Wk13 MacroTechnicals - Echoes of 2022

2022 may be a more relevant roadmap for 2026 than markets assume. Reviewing the macro and geopolitical parallels, why the Iran conflict may drag on, and which trading themes to keep in mind.

“Being early is indistinguishable from being wrong.”

— Howard Marks

This week, we examine some striking parallels between the macro-geopolitical backdrop of 2022 and the one markets face today. It argues that the current conflict is more likely to evolve into a drawn-out and unstable confrontation than a quick resolution or full-scale war, and uses a game-theory framework to assess the most probable equilibrium outcomes. From there, it turns to the market lessons of 2022 and the key trading themes that may matter again if this year follows a similar path.

2022 vs 2026

1.1 MACRO PARALLELS

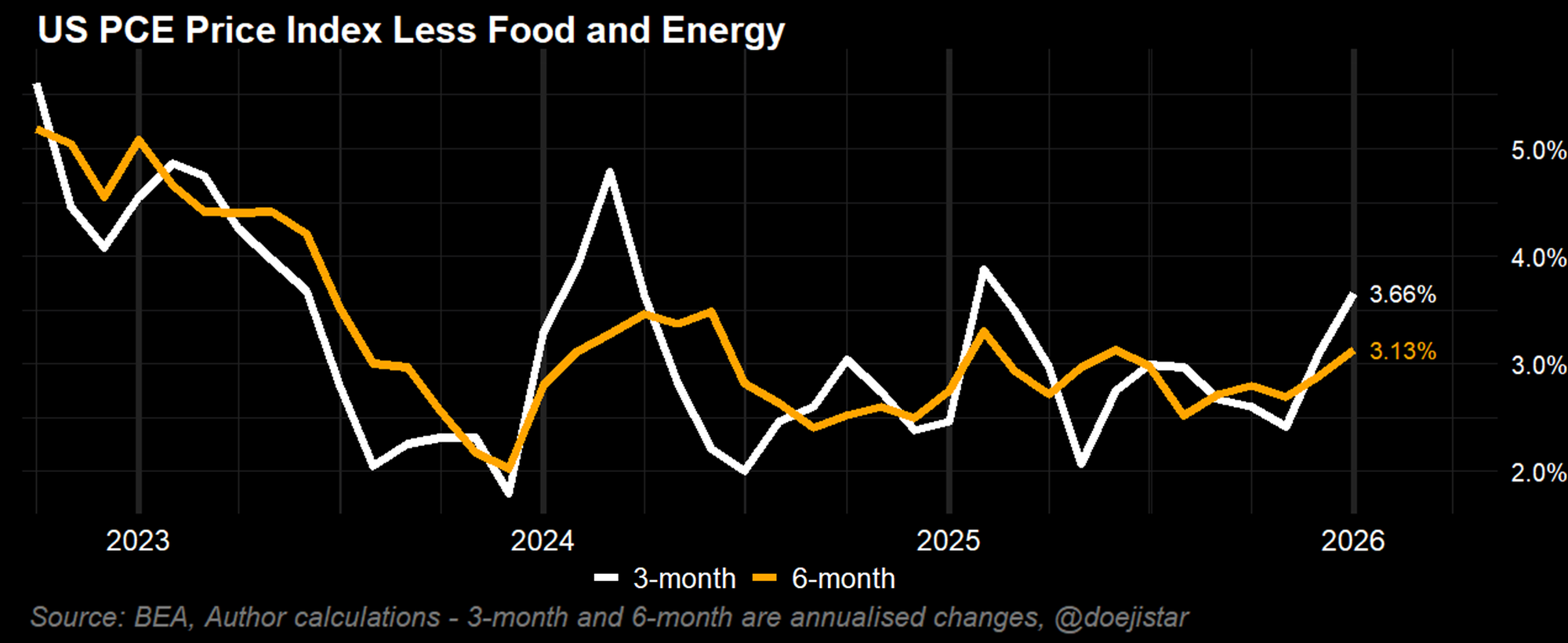

After a period of strong growth, 2026 begins with concerns about a gradual slowdown, with a stagnant labour market and rising concern over AI-related disruptions complicating the durability of the current cycle. Inflation has also proved more persistent with the 3-month annualised rate of Core PCE rising from below 2.5% in November to 3.7% in January, and the impact from the one-time price increases from tariffs have not dissipated. That leaves 2026 starting from a configuration that looks notably similar to early 2022: growth is becoming less secure, inflation is not fully contained, and markets are more exposed to a potential stagflationary impulse.

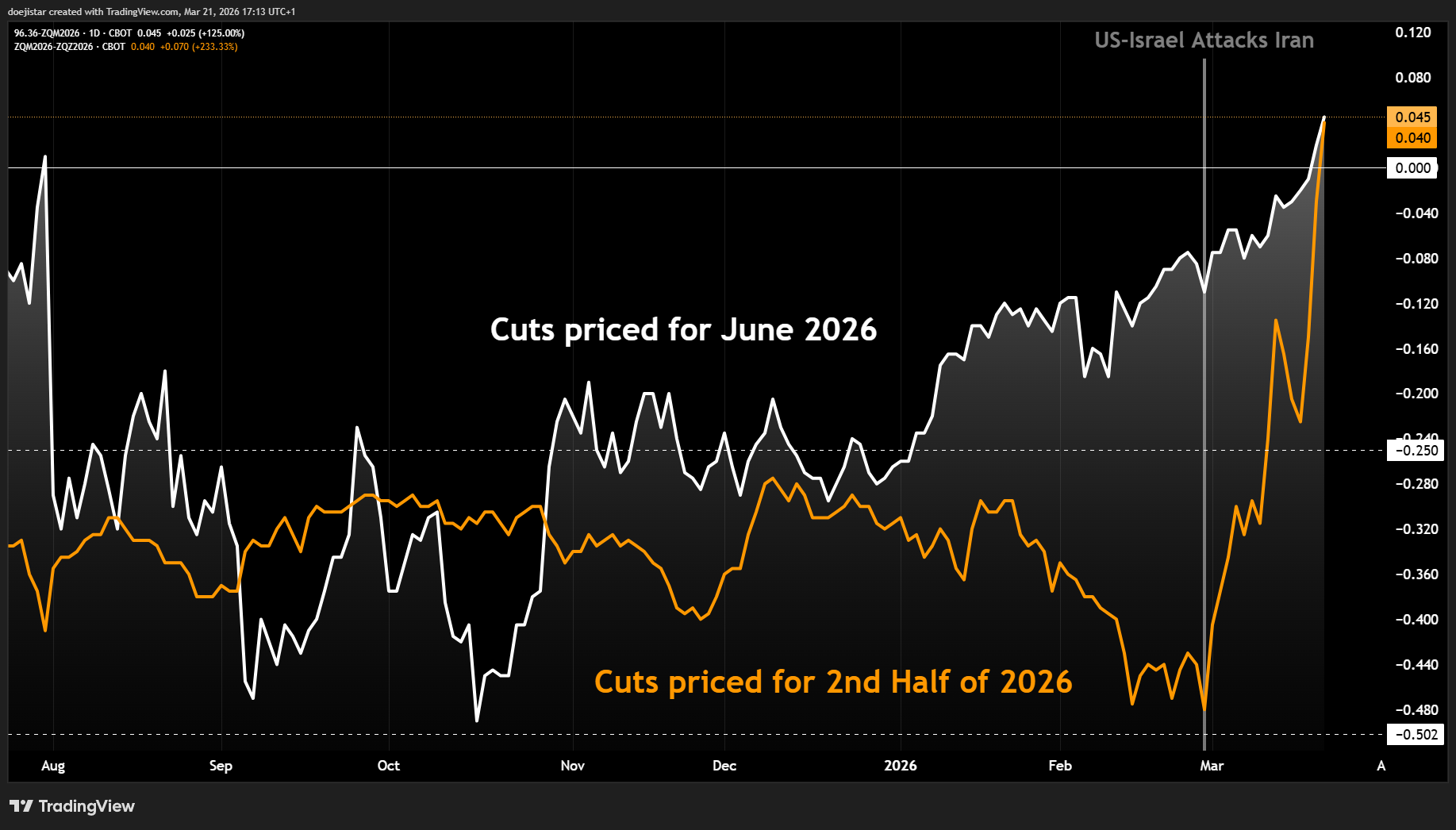

Though there was a strong bias toward further policy-rate easing this year, the market’s recent bear-flattening of the yield curve — driven by a rapid repricing from three cuts to the possibility of a hike in 2026 — also makes the policy outlook comparatively similar.

Taken together, the macro starting point looks uncomfortably similar to the one markets faced in early 2022.

1.2 GEOPOLITICAL PARALLELS

The Russian invasion of Ukraine on 24 February 2022 was a catalytic event that reshaped the geopolitical landscape in ways that still define it today, and the current backdrop bears important similarities to that period. As in early 2022, the key similarity lies in the progression from visible preparation to open conflict. Russia’s troop mobilisation preceded the full-scale invasion of Ukraine and, likewise, last year’s 12-day war could now be considered the preparatory phase of a broader conflict.

Almost eerily echoing the 2022 timeline, with war breaking out on 28 February, the conflict has already expanded through March beyond direct strikes into energy infrastructure, nuclear targets, and the Strait of Hormuz, suggesting that what initially appeared to be escalation risk has already become a wider geopolitical shock.

1.3 MACRO-GEOPOLITICAL ROADMAP

Although the first phase of the invasion largely unfolded in early 2022, the shock reverberated throughout the year as persistent energy stress and continued military conflict kept inflation elevated and growth under pressure. 2026 is beginning to exhibit a similarly uncomfortable macro-geopolitical configuration.

The resemblance to 2022 is striking, making the lessons from that episode directly relevant to the current market backdrop. The key geopolitical and macro developments that shaped that year, summarised above, should serve as a useful roadmap for how 2026 may unfold.

A Drawn-Out Conflict

2.1 CORE VIEW

Not Full-Scale War

My base case is not a full-scale invasion or all-out war. The costs are too high, especially for the US, which has little appetite for a much larger regional conflict involving open-ended military commitments, significant loss of life, and severe political and economic consequences.

Trump Too Committed to TACO

Trump has too much at stake to simply stop and walk away - the so-called 'sunk cost fallacy'. Having committed military and political capital, he now needs an outcome that can plausibly be framed as a 'win'. Reversing course too early would risk making the campaign look costly, inconclusive, and politically damaging at home, potentially to the extent that a blue sweep at the next election could come to look all but assured.

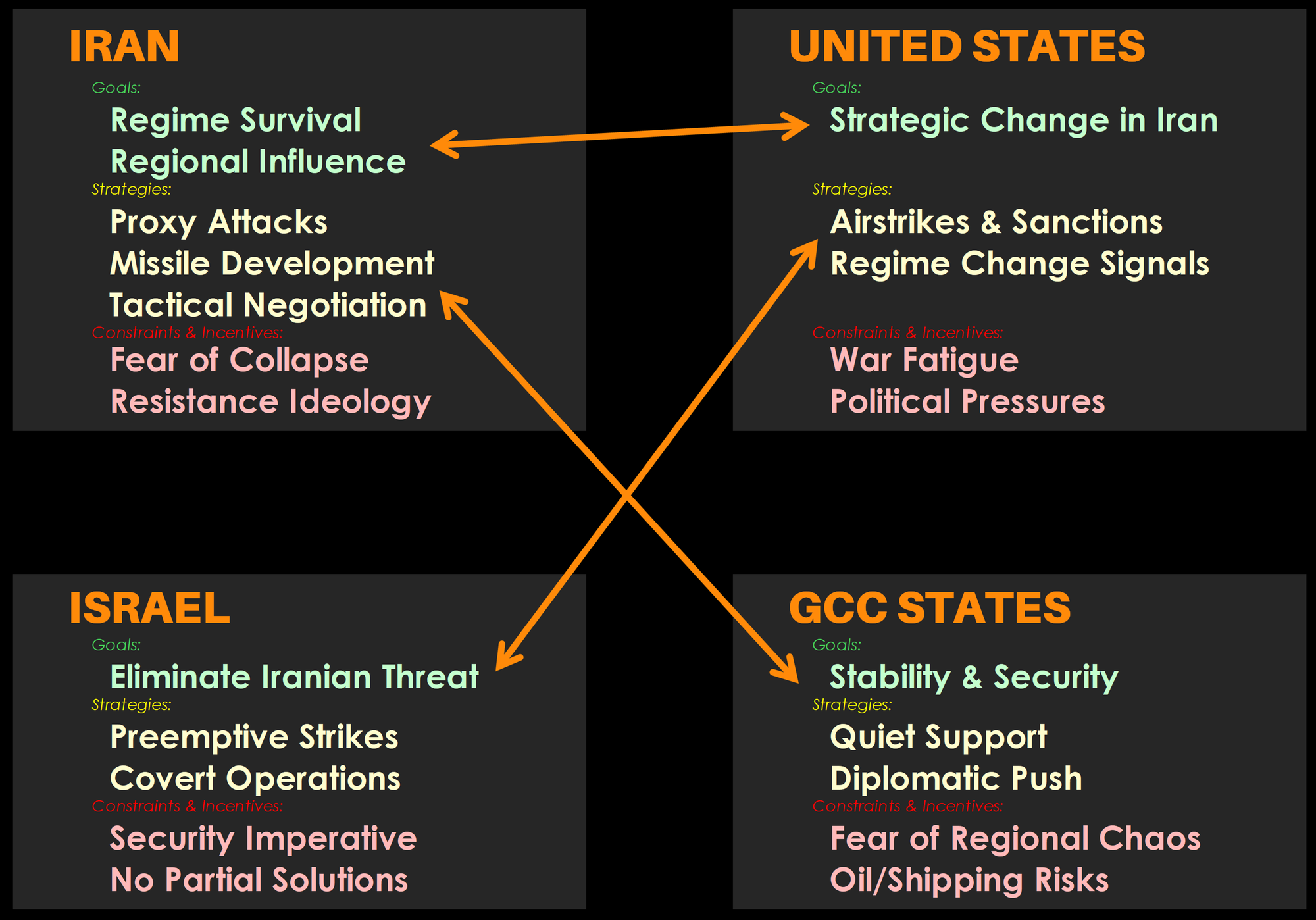

Iran Makes Threats and Demands, Not Compromise

Iran’s incentives do not point to major concessions, at least not of the kind Trump would regard as enough. The regime’s priority is survival, and part of that rests on preserving the strategic capabilities that underpin its power, including its nuclear programme. Military pressure alone is unlikely to force meaningful capitulation. Anything that resembles surrender would be viewed not as compromise, but as the start of regime collapse.

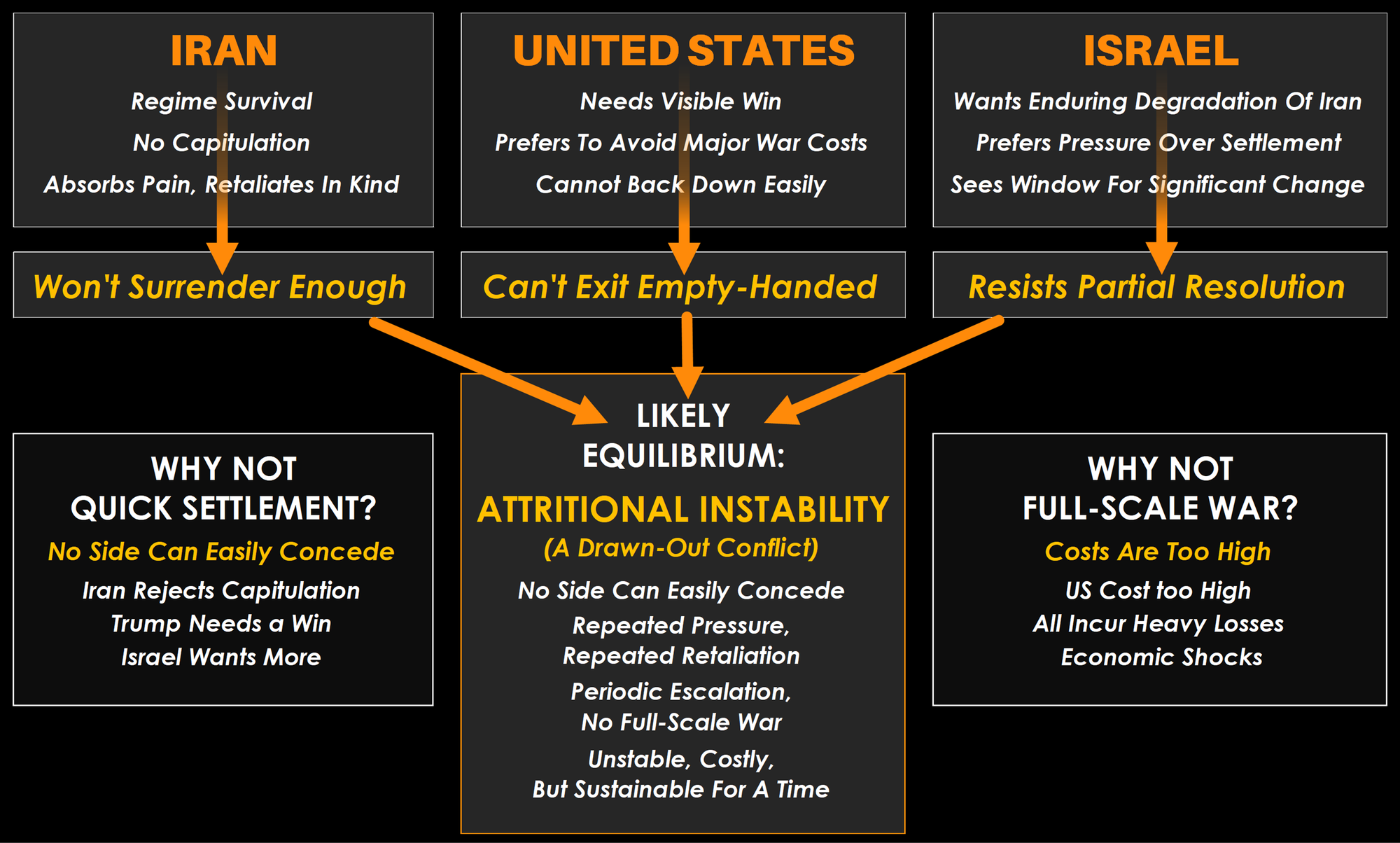

Why the Conflict Likely Drags On

The above leaves a narrow middle ground, if that. If one side cannot back down easily and the other cannot capitulate, the most likely path is a drawn-out conflict marked by pressure, retaliation, and periodic escalation. Thus, my working view is that this becomes a prolonged confrontation in which neither side can achieve its objective quickly, yet neither can afford to stop without more to show for it.

2.2 GAME THEORY POINTS TO SIMILAR OUTCOMES

Strategic Incentives

To work out each player’s likely behaviour given the expected responses of others, we need to identify the constraints and strategic incentives shaping their decisions, in addition to their motives, on which my own view was initially based. ThThe table below sets out how I see this for each player.

Equilibrium Outcome

With the motives, constraints, and strategic incentives of each player in view, the most likely equilibrium also points to a drawn-out conflict; Iran is unlikely to concede enough, Trump has too much at stake to back down without a 'win', and Israel is unlikely to be satisfied by an incomplete outcome.

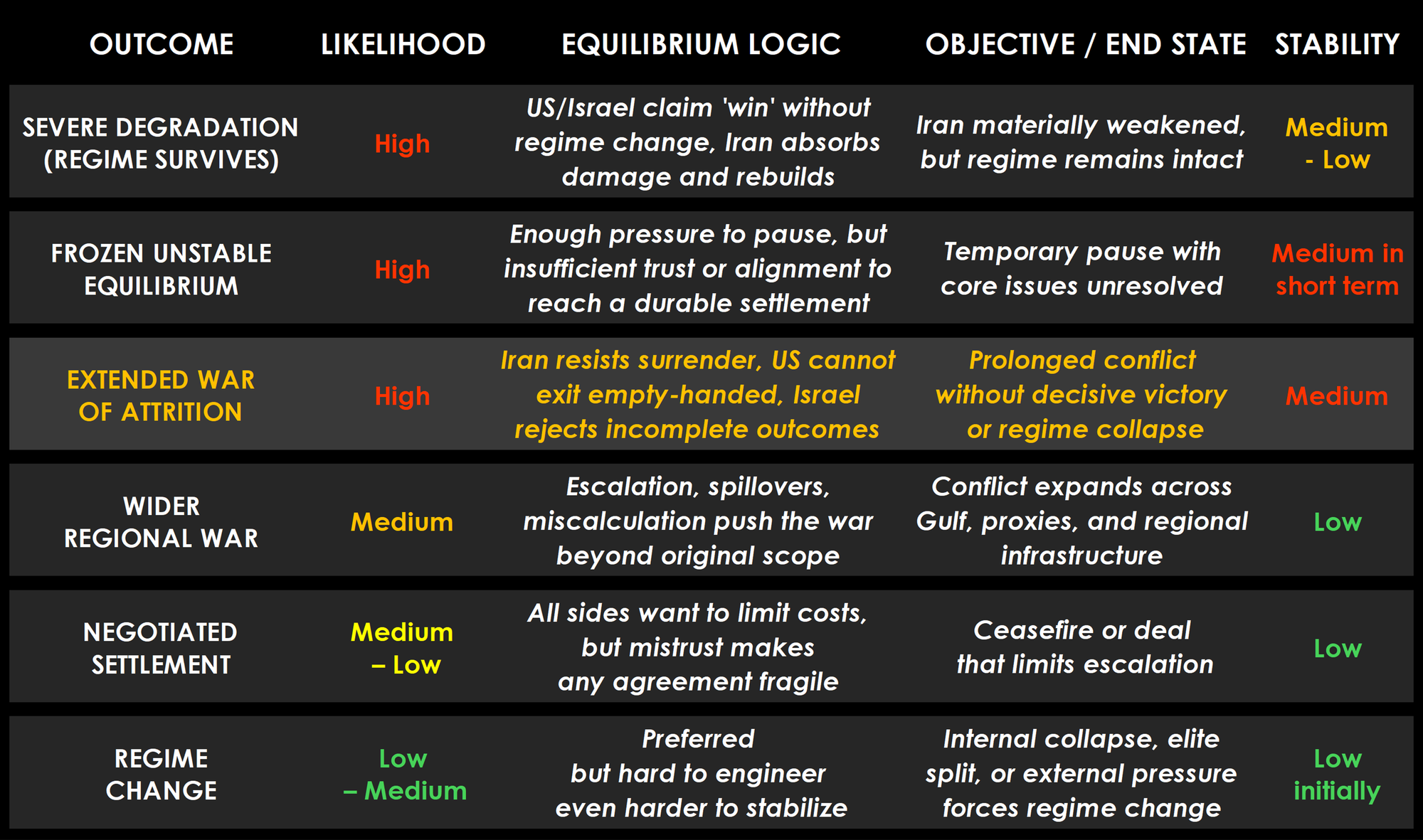

Alternative Outcomes

The table below summarises the main end states the conflict could produce and their assessed likelihood and stability.

Taken together, the table reinforces that the most likely paths are not the cleanest ones, and that a prolonged conflict is the expected outcome across multiple scenarios. The most probable path remains an Extended War of Attrition, consistent with both my own thesis and the game-theory framework. The other high-probability alternatives are Severe Degradation, which would involve intensive military action without regime change, and a Frozen Unstable Equilibrium, which would imply a pause in active conflict but with underlying tensions and military risk remaining elevated.

2.3 THE GAME BEHIND THE GAME

Taking a line from Public Enemy's "He Got Game" soundtrack, the key question is: what is the game behind the game? The visible conflict is one thing; the deeper contest is the incentive structure underneath it, which could, in game-theory terms, shift the equilibrium outcome if one or more players showed a material change in incentives, constraints, or perceived payoffs. Based on the framework established above, that could come from:

- a credible off-ramp that gives Trump a visible win,

- a change in Iran’s willingness or ability to resist, or

- a change in Israel’s or GCC’s tolerance for a prolonged conflict.

That underlying framework looks largely intact, and the deeper game has not yet changed or been revealed by any party in a way that would break the equilibrium outcomes mapped out above. That leaves the conflict still biased toward duration, instability, and an uneasy absence of resolution.

2022 Trading Themes

If the geopolitical base case is a drawn-out and unstable confrontation, the next question is how markets are likely to trade that path. The key point is that markets do not need full-scale war to face meaningful stress. A prolonged conflict, severe degradation, or even a frozen but unstable equilibrium would all be enough to keep pressure on energy, inflation expectations, trade finance, and broader risk sentiment. It is therefore worth reviewing the trading themes that performed best in 2022.

3.1 EQUITIES

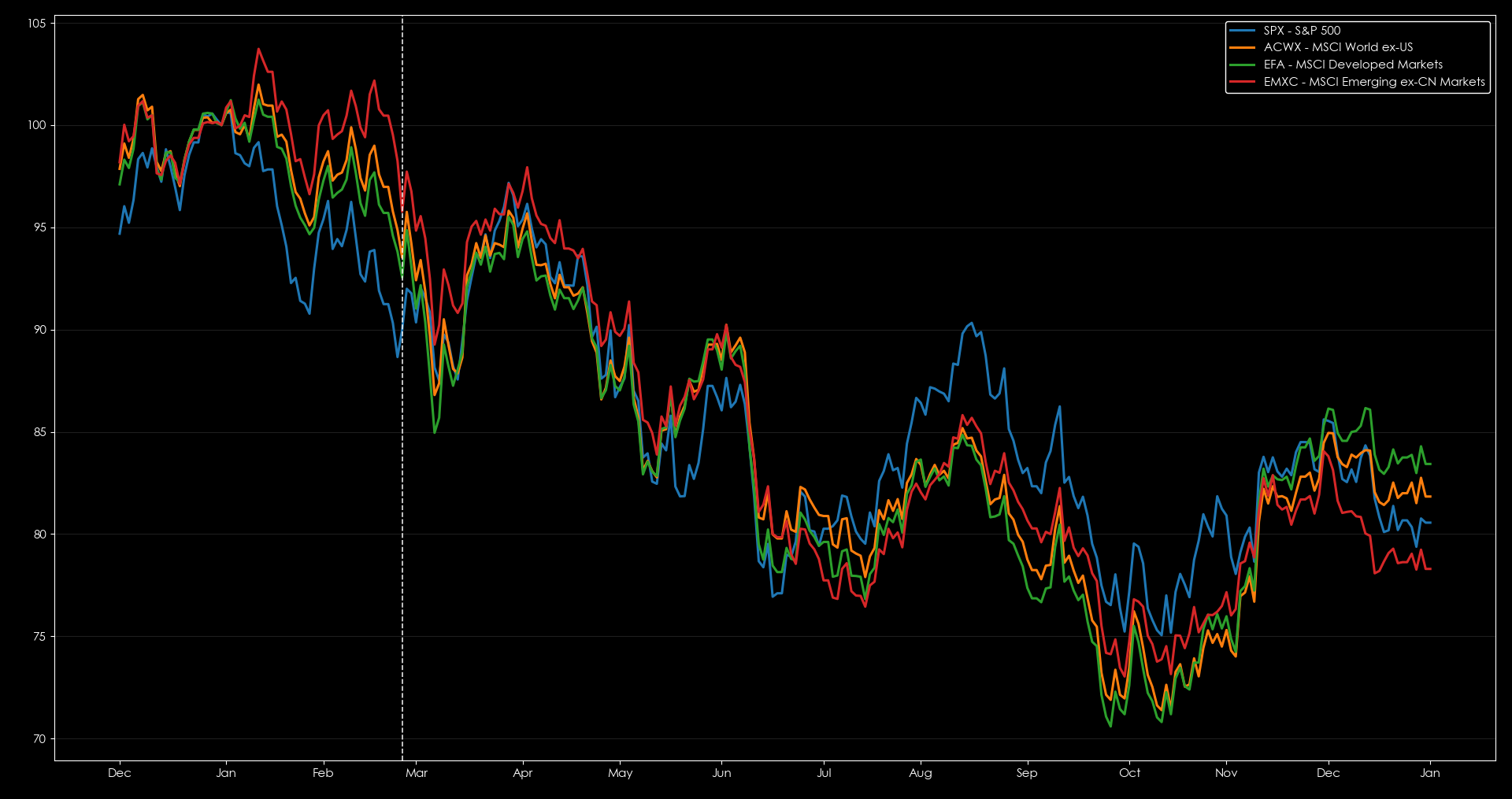

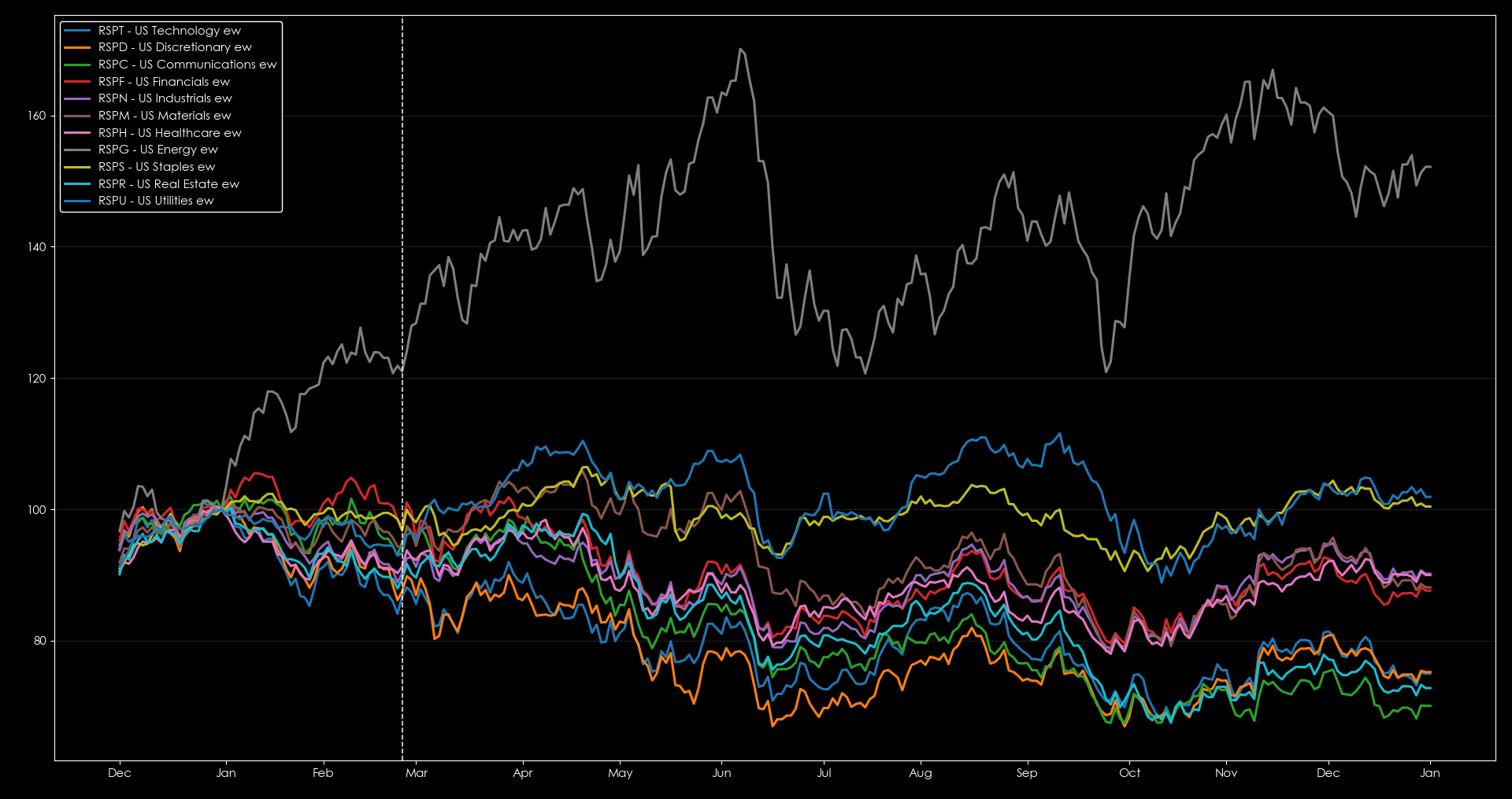

Equity markets were clearly in a risk-off mode in 2022, with the market entering a bear market in June before recovering in late November.

US sector equal-weighted performance shows the high-beta Technology, Consumer Discretionary, Communications, and Real Estate to have been hit the most, while Energy was the only sector in positive territory, and defensive Utilities and Staples held relatively steady.

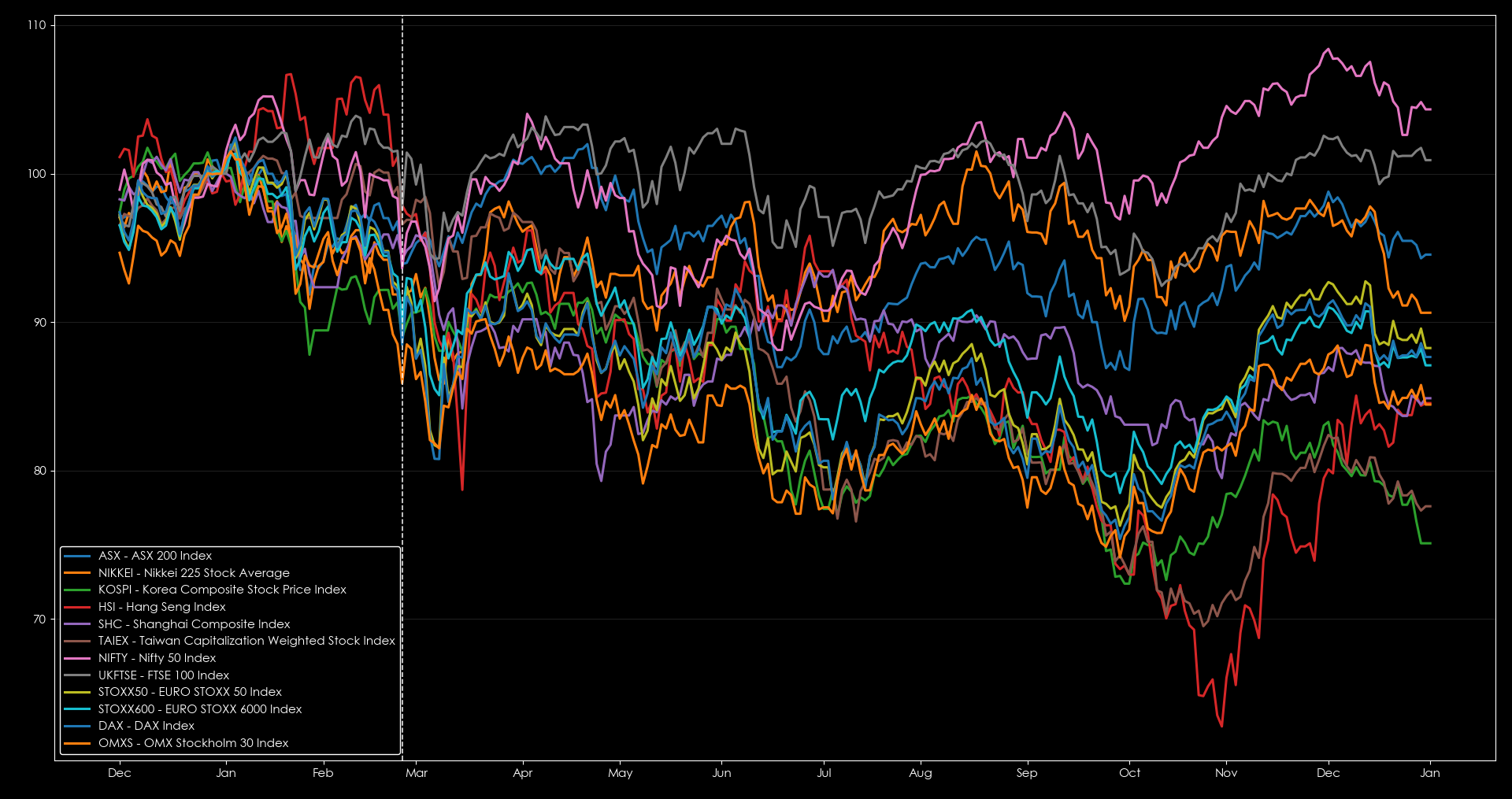

Asian markets were the worst hit, and European equities did not fare much better, and only India's NIFTY and UK FTSE held steady during that tumultuous period. Interesting to see that the NIFTY had performed relatively well during that period given recent reports of ships destined for India transiting through the Strait of Hormuz.

The performance profile of 2022 would suggest long Energy / short Consumer Discretionary in US markets, short SPX / long VIX at the index level, and long NIFTY / short KOSPI (or Nikkei) in global equities as the main themes.

3.2 COMMODITIES

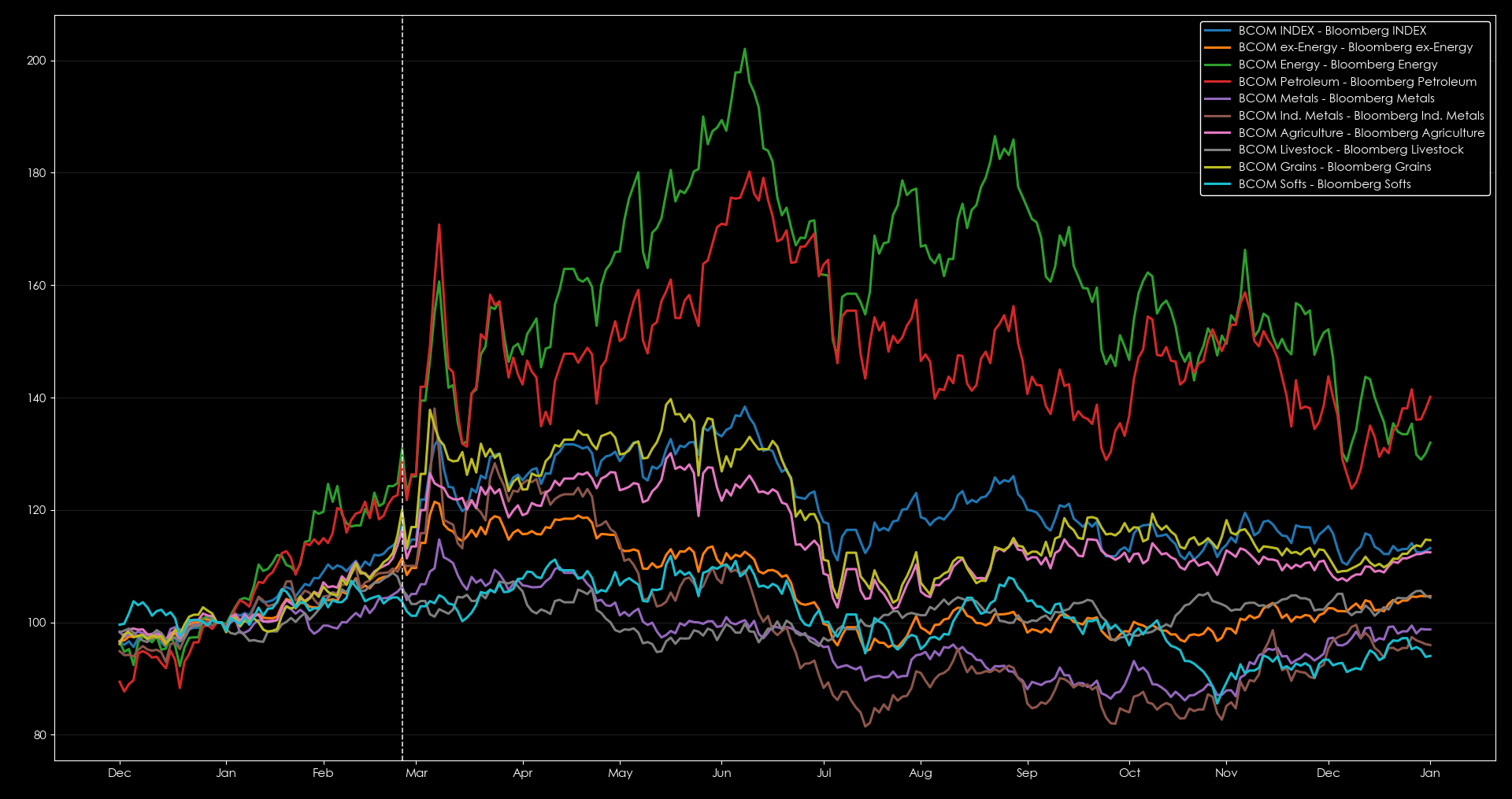

Commodity markets held relatively steady, with Energy as the clear winner. Grains and agriculture also held gains for most of 2022, while industrial metals saw the biggest fall from their March peak. That performance suggests long Energy / short Copper as the theme to watch.

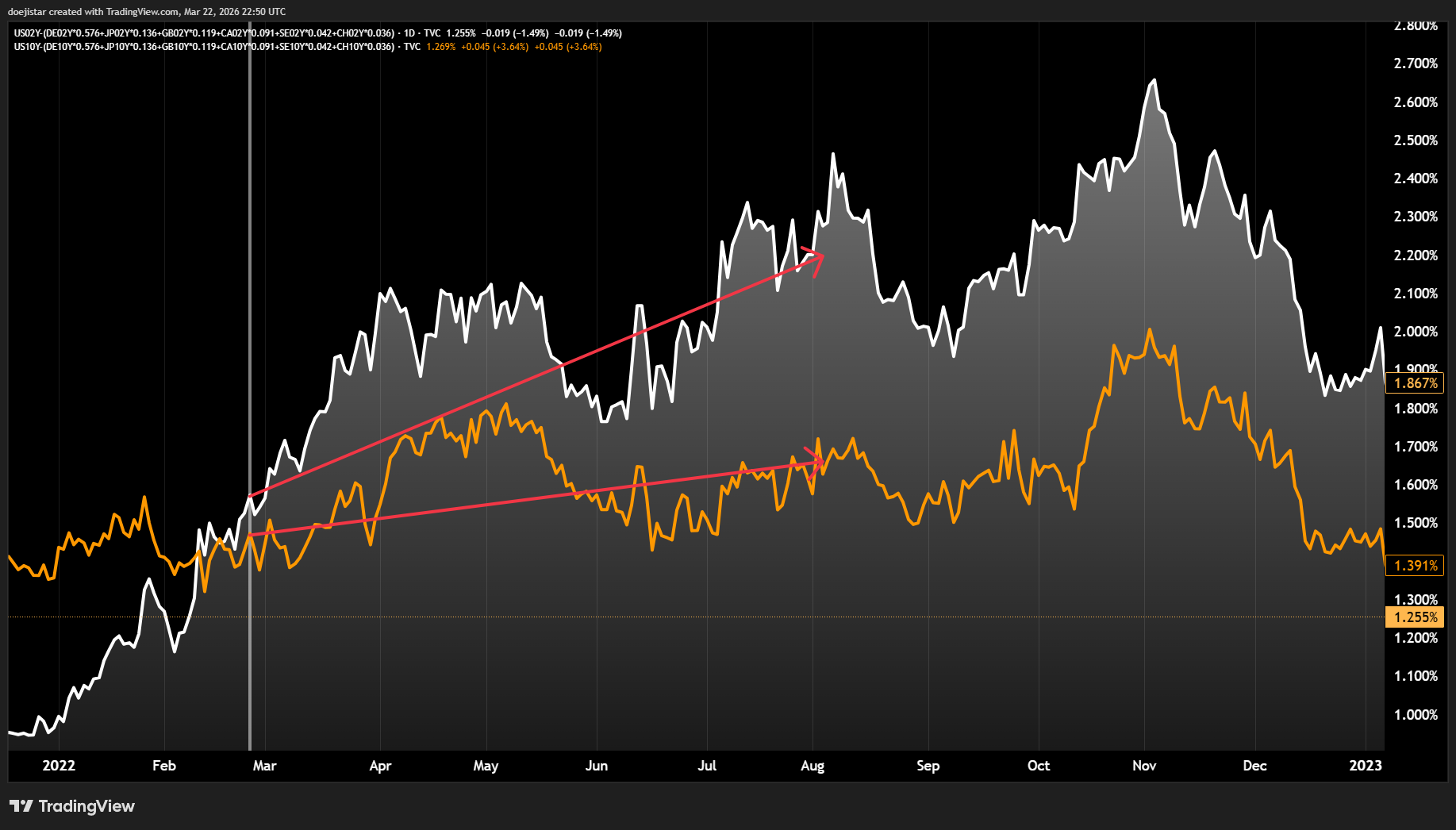

3.3 RATES & FX

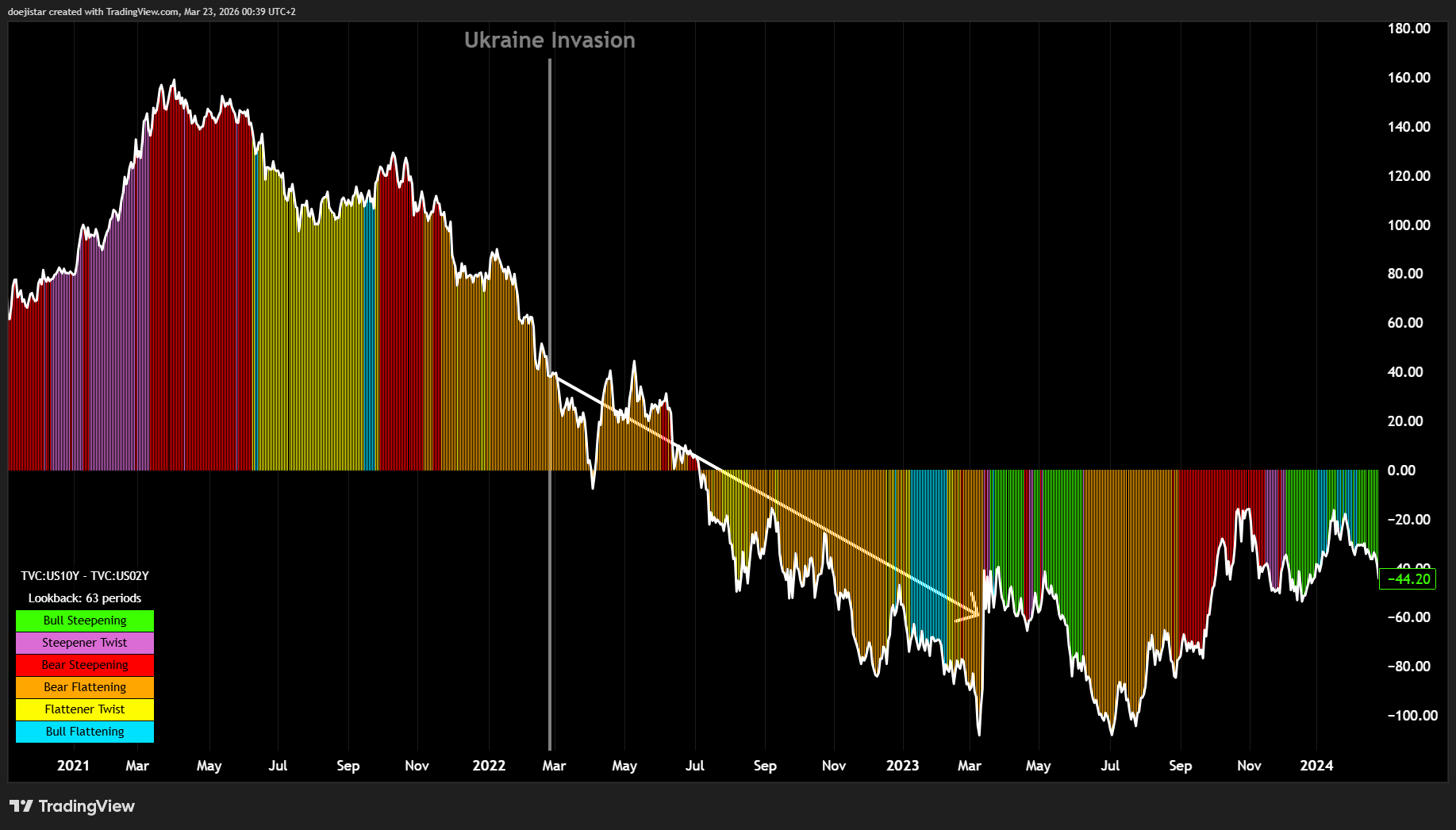

In US rates, we saw a Bear-flattening regime through 2022 which is understandable, as the Fed was embarking on a hiking cycle after a QE-fueled cycle of 2020-21 that was accelerated by surging Energy prices.

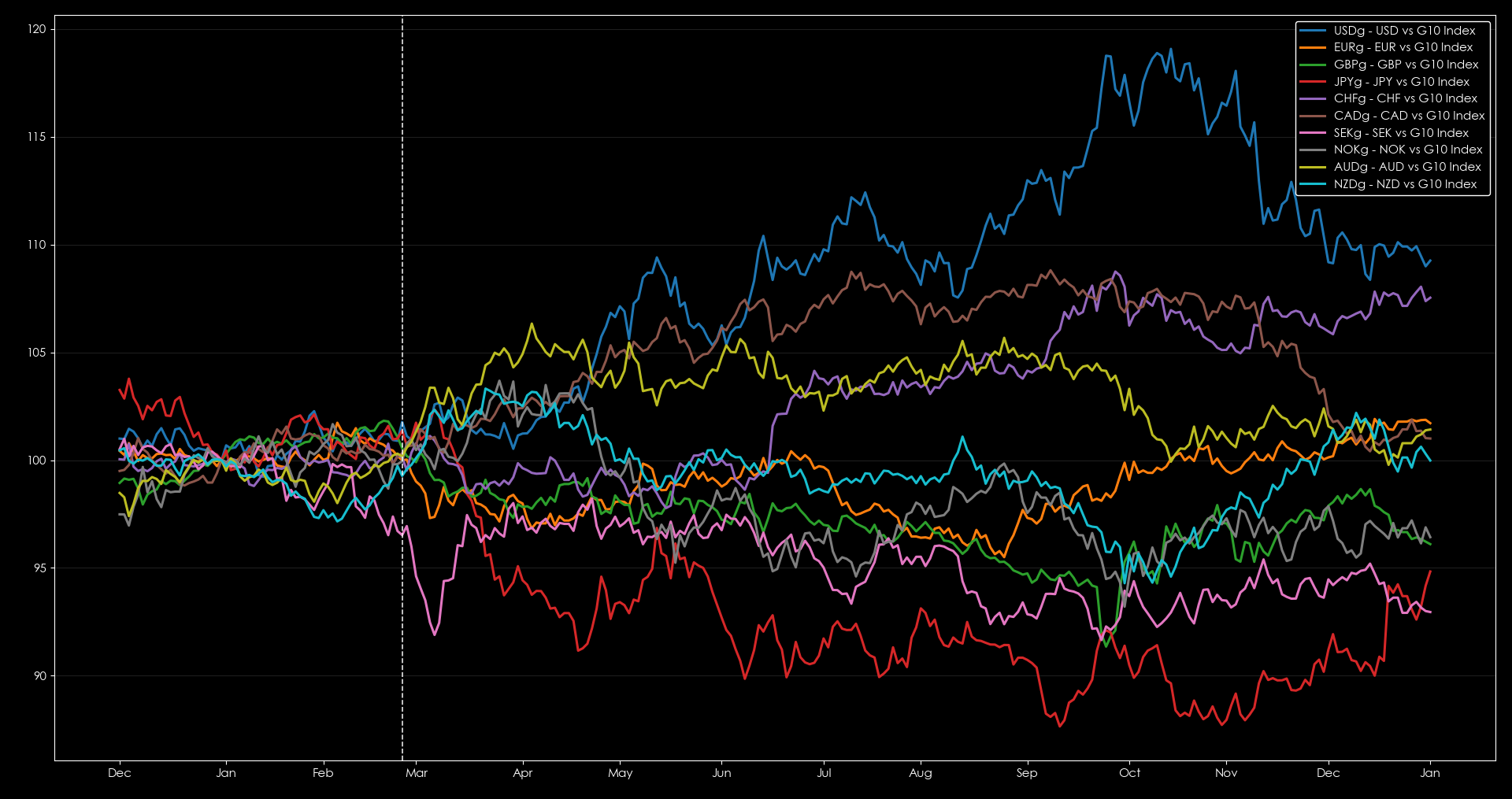

DXY-weighted rate differentials moved favourably toward the US dollar.

The dollar was a clear winner throughout 2022 until we saw a re-steepening in the US yield curve at the end of the year. CAD was a strong performer, as was the CHF later on, and JPY was a notable loser. Lessons from 2022 would point to long bear flatteners and long USD / short JPY as the key themes to focus on.