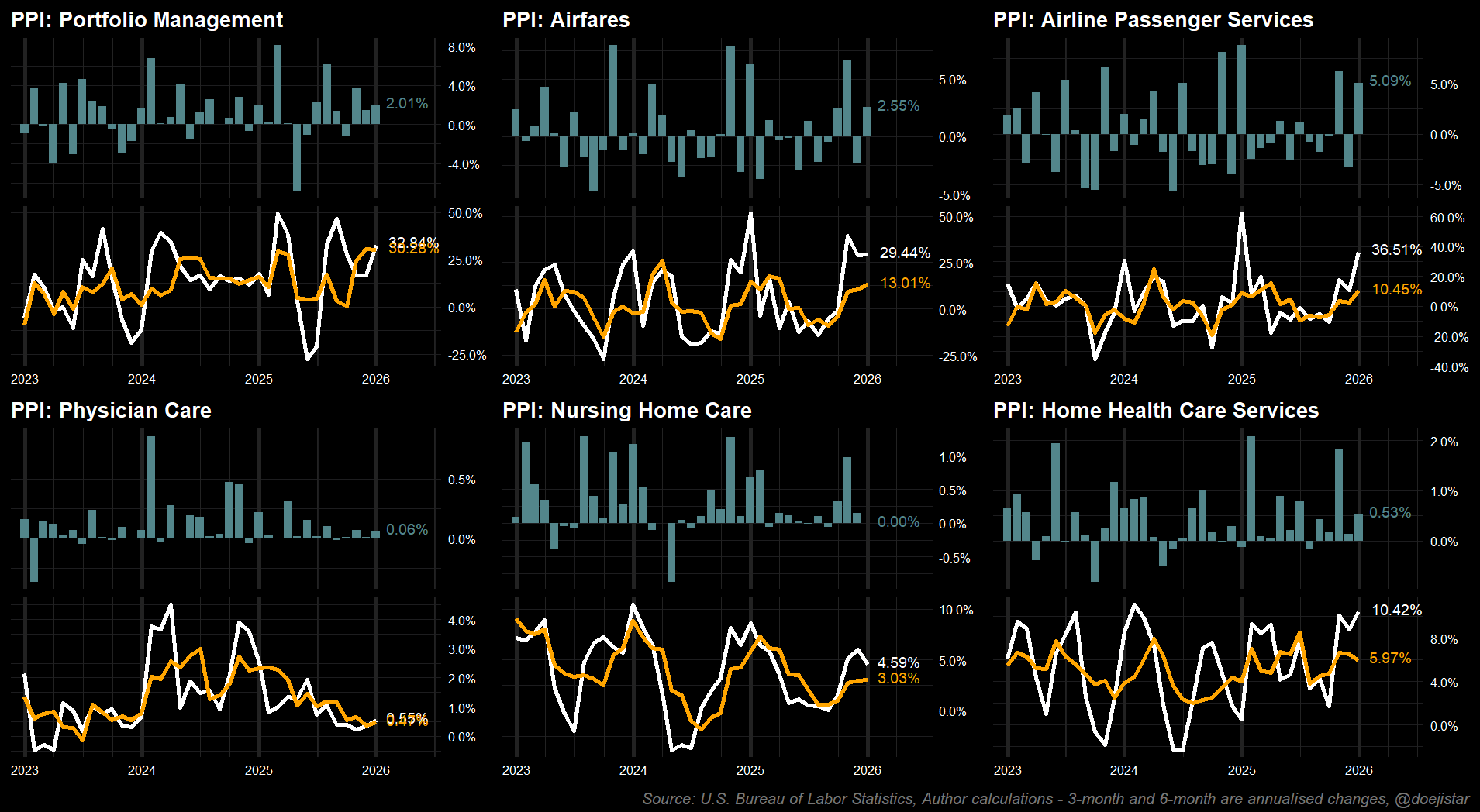

PPI was much hotter than expectations for 0.2% on both prints. Headline 0.49% and core 0.66%.

Despite PPI for Goods being responsible for the recent reacceleration over the last 6-months, it was Services this time driving up PPI - specifically the 1.7% monthly rise in Trade Services that drove the above expected increase in PPI.

In terms of some PPI components that feed through to Core-PCE inflation, there's been a strong uptick in Portfolio Management and Air Transportation industries. Healthcare however, having a particularly strong weighting in CPI and PCE, was relatively stable in December though longer-term trends still point upwards.

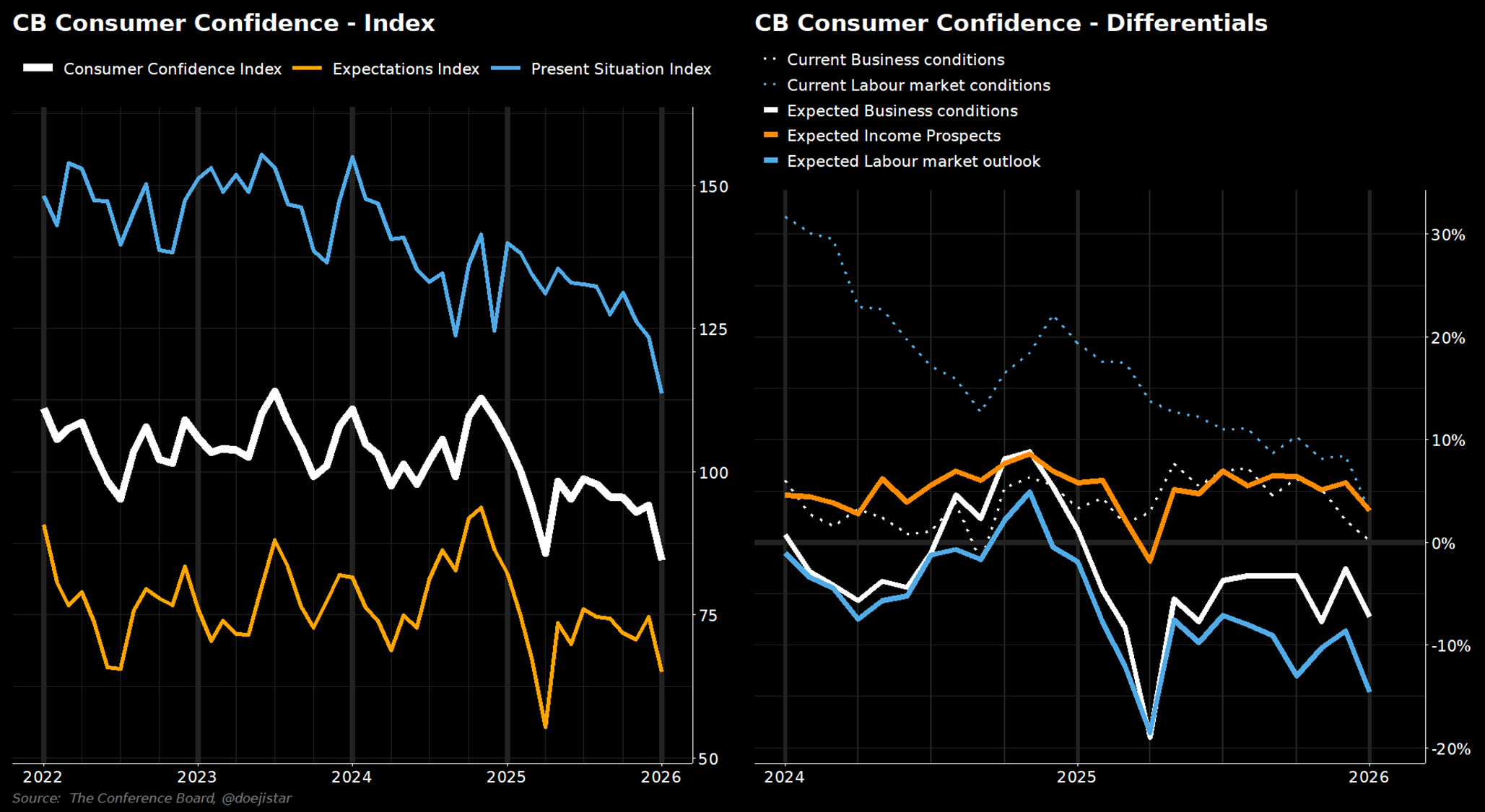

Consumer confidence collapses just after I thought it was embarking on an improving trend. Conference Board economist noted that write-in responses on economic factors remained pessimistic with mentions of inflation and elevated prices of oil/gas and food/grocery costs. References to tariffs/trade, politics, labor market conditions, health/insurance, and war also increased.

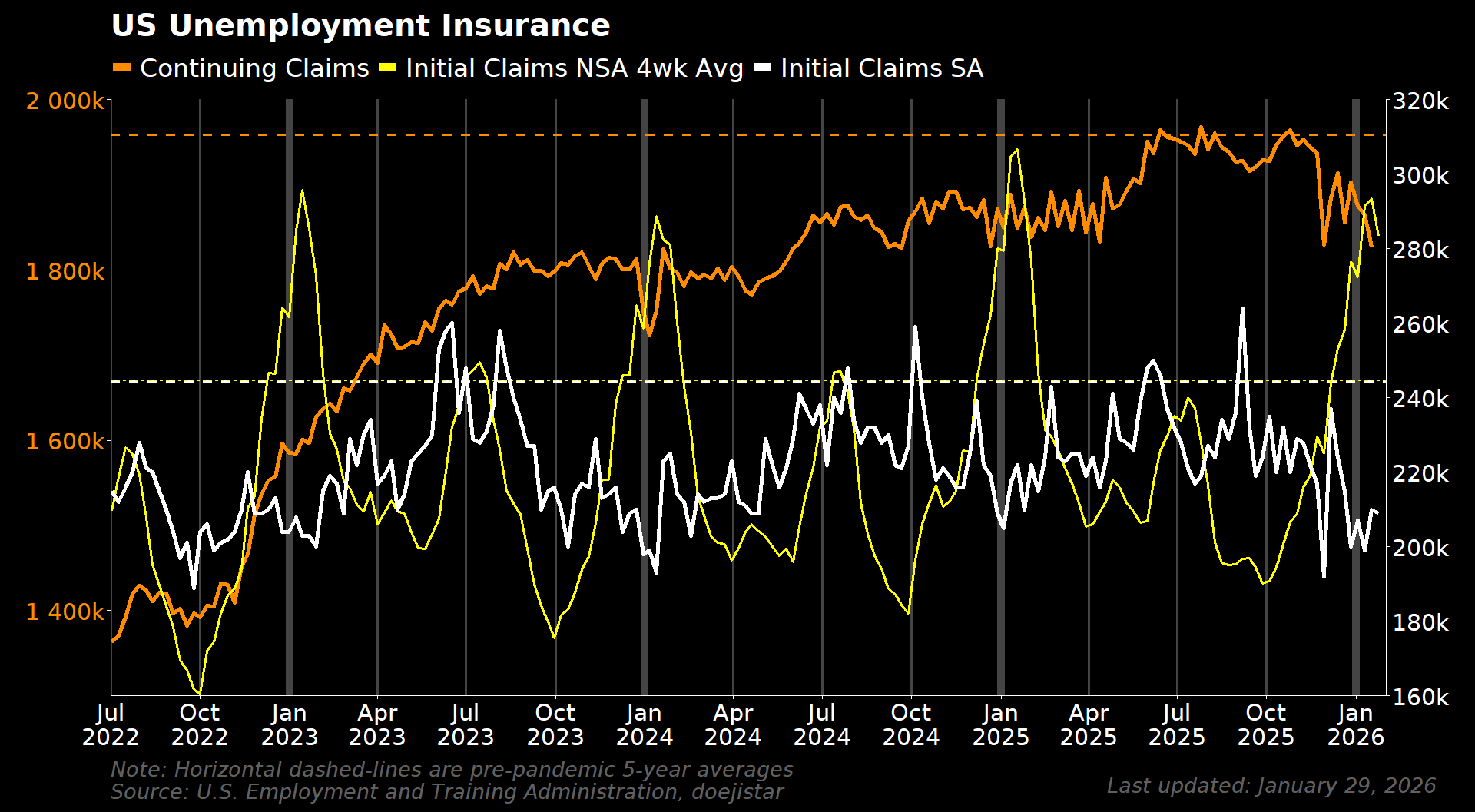

Unemployment claims was slightly above expected while the prior week was also revised up slightly. It is holding relatively steady however while the trend in Continuing claims continues to be encouraging.

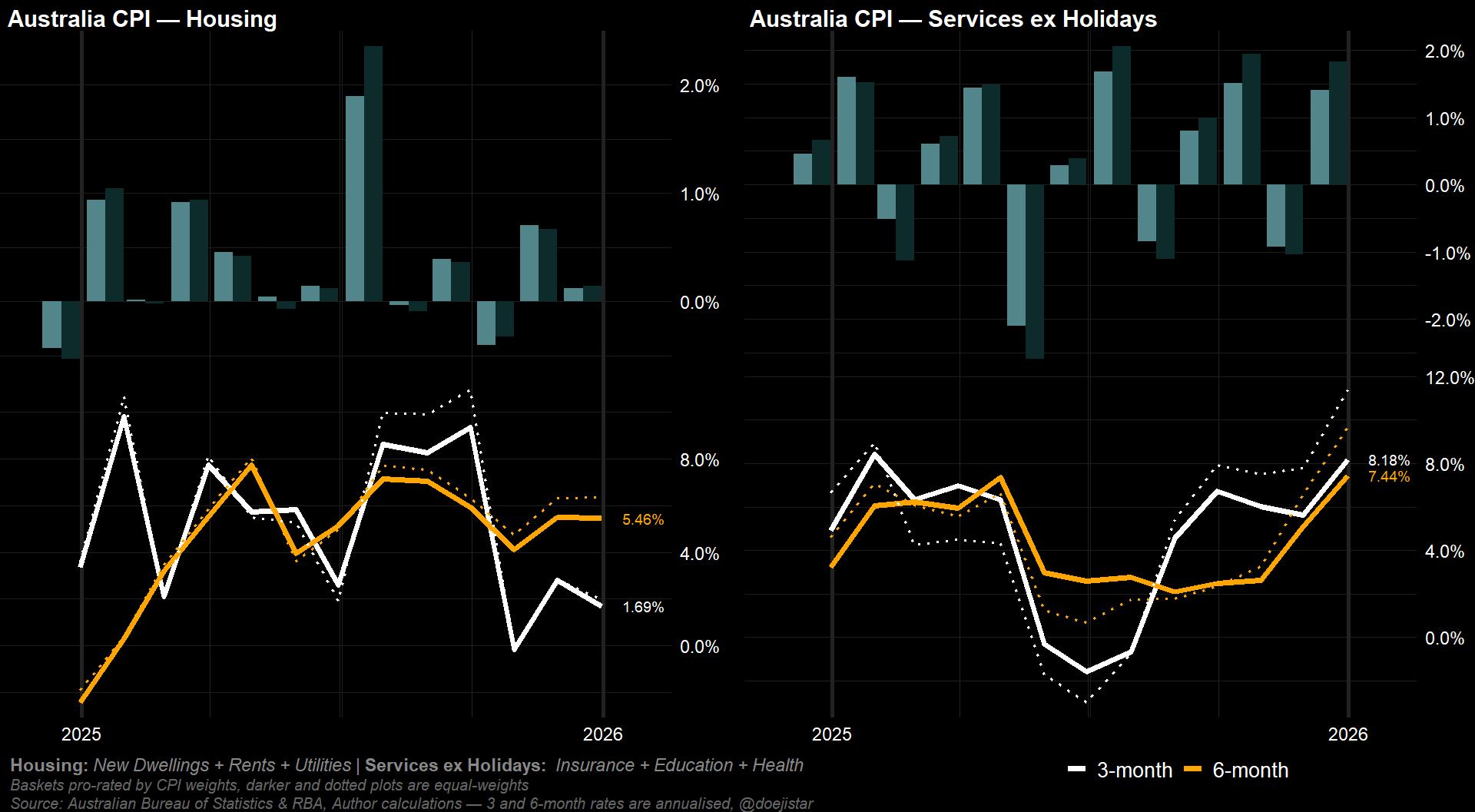

AUSTRALIA CPI

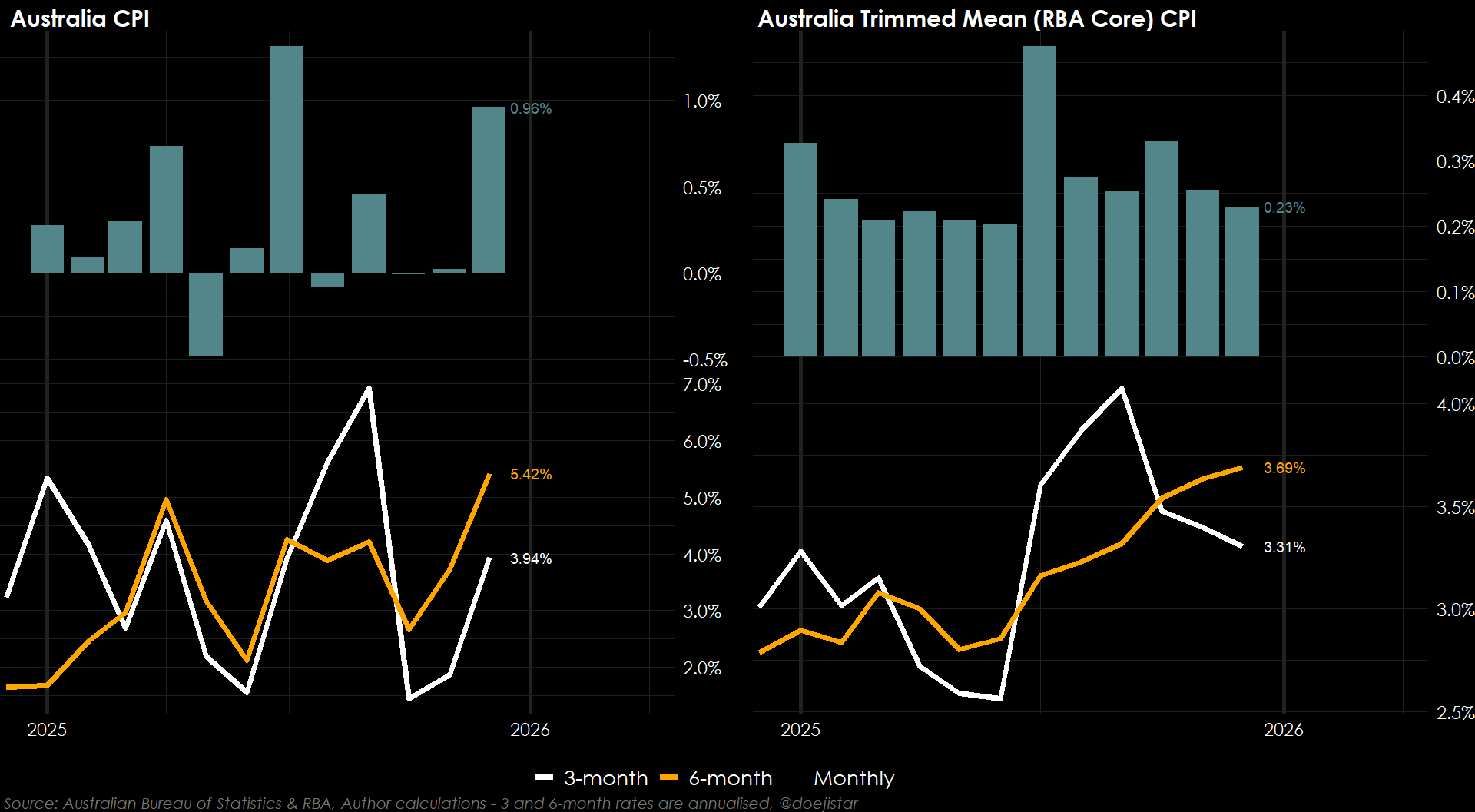

The December CPI report was an interesting one - headline CPI printed 1% which was above the 0.7% expected, while the trimmed mean CPI (which is the Australian equivalent of core inflation) printed 0.2% and below the 0.3% expected.

The surge in headline CPI from 3.4% to 3.8% raised eyebrows and amped up the next rate-hike conversation but from a policy perspective, the 3-month annualised trimmed-mean measure has continued its deceleration to 3.31% from above 4% several months prior, and pointing towards to the 3% level (RBA's trimmed mean target).

The problem is Services however. The RBA tends to focus on Housing and Services to assess inflationary pressures, and while Housing components are steady, Services inflation has continued to be very strong and supported by a big rise in Services PMI from 51.1 to 56.0 in the January Flash release. With inflation expectations rising, it appears the hiking conversation will only get louder going forward and the RBA who meets this week might even surprise with a hike, or guide to one on the current trajectory of Services inflation which they see as being inextricably linked to wage inflation from their statements.

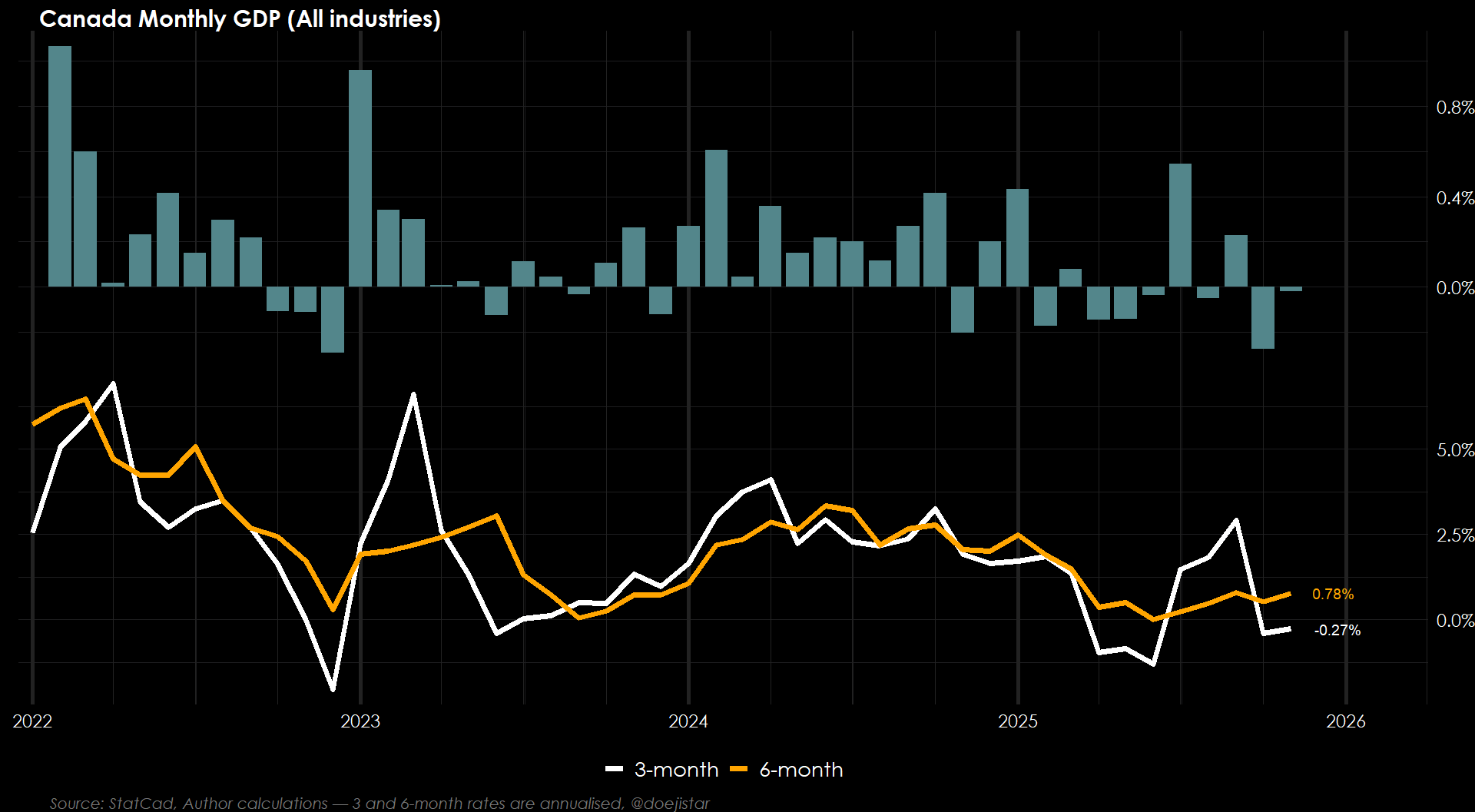

CANADA GDP

To extend upon prior discussions on Canadian fundamentals and evidence of increasing financial strain on Canadian households (unemployment being relatively high and mortgage delinquency rates creeping up among the major cities), the latest GDP print confirms the Canadian economy is experiencing a very mild recession. With a lack of visible drivers for a rebound, CAD remains a strong short preference thematically, and something like AUDCAD NZDCAD could be seeing quite an extended trend following their already strong rebounds.

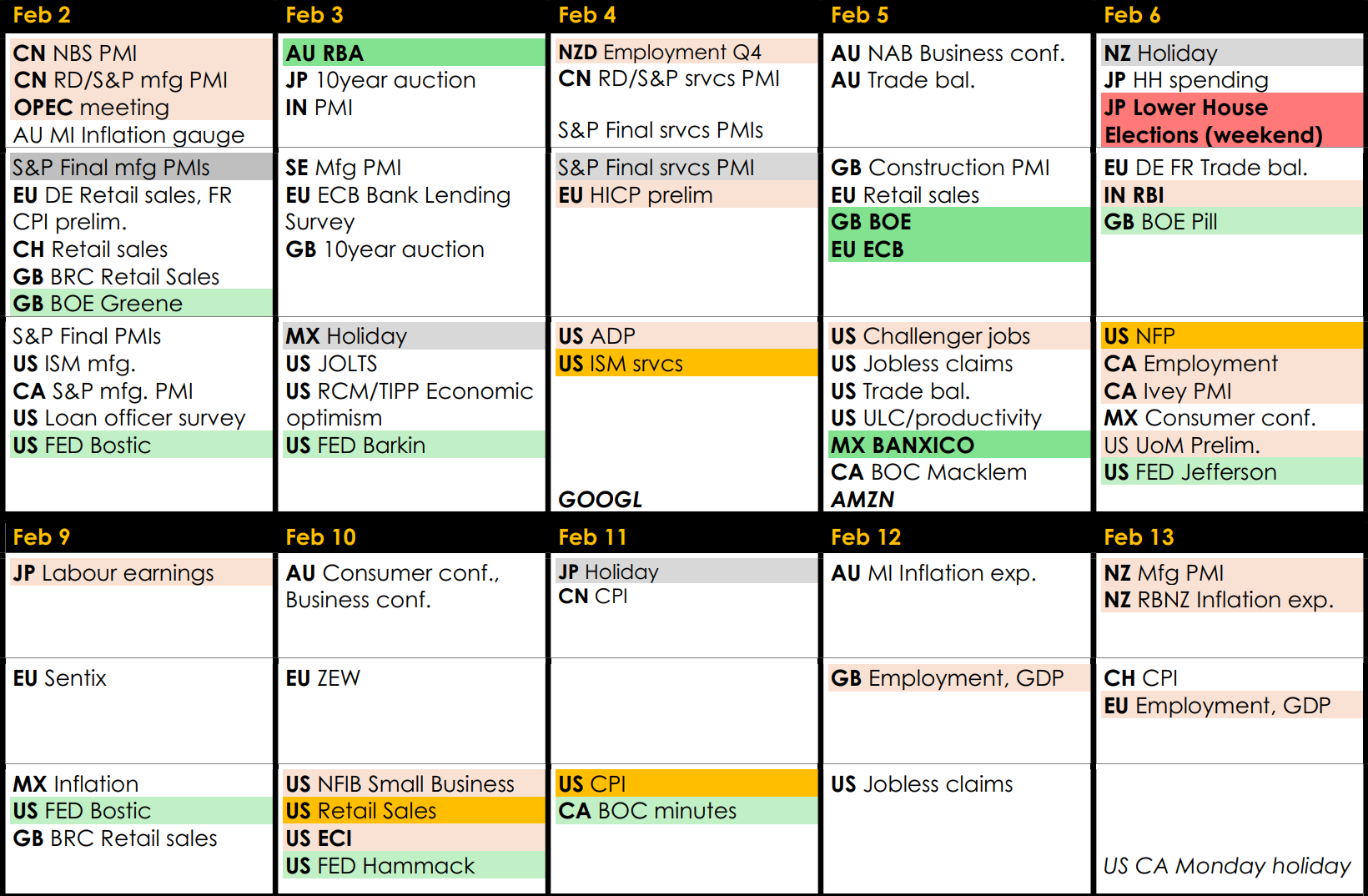

LOOKING AHEAD

Considering there isn't much confidence in the USD at the moment, ISM services and NFP this week could help to change that, especially if the House votes through a funding bill for government shutdown risks to be deferred till mid-year. We also have a few Central Bank meetings - RBA BOE ECB and Banixco this week, and finally the Japan elections which could undermine Takaichi's premiership to lessen debt concerns that has plagued the JPY.

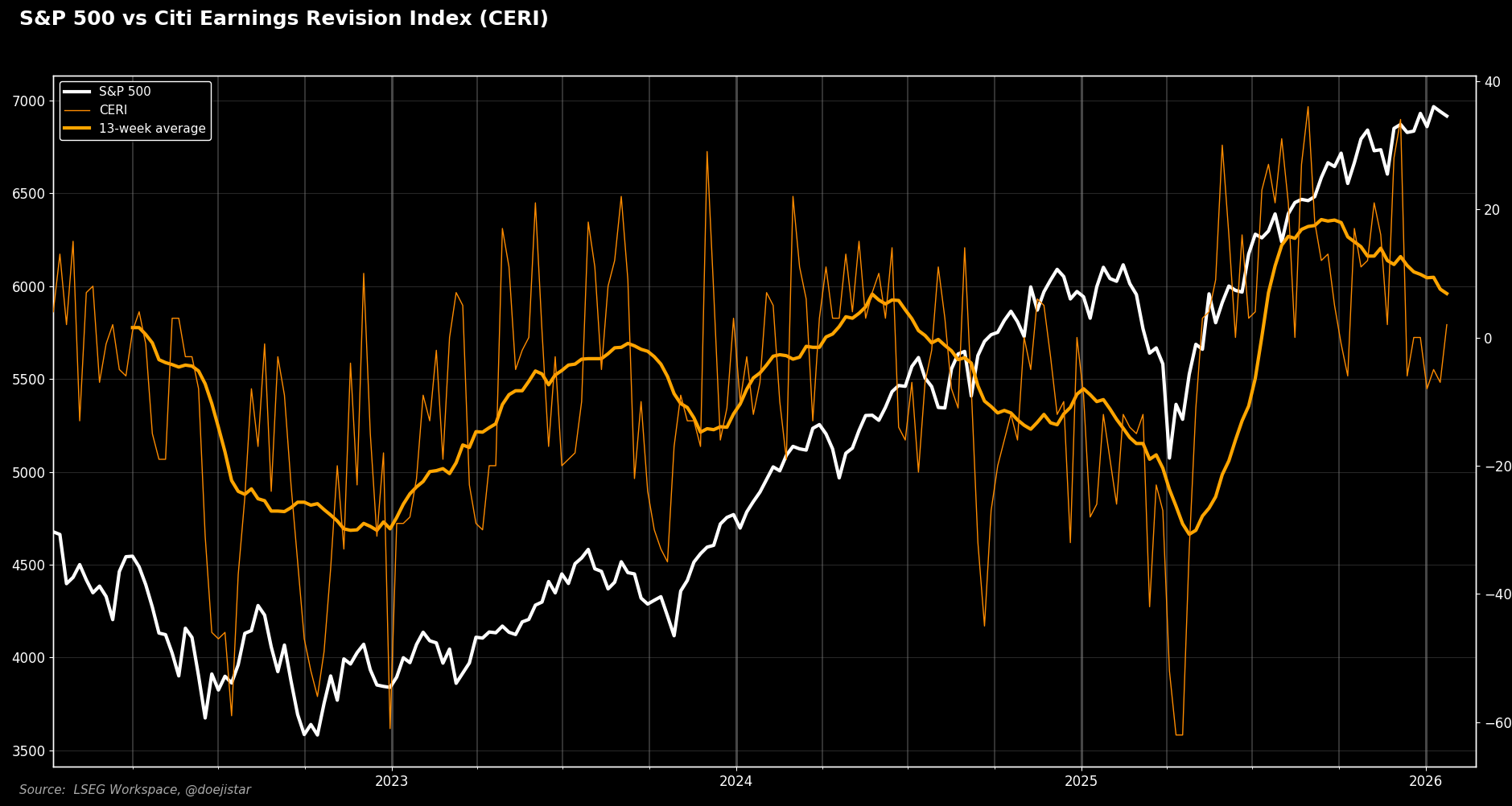

AMZN and GOOGL the big ones, but quite a few names there that will weigh in on how the AI-capex cycle is going. Earnings season is so far going well however with Citi's earnings revision index turning higher.

Technicals

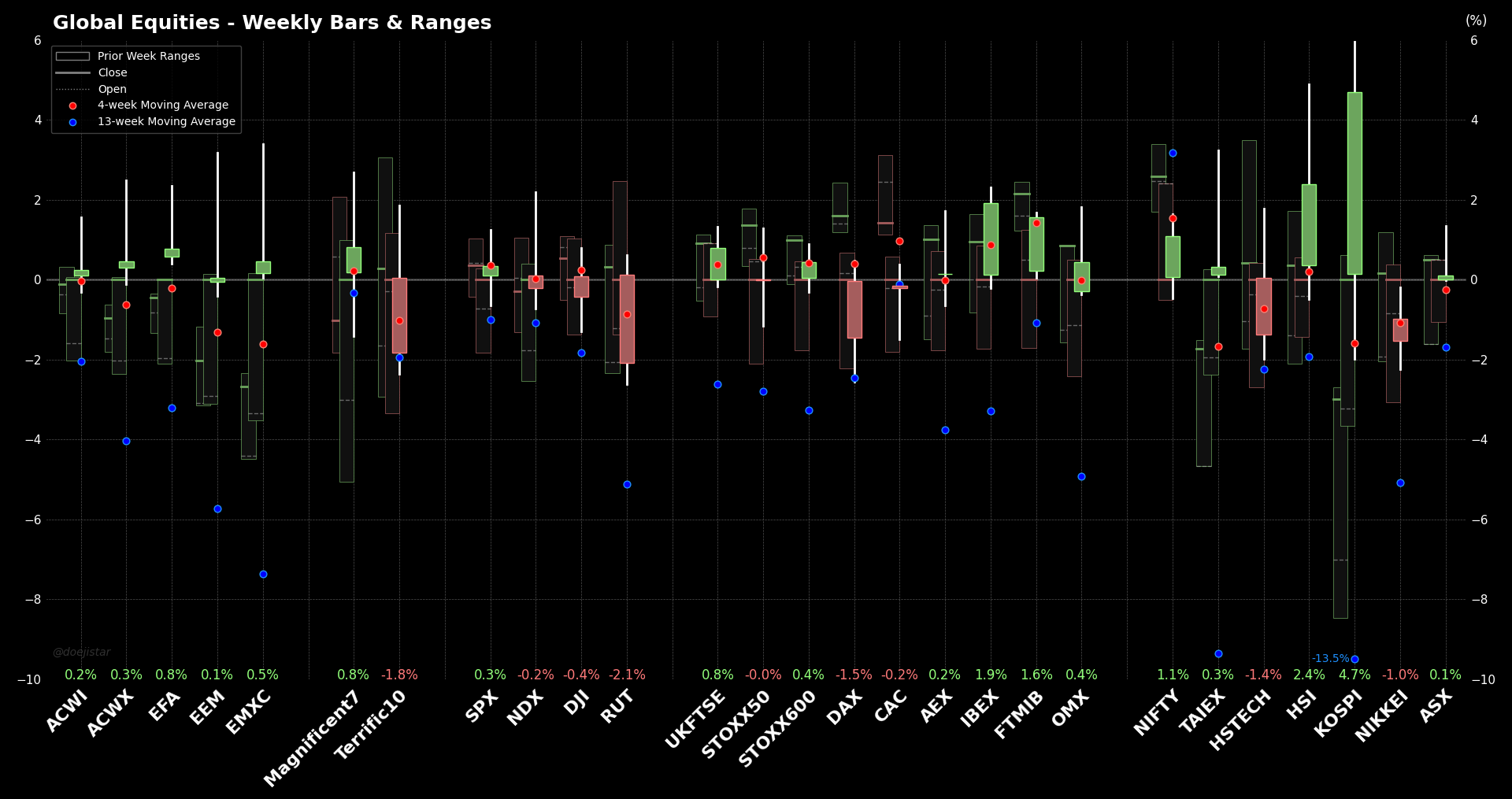

EQUITIES

Market profile for global equities - is starting show some weakness. Barring the KOSPI which is on cloud9 which, I can understand to some extent being a major producer of chips in the face of ballooning compute demand.

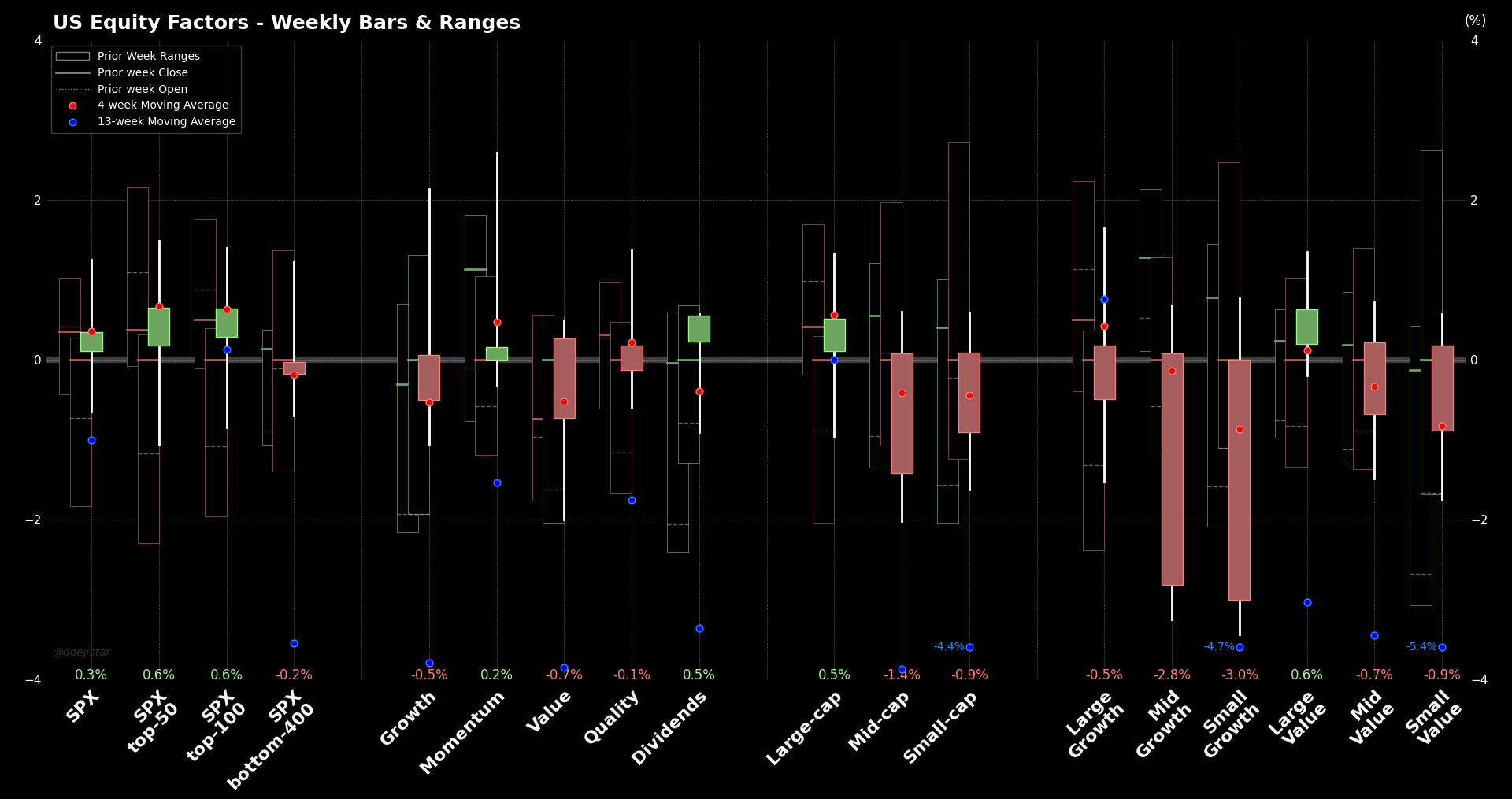

US equities in particular is now showing weakness after many weeks of market broadening with the bottom-400, medium and small-caps, all greatly outperforming large-cap top 50 stocks. We saw some of that reverse last week as the market takes on a more defensive posture with Dividends and Large-Value factors performing well.

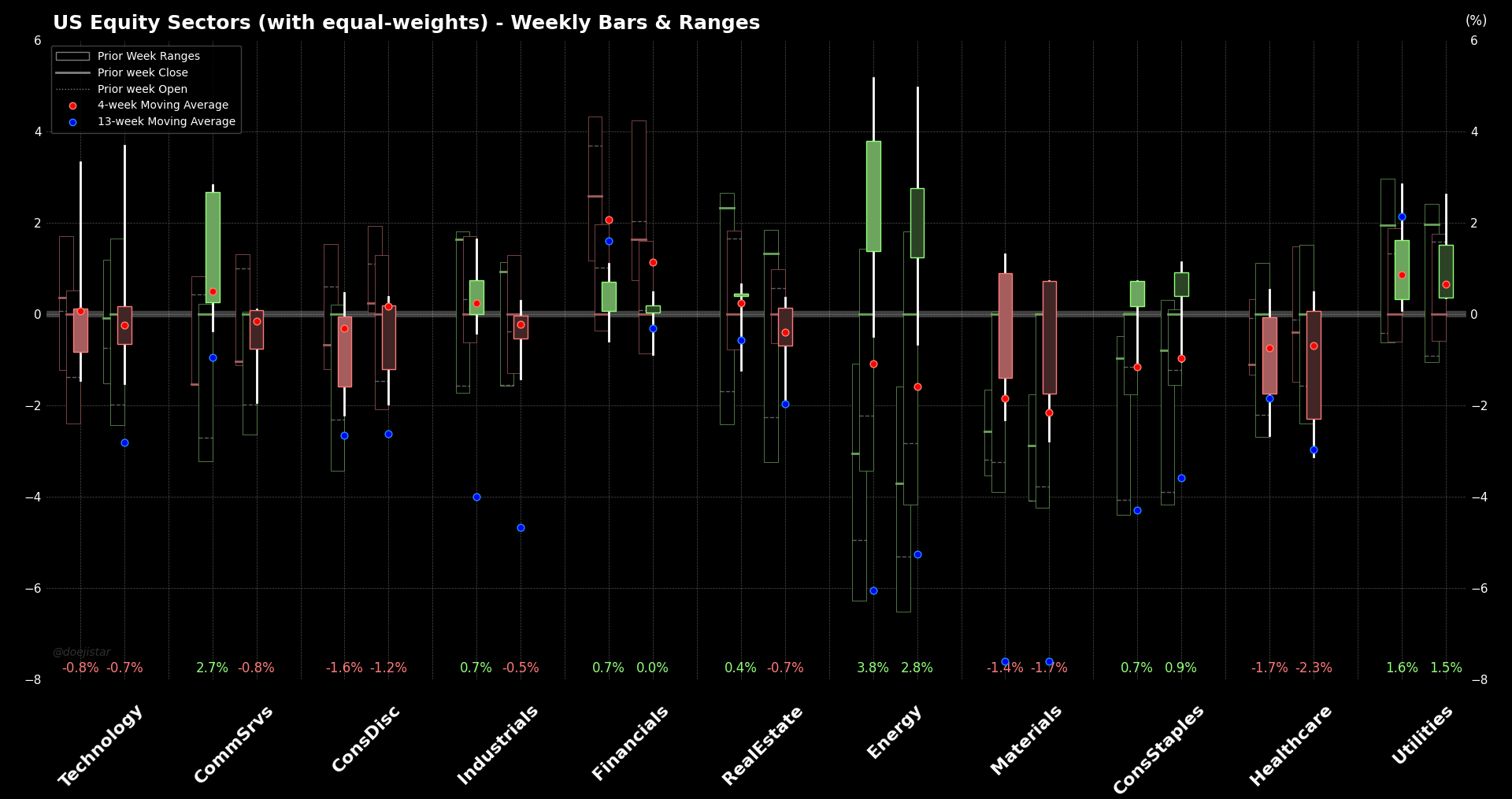

Sector profile also shows some defensive posturing with equal-weighted Utilities, Consumer staples performing well, while the strong Energy sector rally continues.

We've seen some very strong rebounds in SPX, but I think I would consider those tails - traditionally signalling buying pressure, to be misleading given the pattern of highs (red square). The upper trendline has been a great point of reference for the recent price action and each of last week's highs have printed a symmetrical double shouldered top strongly indicating a trend reversal, and probably more likely - further consolidation, but certainly not in my view an indication of strong buying pressure.

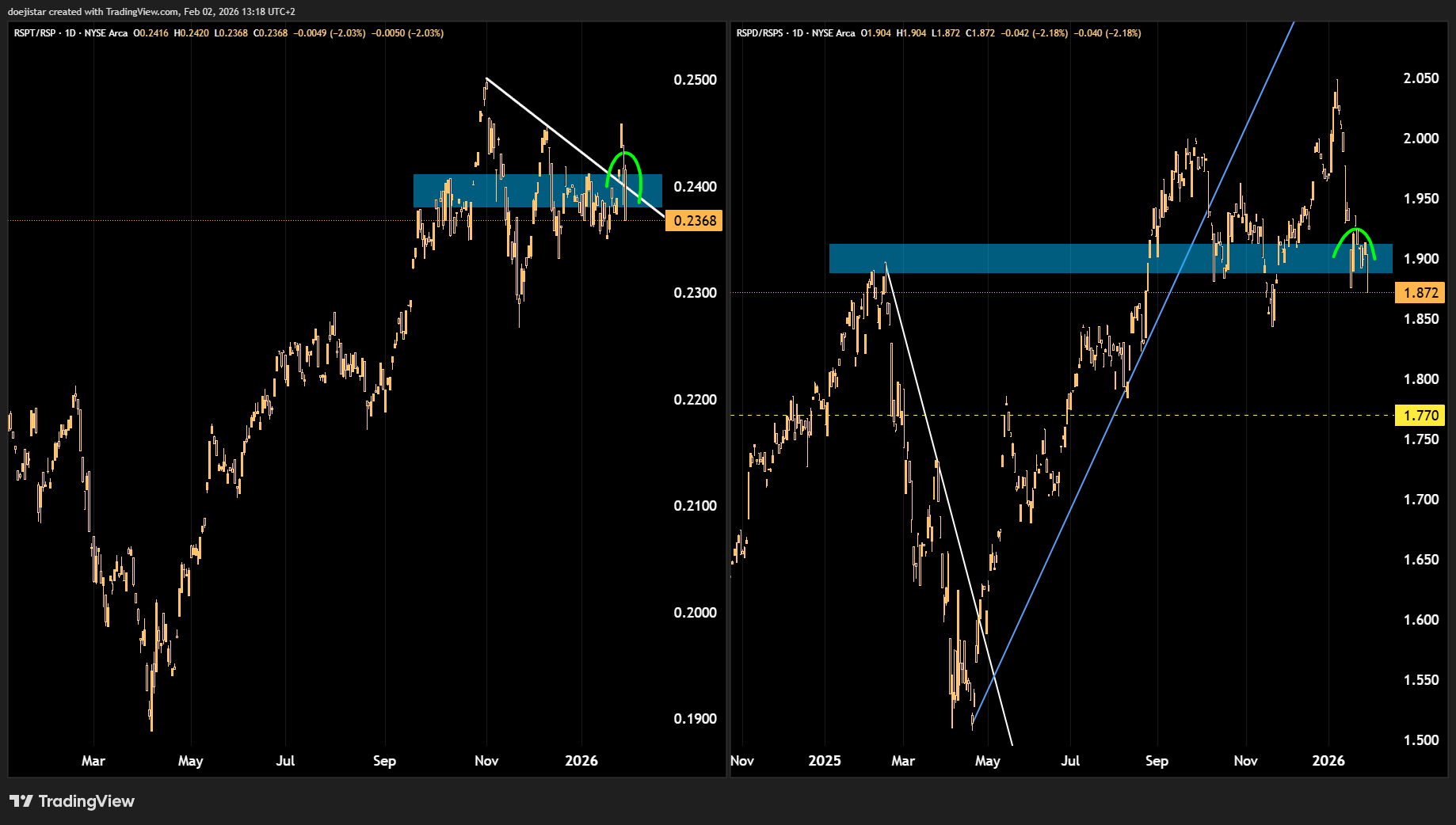

Relative equal-weighted performances of technology/spx and consumer discretionary/staples also points to weakness after the attempt to rebound has completely collapsed.

I do think we could see more of sideways chop or a slow decline however given that realised volatility isn't picking up with the rise in the implieds, which would lead to situations where the market chops back as long vol positions unwind quickly when vol spikes. To take on a view that we could see a deeper corrective leg in stocks, I would like to see realised volatility (orange line) to pick up again.

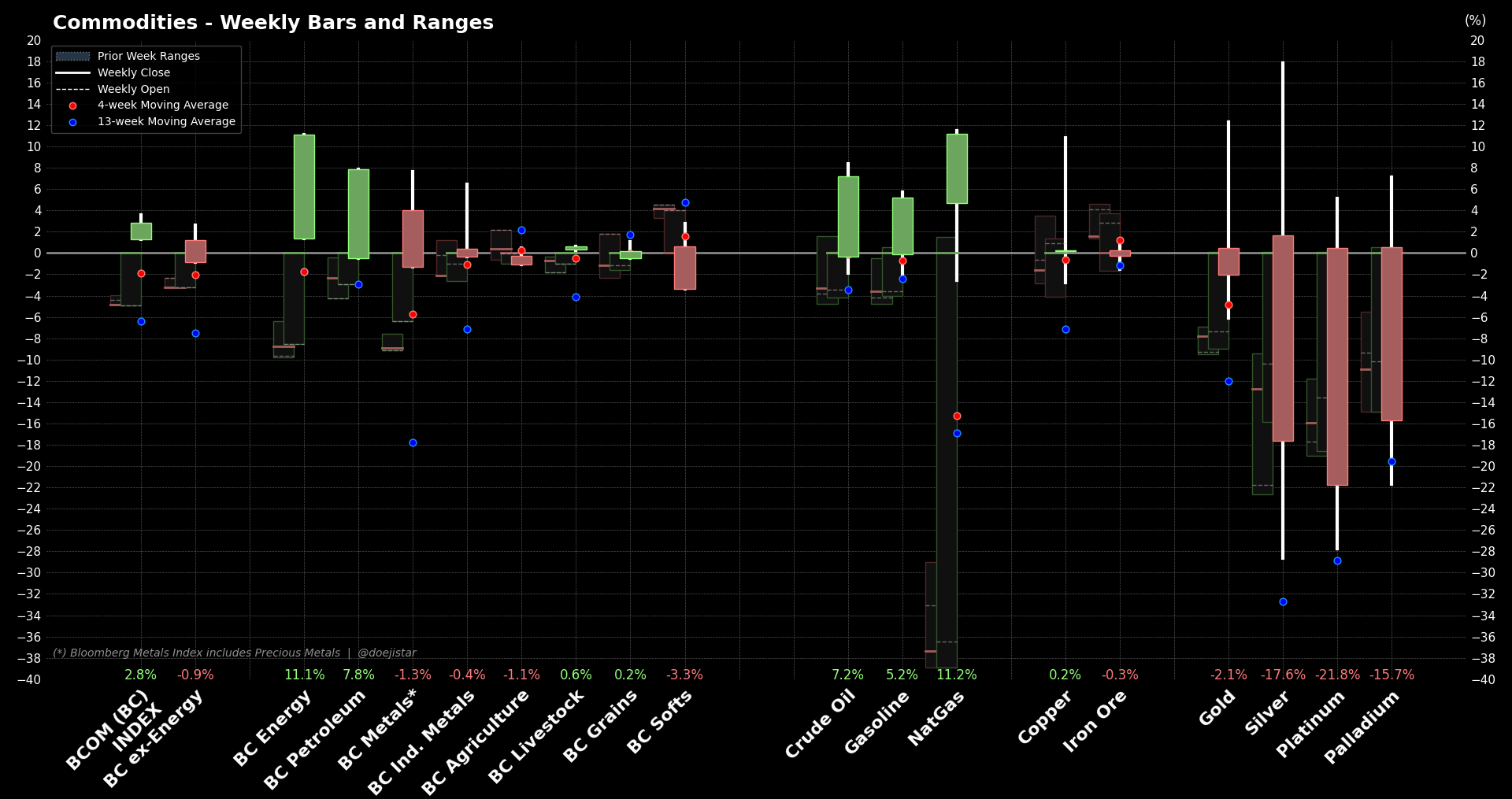

COMMODITIES

We've seen a huge unwind in precious metals last week with last week's ranges being of historic proportions. Both Gold and Silver was the 2nd highest weekly range in percentage terms, and the highest for platinum.

$XAU $GOLD 14.28% daily range... only surpassed once since 1975 (Aug1999 15.38%, overtaking the Jan1980 14.11%) pic.twitter.com/1PICaeWDAF

— Doe (@DoejiStar) January 30, 2026

Energy continued its weekly breakout despite this morning's pullback, while Precious metals printed bearish engulfing bars and selling off even further to start the new week. I do think these are opportunities to get long on both again given that I don't see confidence in Trump-related risks and Dollar returning quite so soon, and Iran risks lurking to keep the market trading with a relatively high geopolitical risk premium.

Crude has retested this key pivot level around 61.60 and this would be the perfect 'impulse-pullback' entry in consideration to the strong breakout move.

We've retested key pivot levels this morning and found decent demand just before the 4400 handle with a strong recovery above the 4600 level. Those who are familiar with my technical methods may know that I see big levels as bands - in this case the 4500 as 4400-4600, when assesssing price action. I therefore find this bounce to be very constructive and that the 4500 level has held and will hold with reasonably high conviction.

RATES & FX

Fed fund futures priced out 9.5bps of cuts last week as early reports pointed to Warsh being picked.

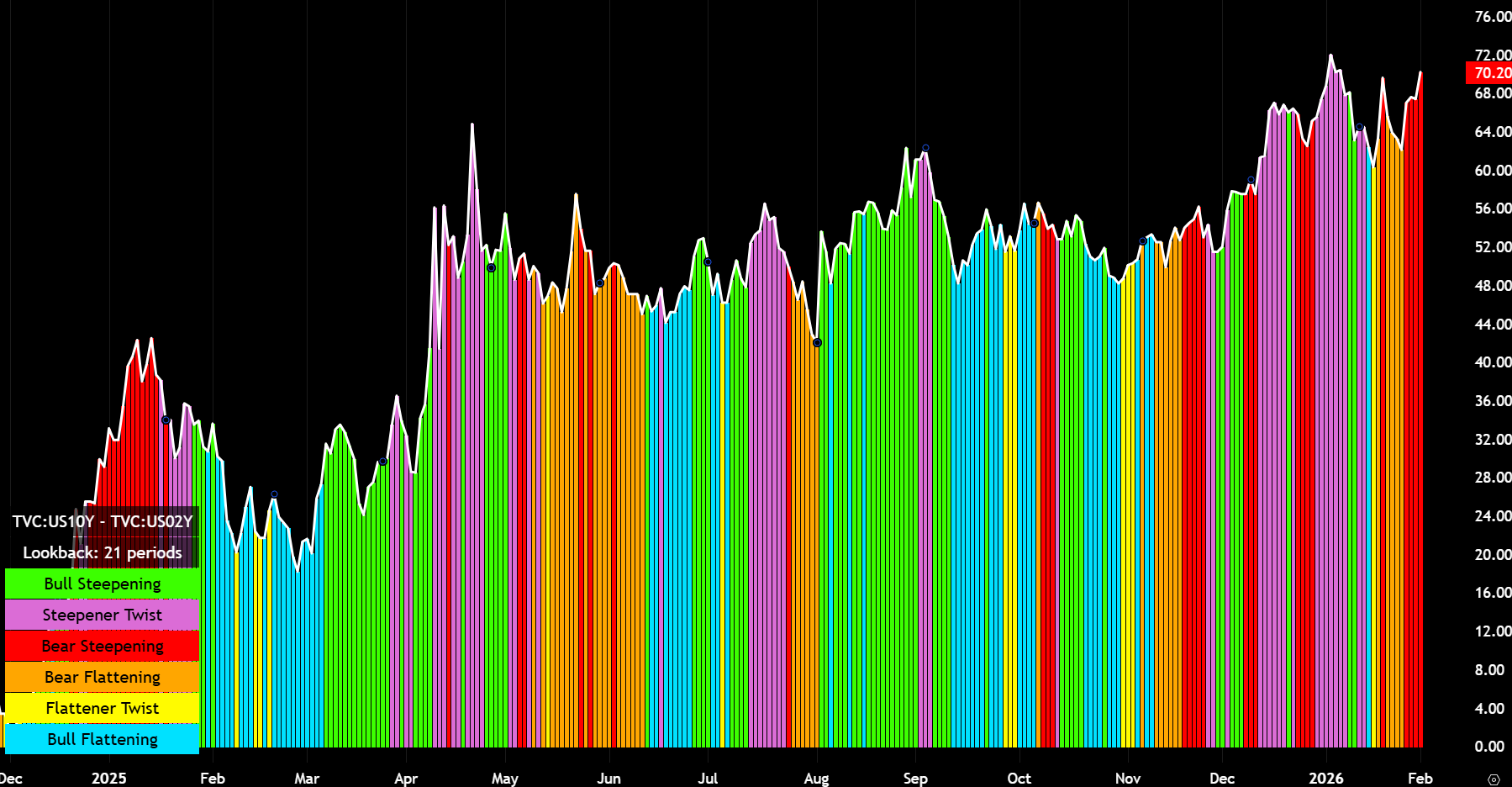

2s10s curve bear-steepened with the rebound also coinciding with those reports as he made a visit to the White House for a talk with Trump, reflecting the assumption that he will be pressuring the committee to cut more aggressively.

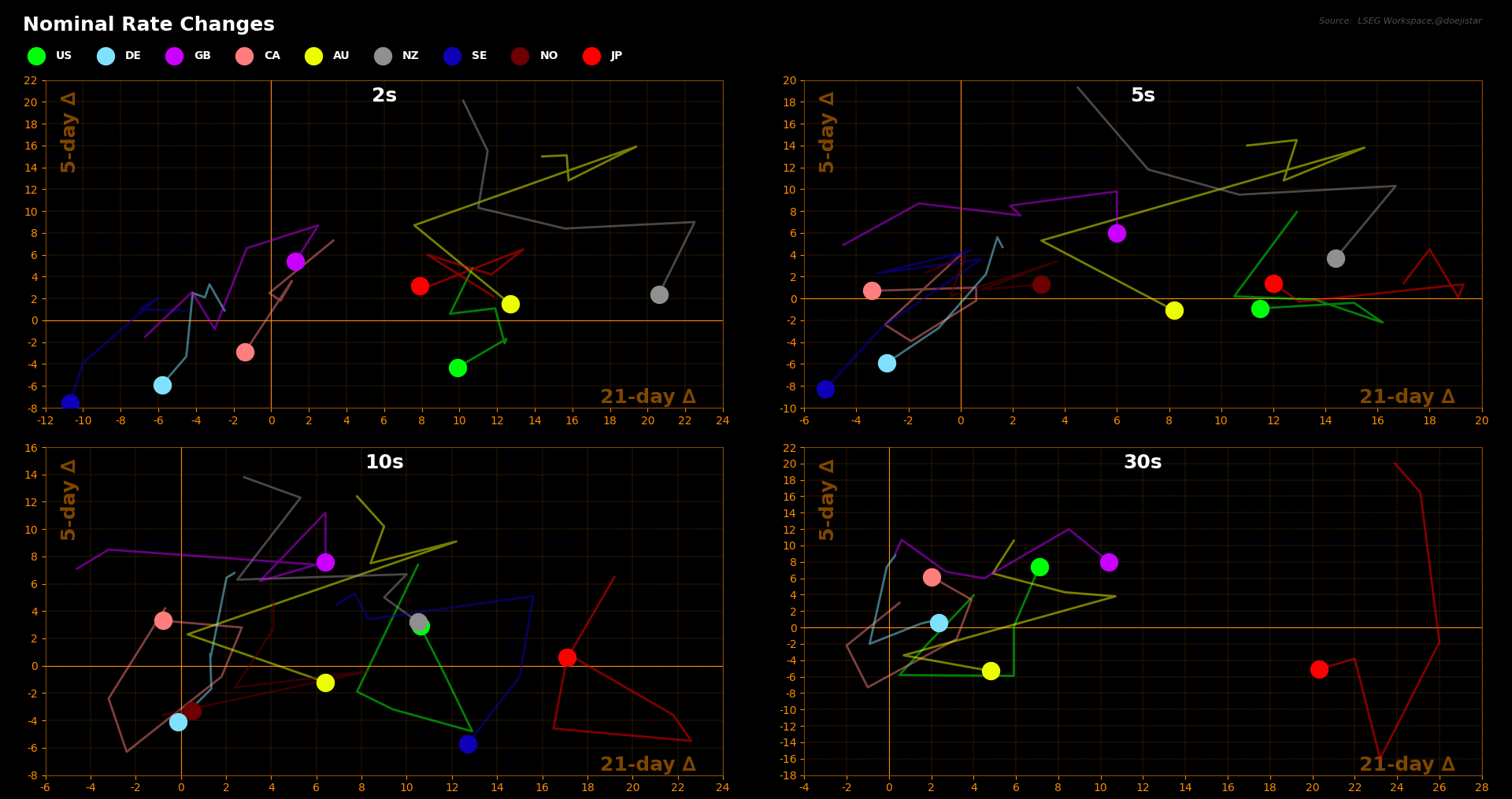

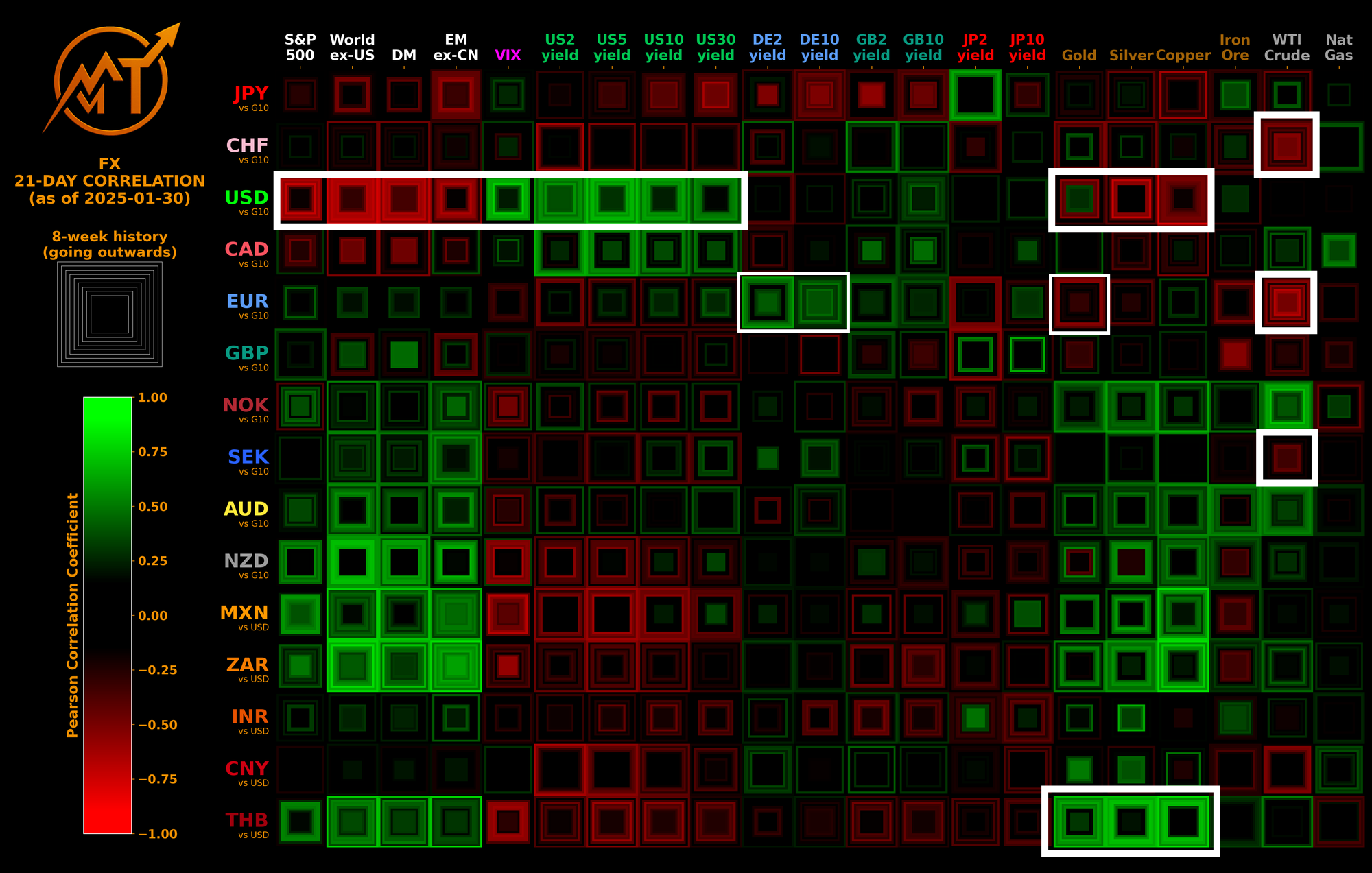

Looking at other changes in rates, Swedish and German 2year rates drifted into the negative 5-day and 21-day change lower left quadrant pointing to relative weaknesses in SEK and EUR. The US 2year also saw a 5bps point move lower last week. On the flip side, UK 2year had the most positive 5-day change, followed by the JP 2year.

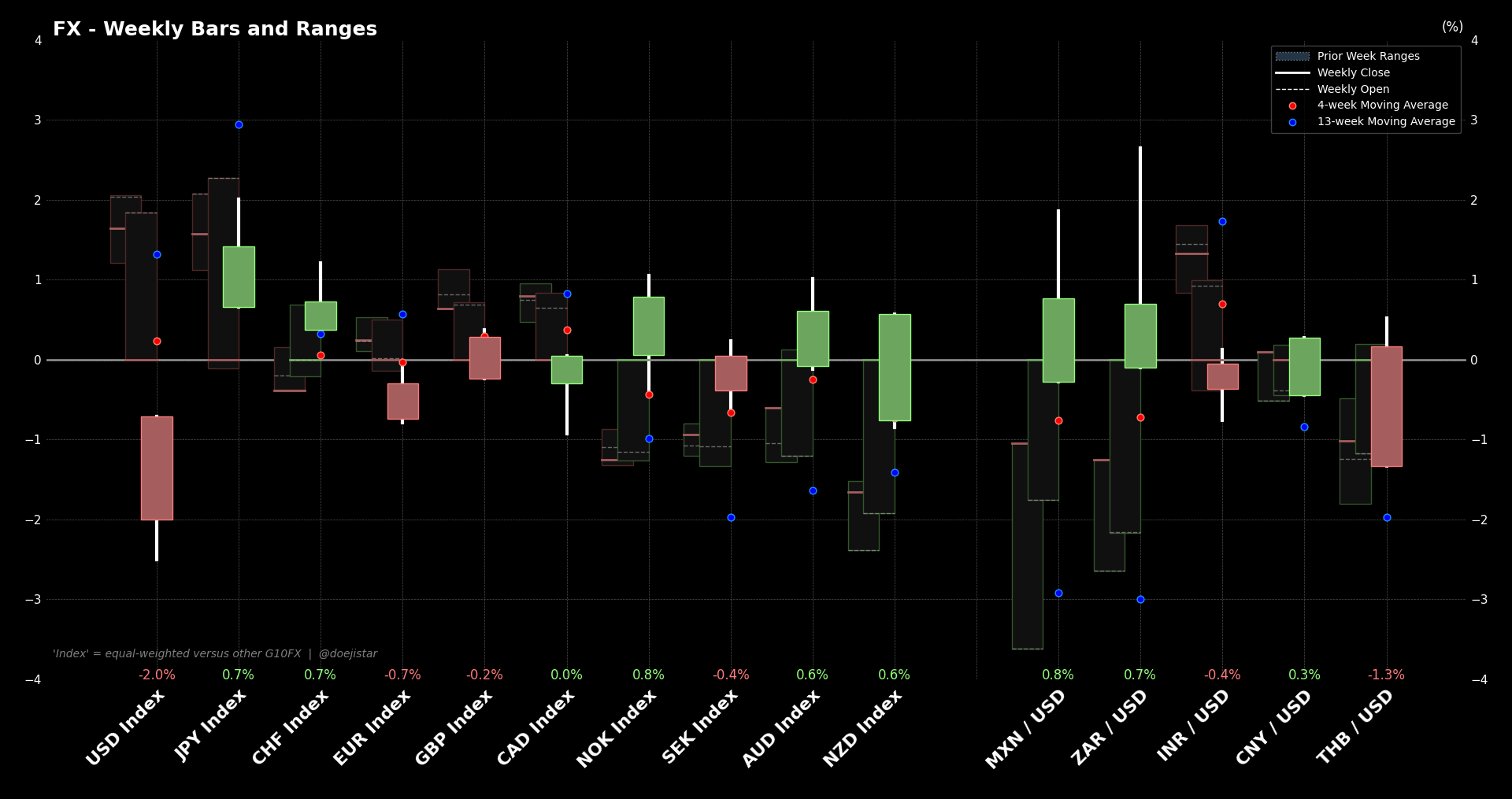

Those changes are reflected in the equal weighted performances of G10 currency indices - USD weakest, followed by EUR and SEK, while the JPY performed the strongest. THB was also very weak following the weakness in precious metals.

This also follows cross-asset correlations where we see the THB (and ZAR) typically sharing a strong relationship Gold, while EUR and SEK (and oddly the CHF for reasons unknown to me) tending to suffer from higher Oil prices.

But USD correlations have clearly gone wonky lately, losing its clear inverse-correlation to risk sentiment and positive-correlation to yields, and even its correlation to Gold in recent weeks has gone positive. This is why I'm finding it very difficult to trade the Dollar at the moment but if anything, I'm liking EURUSD shortside though I would would prefer to pair EUR shorts against something like JPY or AUD. USDSEK is another long-Dollar option I would consider. That said, not very high conviction views and it's based on Energy prices finding a rebound of which I prefer to express elsewhere. No position in FX currently.

That's all for this week, good luck out there!