Wk12 MacroTechnicals - If Iran Stands, Trump Doesn't

Stagflation risks are building and reshaping the macro regime. We assess the current backdrop to examine whether these conditions could be short-lived or likely to persist.

I have felt somewhat alone on my bearish convictions the past week given that many of whom I had discussions with, have been buying dips and fading war-risks. And against the big cohort of those who have turned tactically bullish last week, my view has proved corrected, at least for now. Can I prove to be correct another week, or two? I've no idea, but I do think I have a solid case for why it is difficult to be fading these risks so soon, of which I'll outline below.

We'll jump straight into the consequences of a conflict that I find structurally near-impossible to resolve, the stagflationary pressures now re-entering the macro picture, and how that can complicate the policy outlook to keep central banks 'trapped' - many of which have meetings this week and who tones I expect to lean cautiously hawkish.

Macro

IRAN WAR

Some major developments this past week:

- Khamenei's son Mojtaba becomes new Supreme Leader. Thought to be even more of a hardliner than his father, and if that wasn't enough, Israeli airstrikes killed not only his father but his wife and brother. The most recent reports suggested he has been injured from airstrikes but lives.

- Iran attacks Oil infrastructure of neighbouring countries. Attacks have forced suspension of production, refinery and ship loading operations including - Ras Laffan LNG in Qatar which is the World's largest LNG plant, Ras Tanura which is Saudi's largest refinery, a refinery in Bahrain, and the port of Fujairah, the biggest oil trading hub to where Oil can be rerouted to as a way to bypass the Strait of Hormuz. The hit to Fujairah was in retaliation to US/Israel strikes on Kharg Island that included 90 military targets but spared oil infrastructure "for decency".

- Iran continues to issue new threats. Iran threatened to continue its oil blockade until the attacks end while US/Israel escalated strikes, as well as telling the World to get ready for $200 Oil. Iran also said it would be ready for a Truce should Israel/US stop their attacks.

- Trump: War could end soon, far ahead of schedule, deploys Marines. On Friday, Trump said "Strikes increasing. Today will see the highest volume yet" and a 3rd carrier USS George H.W. Bush with 2500 Marines will be deployed to the area.

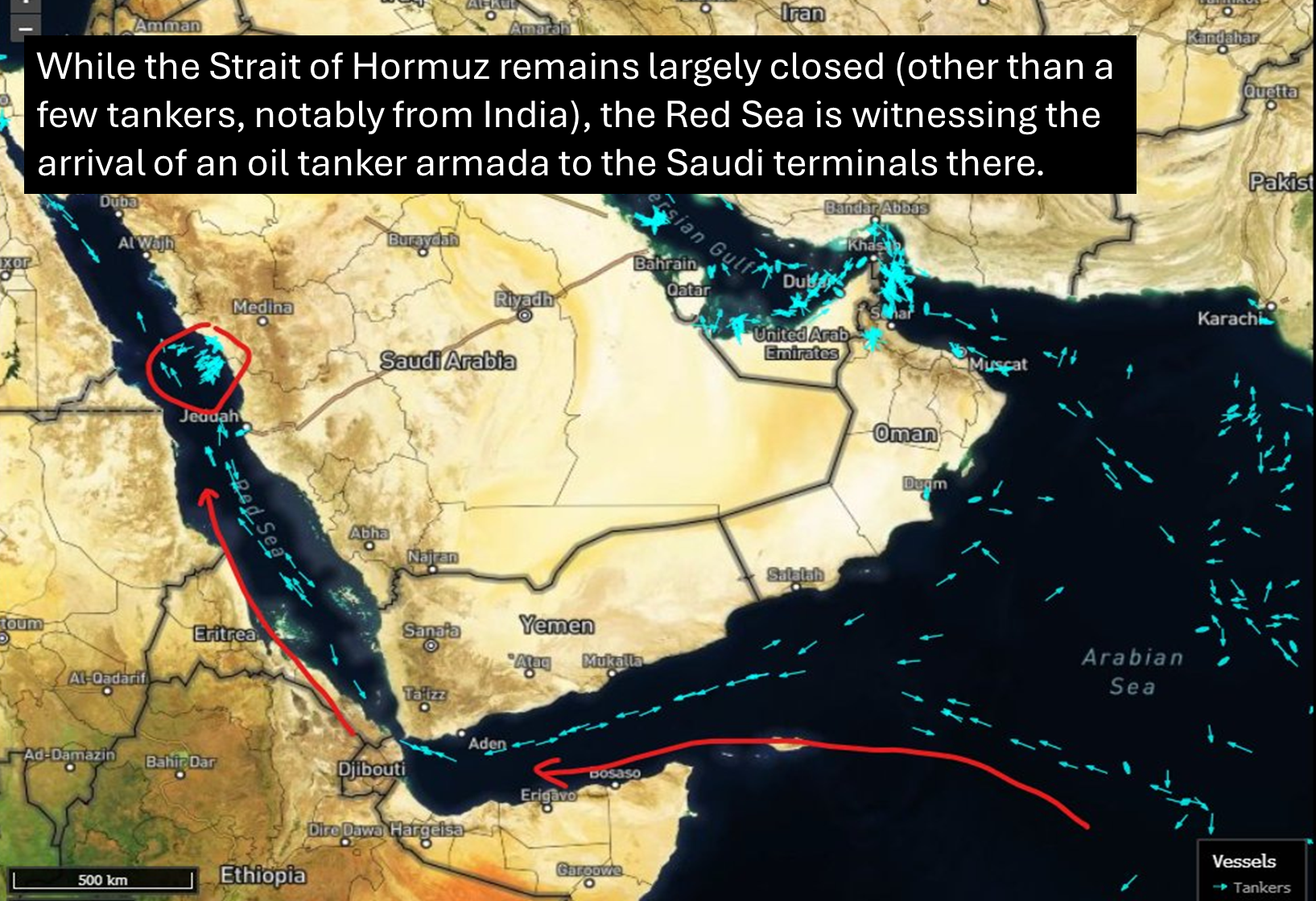

- Ships are passing through the Strait of Hormuz. Reports as early as last Tuesday asserted that Chinese bulk carriers and a Greek oil tanker have passed through the strait, and in more recent days - TankerTrackers.com observes oil has been transported out through the Strait. Javier Blass also reports that tankers are opting for the Red Sea terminals:

Gaming out the motivations of each party:

When it comes to geopolitical matters, I find the best approach to the many questions and scenarios is to attempt at understanding the mindset and motivations of each party. For instance, there is a reason why Zelenskiy has played hard ball with a peace deal (I'm not giving up land that is rightfully ours); why the BOJ has been very slow to normalise policy (we have a severe case of deflationary PTSD and want to foster wage-inflation). Let's attempt to dissect those motivations on either side of this conflict:

1) US/Israel mindset - regime change and to bring the opposition to power. After 8-10k+ sorties (at ~$20-30 billion cost to US taxpayers), the tactical retreat would be a strategic defeat. Both Trump and Netanyahu need a decisive win to justify their efforts and the only real acceptable off-ramp, is a "regime change". It could not be any simpler or more obvious than that. Because....

2) Political calculus points to the conflict being far from over: The most politically damaging thing that Trump can do now is to TACO and effectively abandon victory. Domestic polls show 27% support goes to 40%+ if "mission accomplished" is declared. A regime change is quite simply the best political outcome for Trump as well as it would be for Netanyahu.

3) Iran's IRGC wants continuity, regime survival. This is completely opposed to the very thing that the US-Israel coalition hopes to engineer as a way to vindicate that their aggressions.

In simplistic game-theory terms, the payoff/benefit structures to each party means that the conflict is likely to persist longer because the cost of a compromise is untenable to both sides. In other words, deescalation is not the natural equilibrium according to basic game-theory - IRGC won't accept a situation where they do not stay in power, and US/Israel have increasing incentive to pursue a decisive result for political vindication, and even political survival with respect to the Republican party. There simply isn't a scenario where the optimal cost/benefit of both sides can meet and until an alternative face-saving equilibrium emerges that allows both sides to sell an outcome as a success; the latter of which isn't quite foreseeable for the time being.

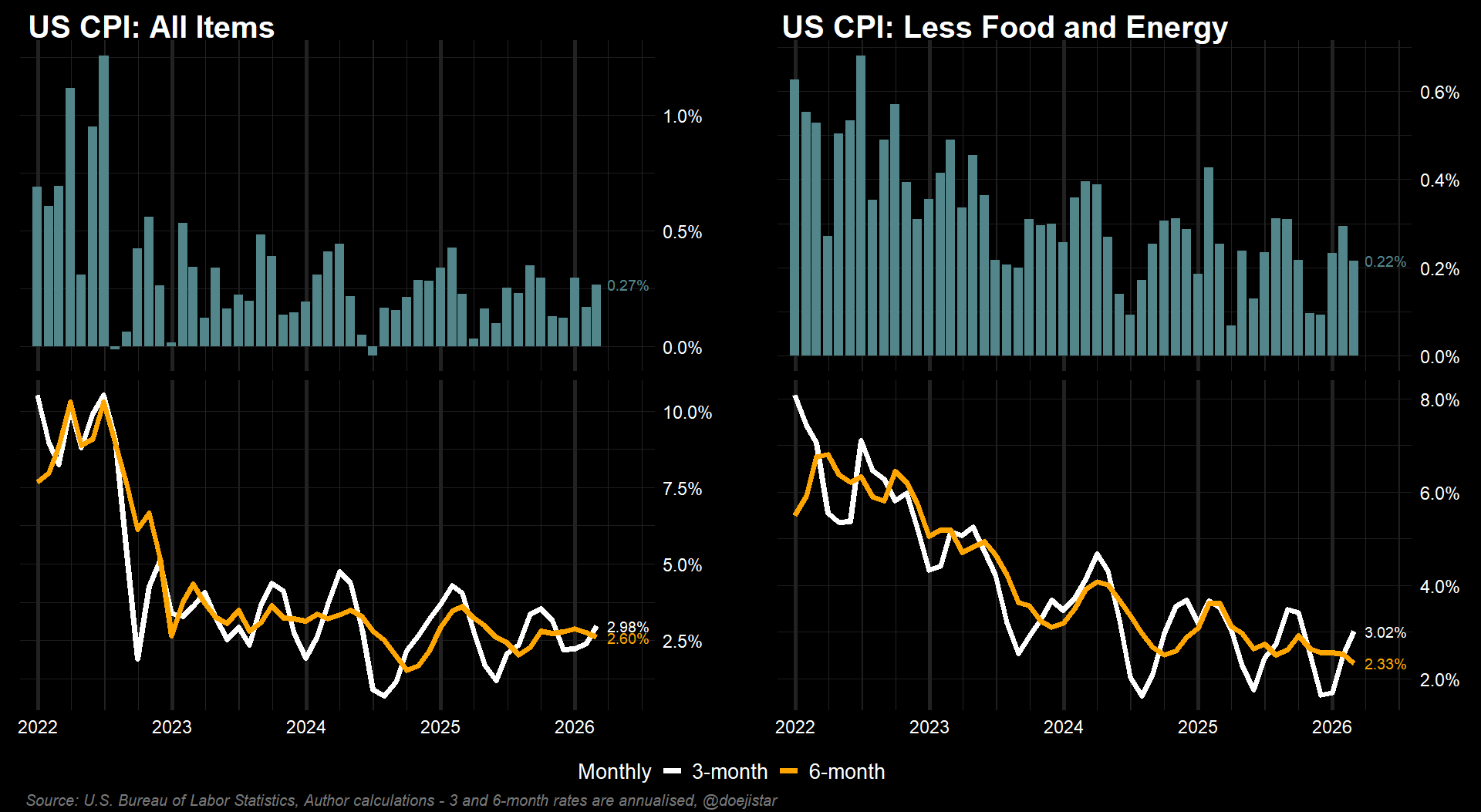

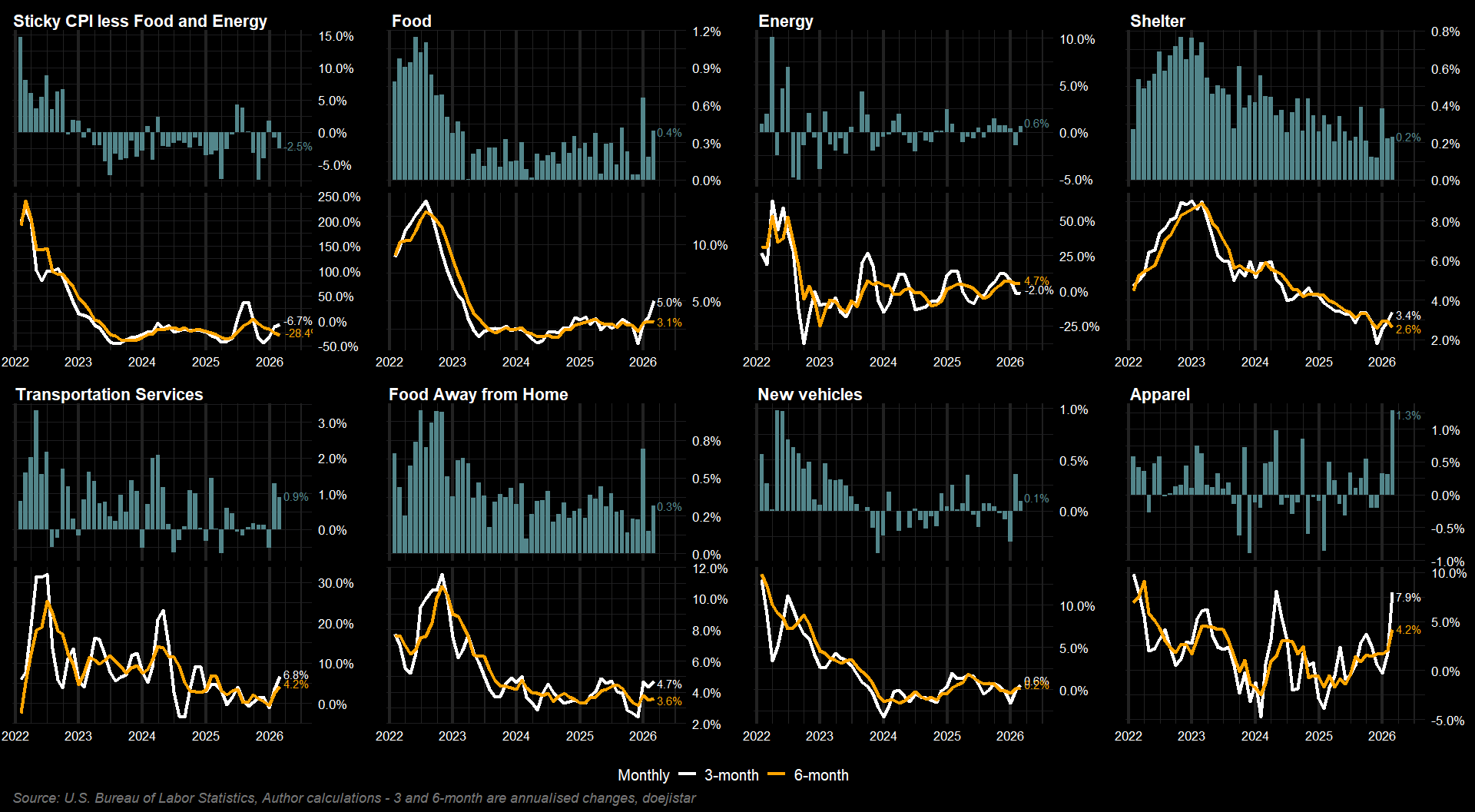

INFLATION

CPI was in-line with MoM expectations of 0.3% headline and 0.2% core with the 3-month trend continuing to pick up.

A pickup across some major components since the end of last year is likely to temper any thoughts by the FOMC to cut any sooner who were, just a few months ago, very welcoming of the disinflationary progress.

We're only up to the January month for PCE, but both 3-month annualised headline and core were in acceleration to roughly 3.5%.

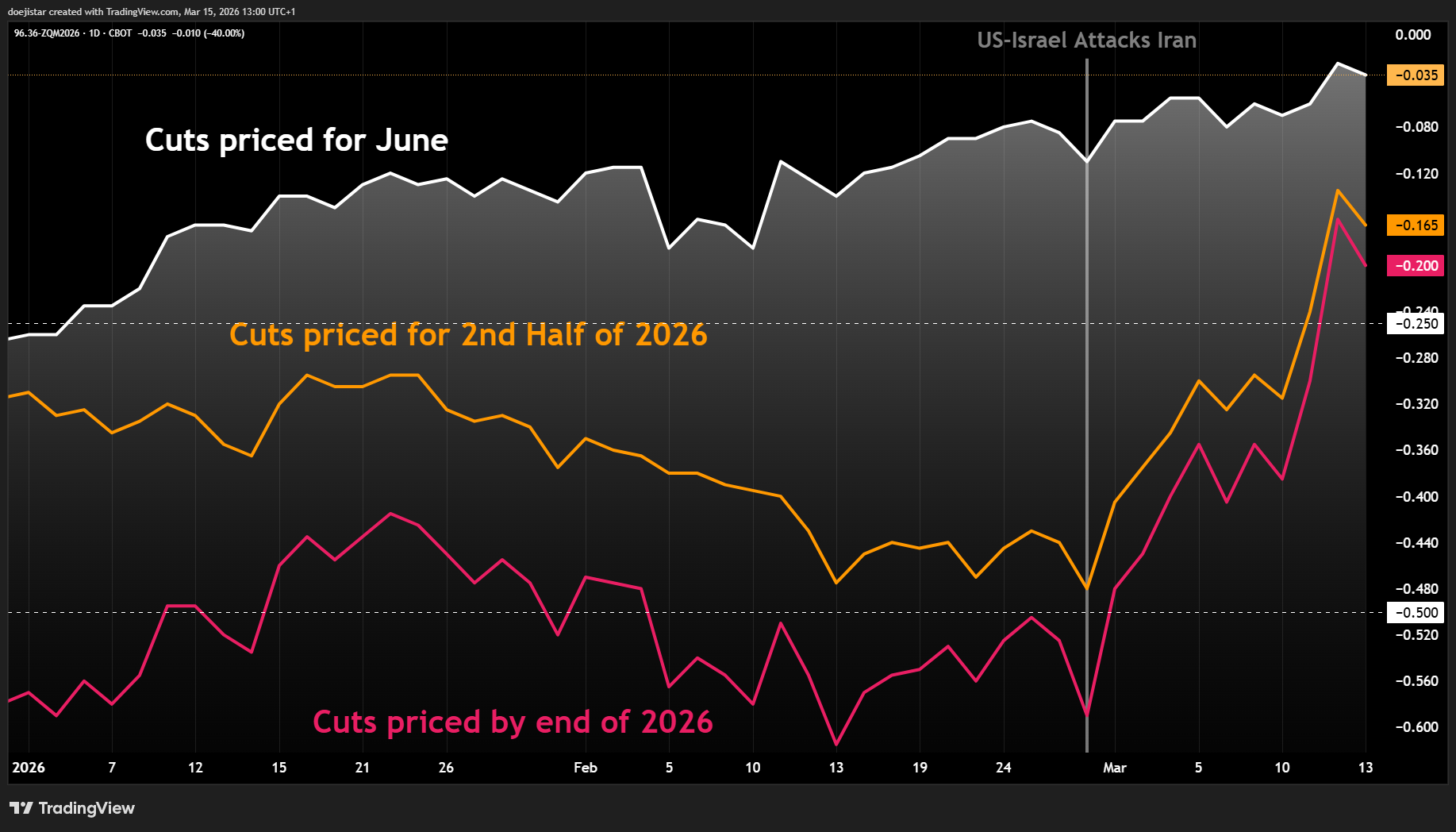

Cutting expectations were pushed back into the latter half of 2026 as inflation began to pick up again, then a cut in 2026 suddenly became a doubt as the Iran-war kicked off with the 2026-end pricing at 20bps.

The surge in Energy prices is already impacting prices at the pump coupled with seasonal demand strengthening through the spring and summer months. The US will be releasing 172 million barrels of oil from its SPR over the next four months in an effort to offset higher price pressures, but there will be some damage done to the inflation picture with significant upside risks to the next March and April CPI reports.

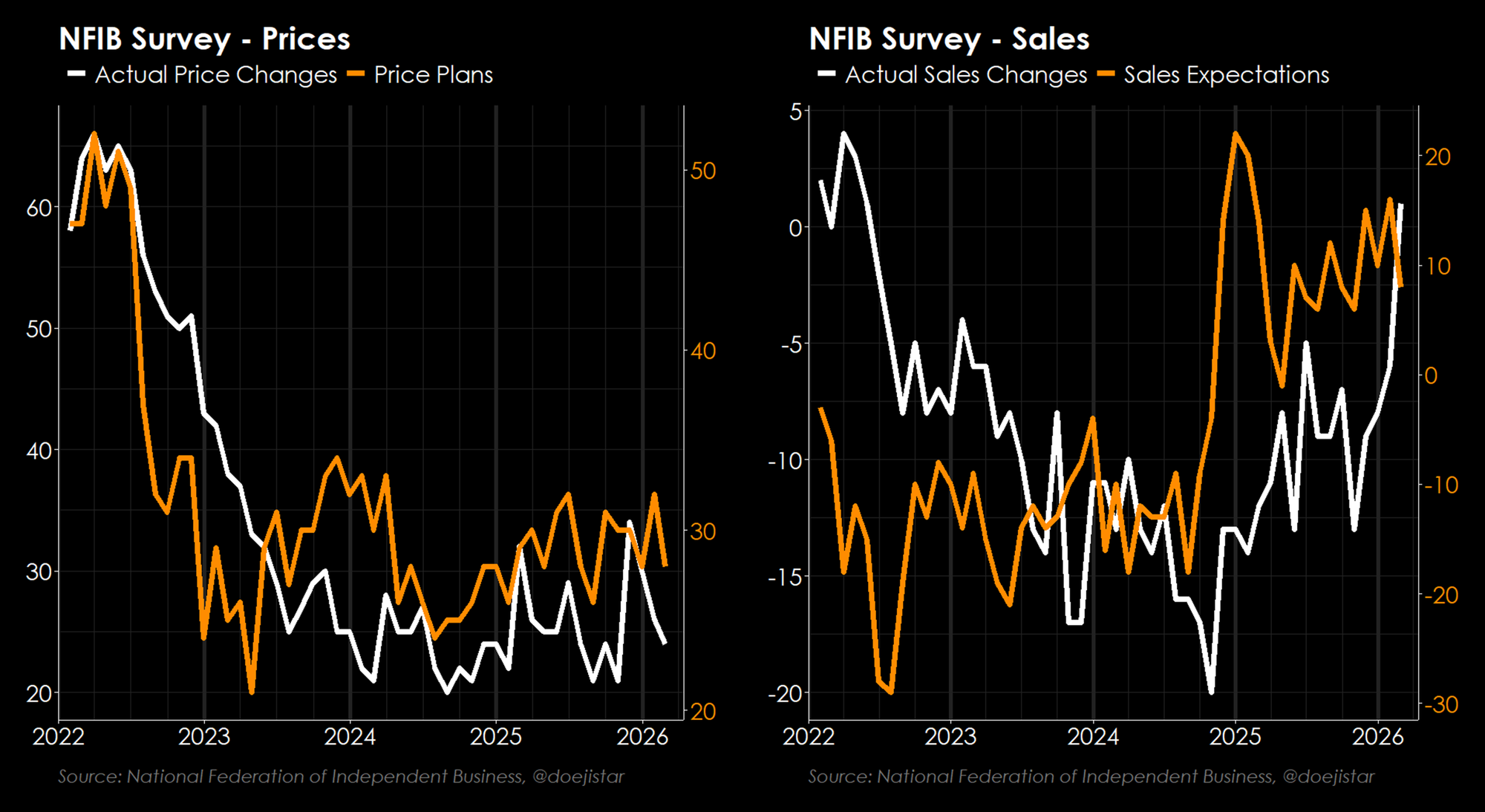

Net percentage of firms reporting higher price changes have eased, but proportion of firms reporting a positive change in sales had turned positive for the first time in almost 4 years!

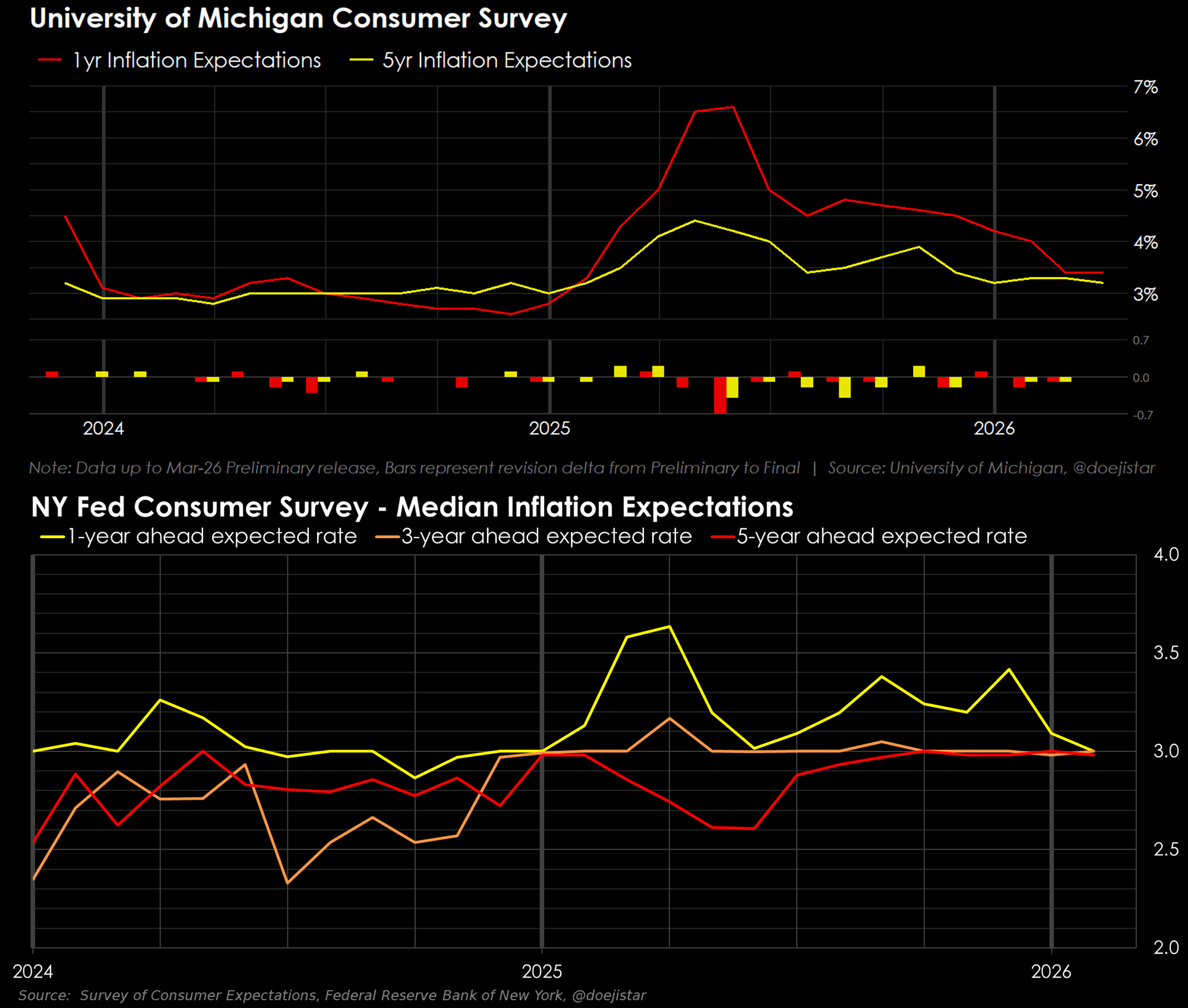

Consumer inflation expectations have also eased, but the risk is to the upside for the Final UoM release and NY Fed survey for March given the 20% surge in average Gas prices so far this month, and almost 30% so far this year.

EMPLOYMENT

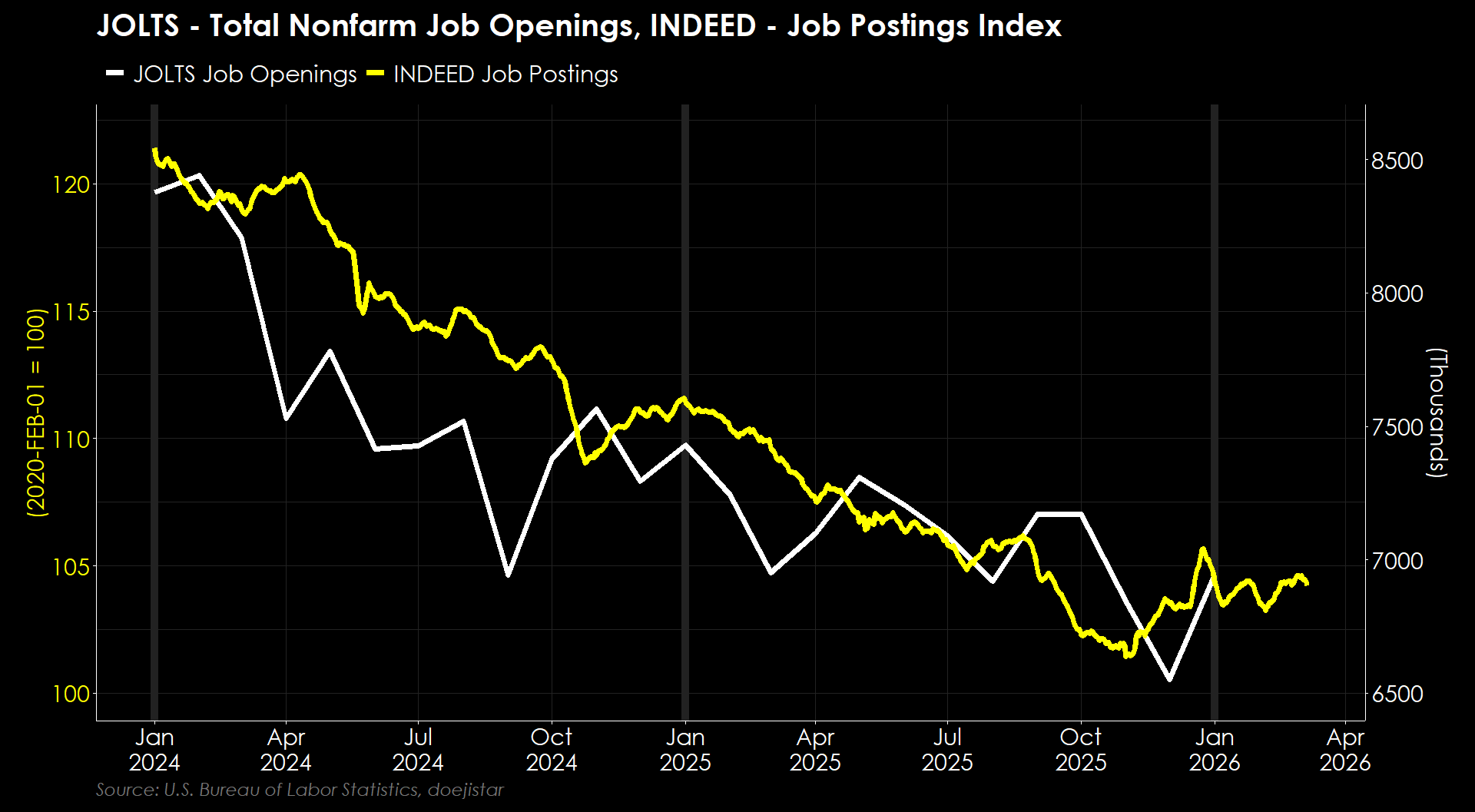

JOLTS openings was 6.9 million, above the prior months 6.6 and above expectations of 6.7. The more up-to-date Indeed data suggests openings have remained stable since the start of the year.

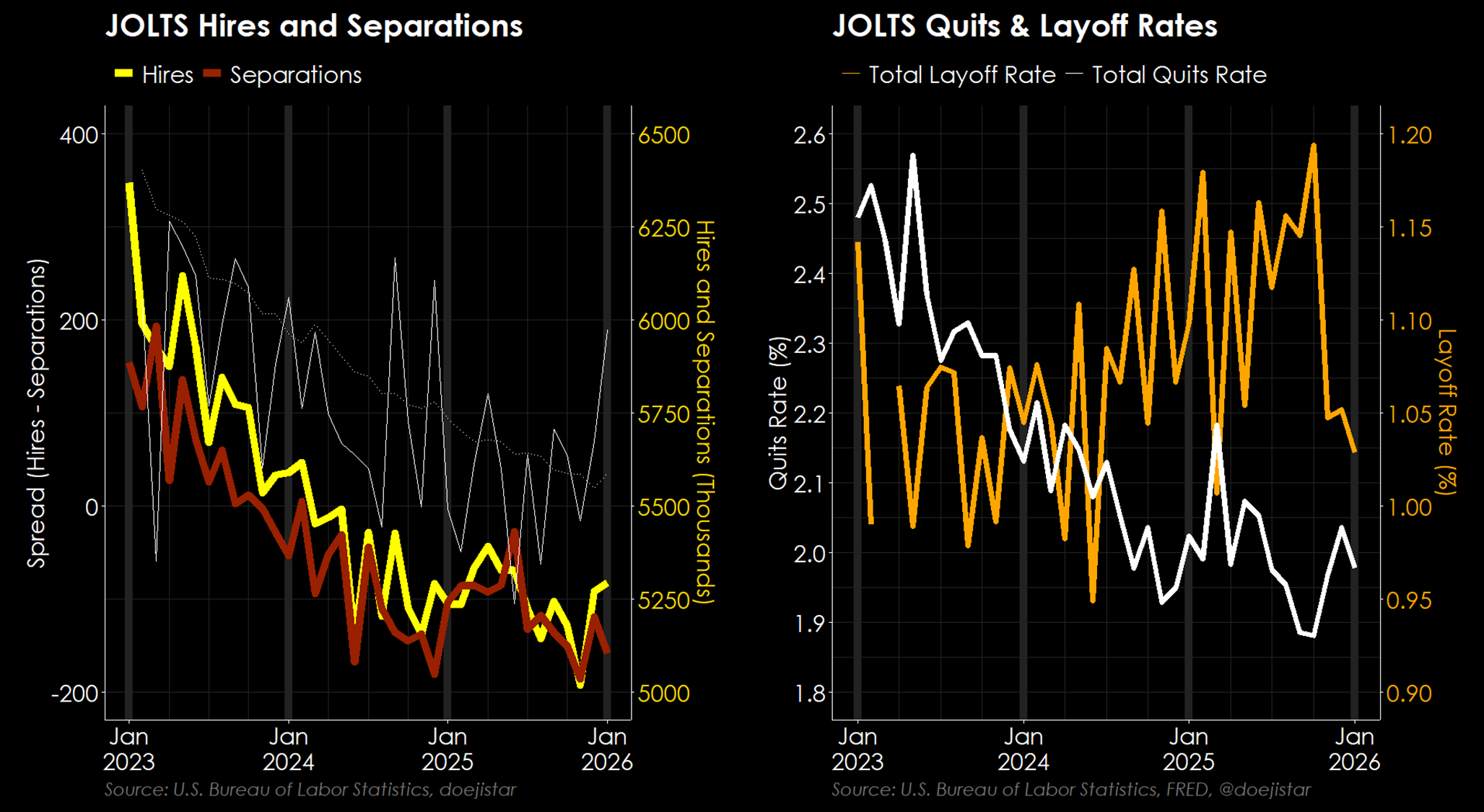

There were only slight changes to hires and separations but had both moved in a positive direction with the spread at the highest in over a year. Quits rate was just below 2% and the layoff rate continued to move sharply lower reinforcing the “low-hire/low-fire” environment.

But employees are less willing to quit their jobs (orange) as if job-switching may be too difficult or too risky given consumers view on finding a replacement job being very low (green).

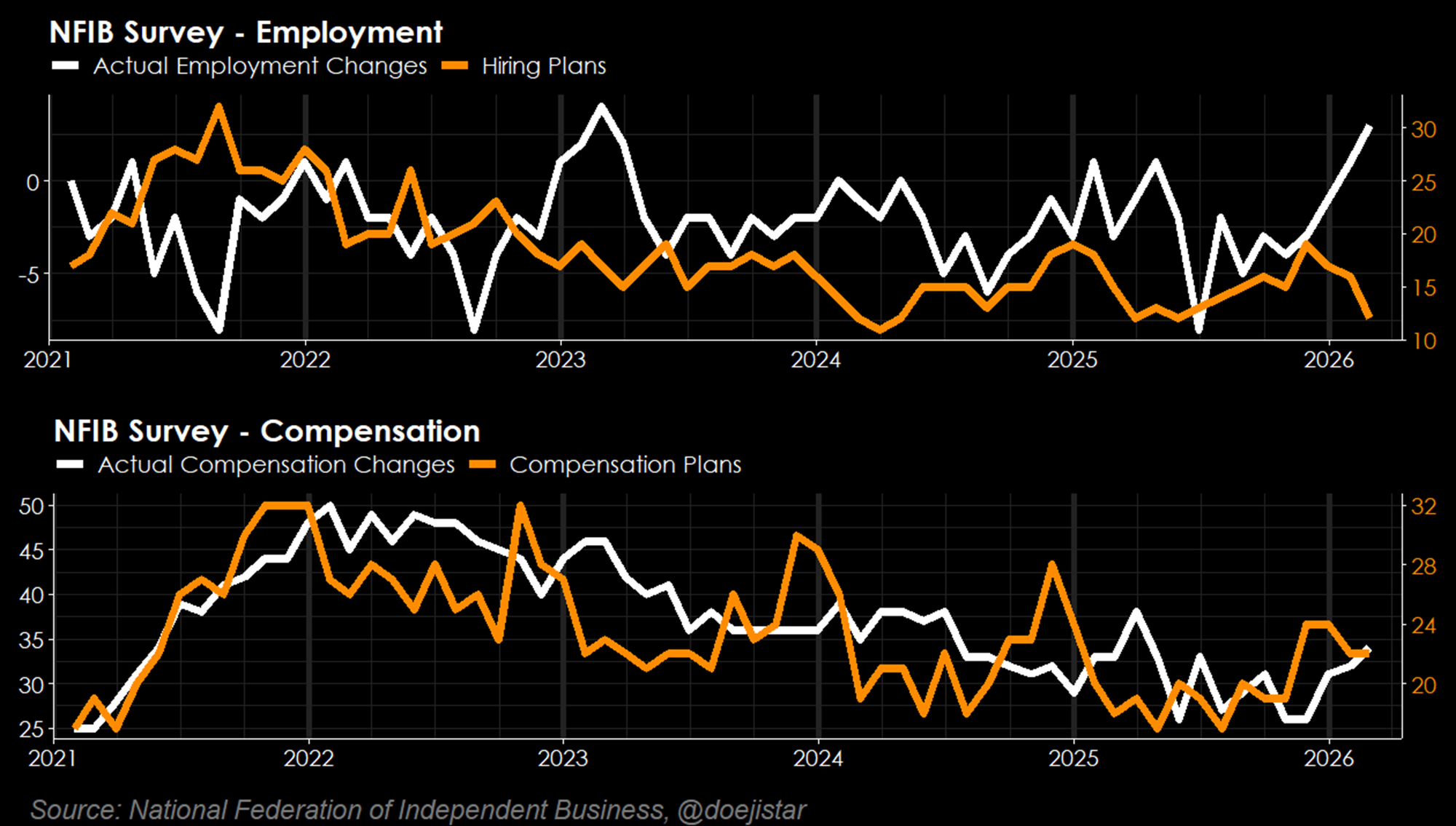

On the plus side, more small businesses have been reporting positive employment changes for a 2nd straight month, paying their employees more, both of which appears to line up with the big rebound in Sales, observed earlier.

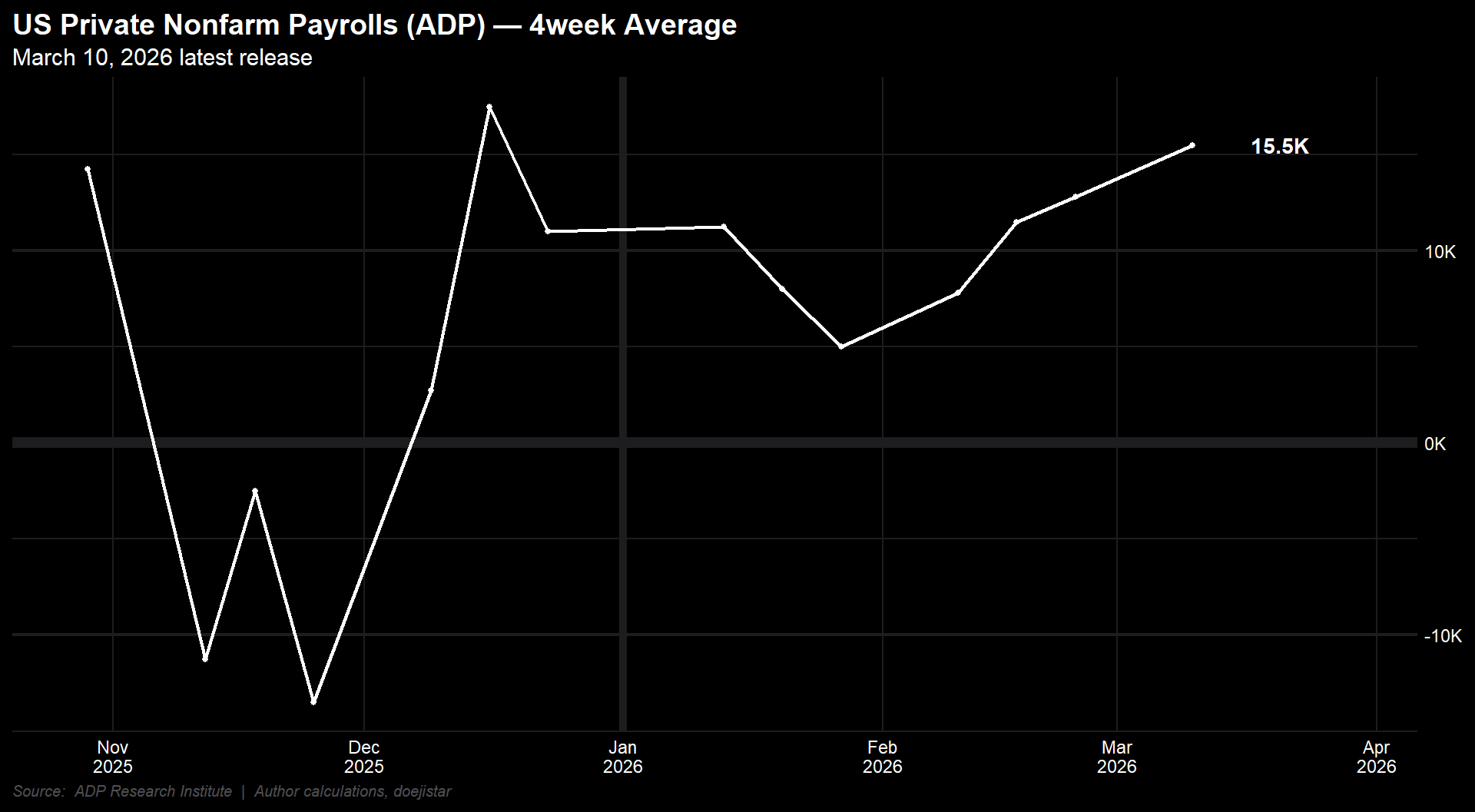

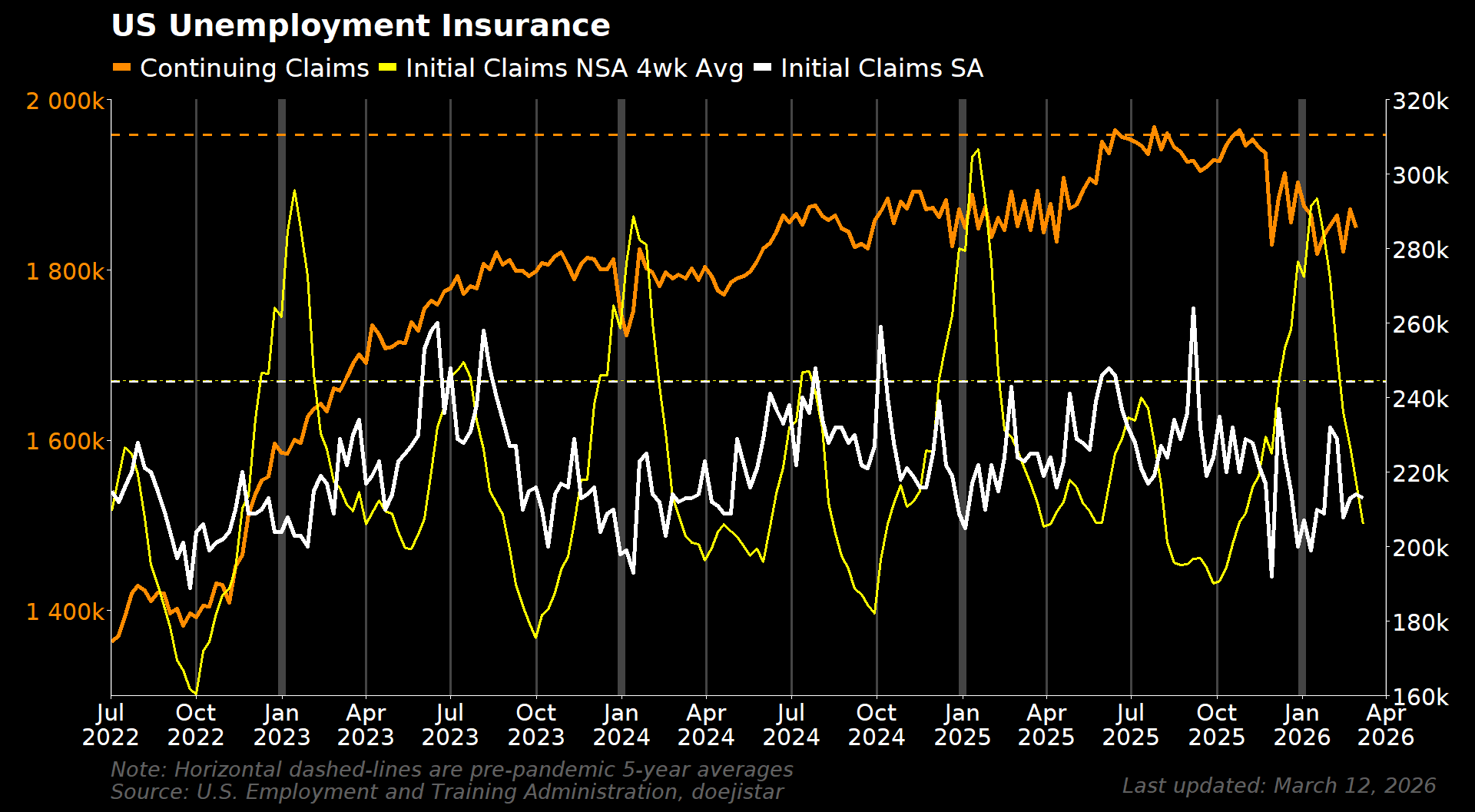

ADP's weekly payrolls data also suggests slightly firmer hiring so far this year, compared to late last year, and Unemployment claims continues to be steady at low levels.

GROWTH

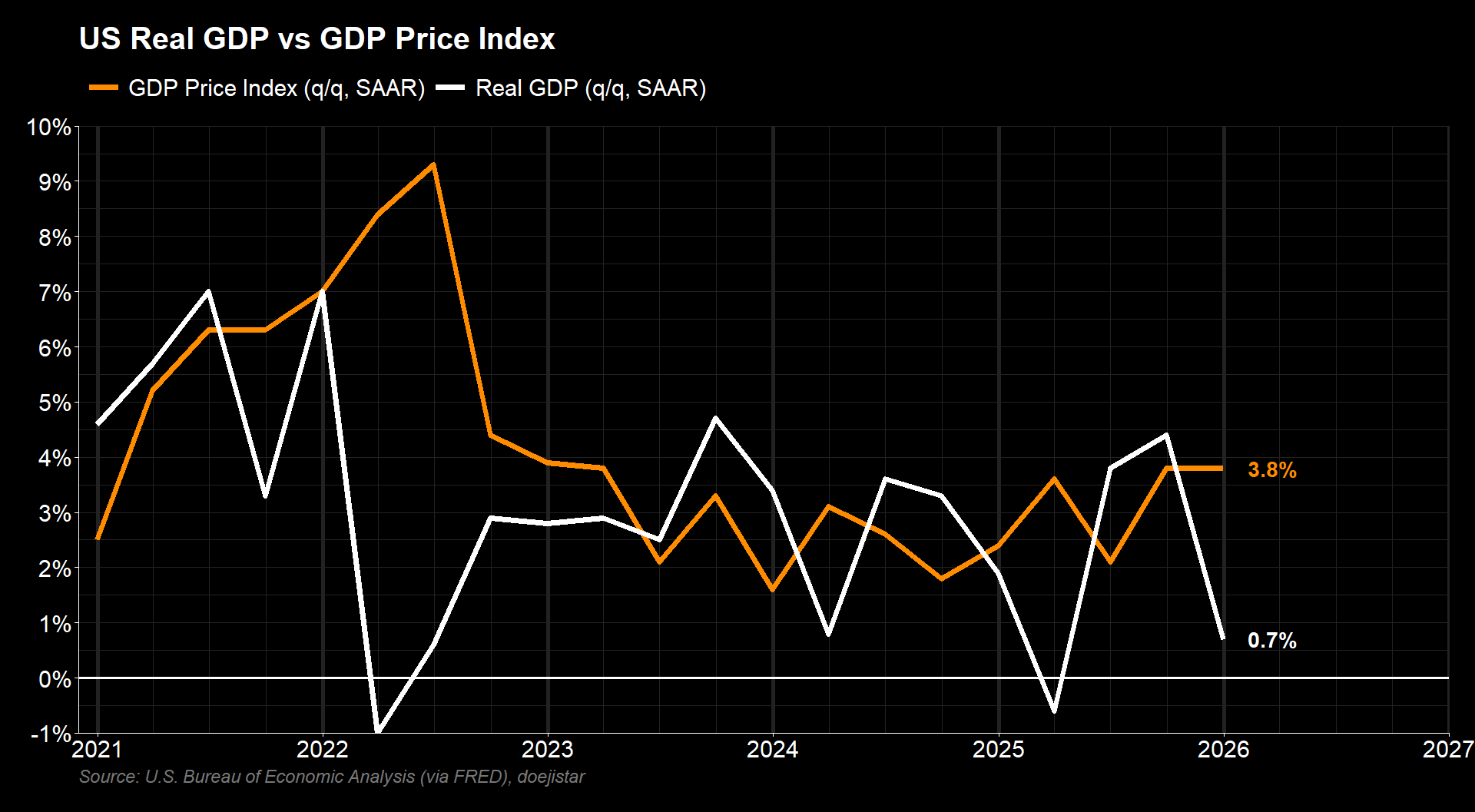

Preliminary (2nd release) Real GDP was 0.7% for the 4th quarter showing growth to have slowed much more than the 1.4% expected. GDP Deflator was also higher 0.2% higher than expected at 3.8% showing stronger than expected inflation.

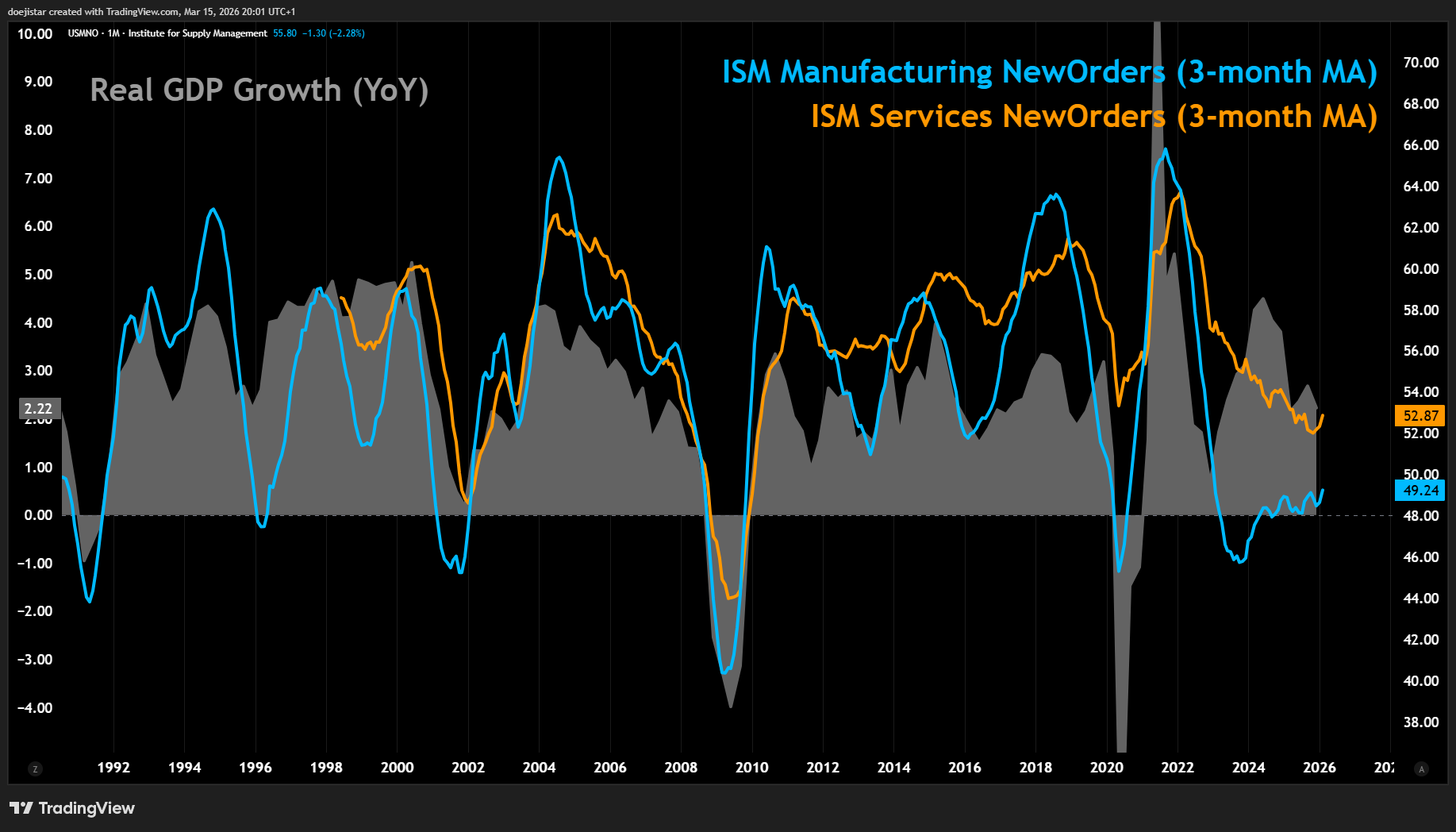

ISM New Orders which tends to lead GDP has been on an upward trend the past 6-months pointing to resilient growth despite the weaker than expected Q4 GDP. While we won't get the next set of ISM PMI reports for another 2-weeks, I suspect the sub-components will be closely watched as well as have a large bearing on RV performances going forward. And while US data still looks very resilient on the whole and assumed to be the most shielded from Strait of Hormuz disruptions, India and Asia are not and likely to see that reflected in the macro data. We look forward to early indications of that as soon as the following week for Europe and India, and the Asian countries on April-1st.

Technicals

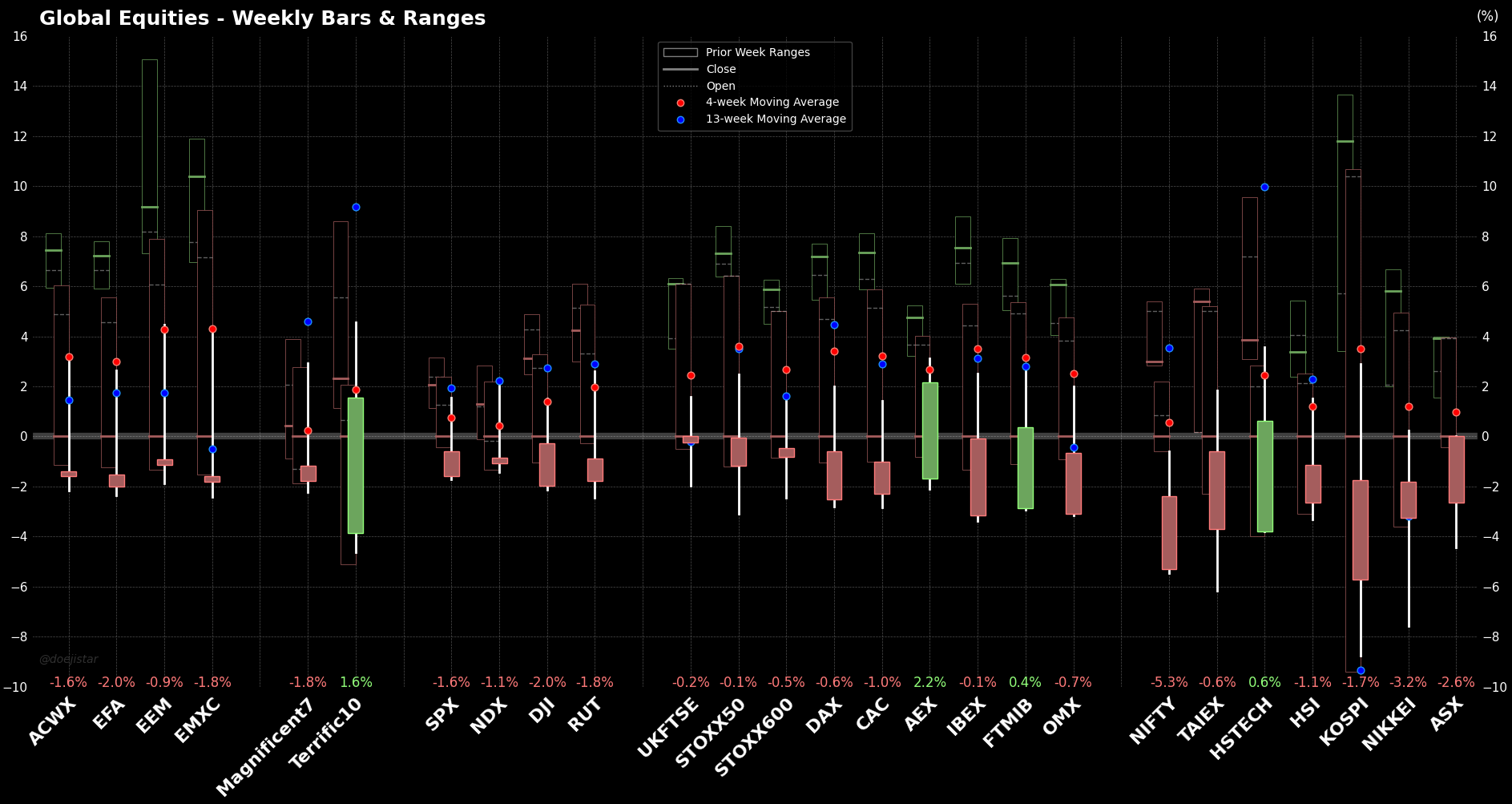

Global equities produced something of a dead-cat bounce on Monday, the bounce of which was faded as the week progressed. Clearly not a sign of buying pressure.

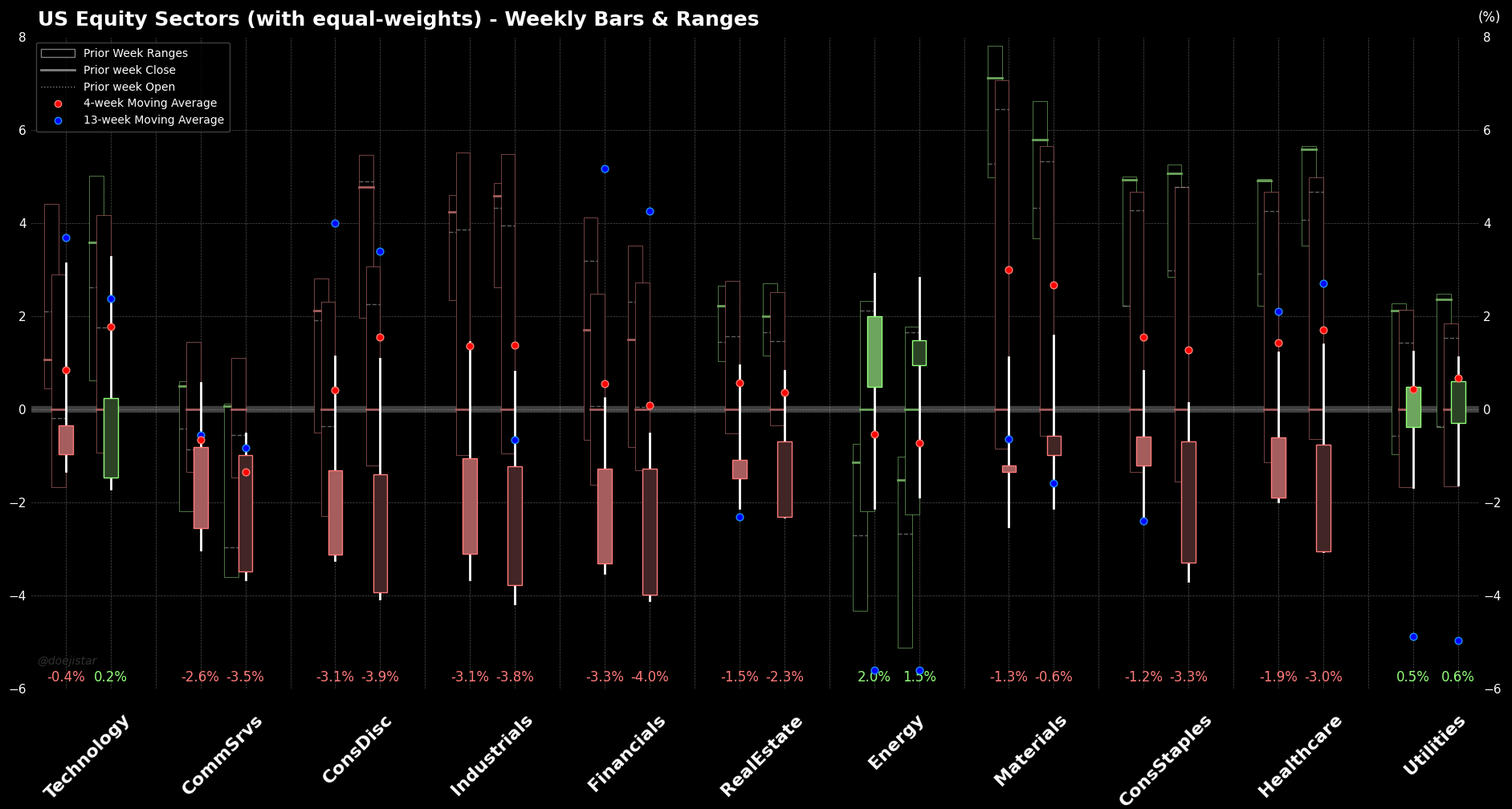

Energy was the standout performer, followed by Utilities. Equal-weighted Technology finished marginally up, but there is clearly a bearish performance profile with the weekly closes pretty much at the lows.

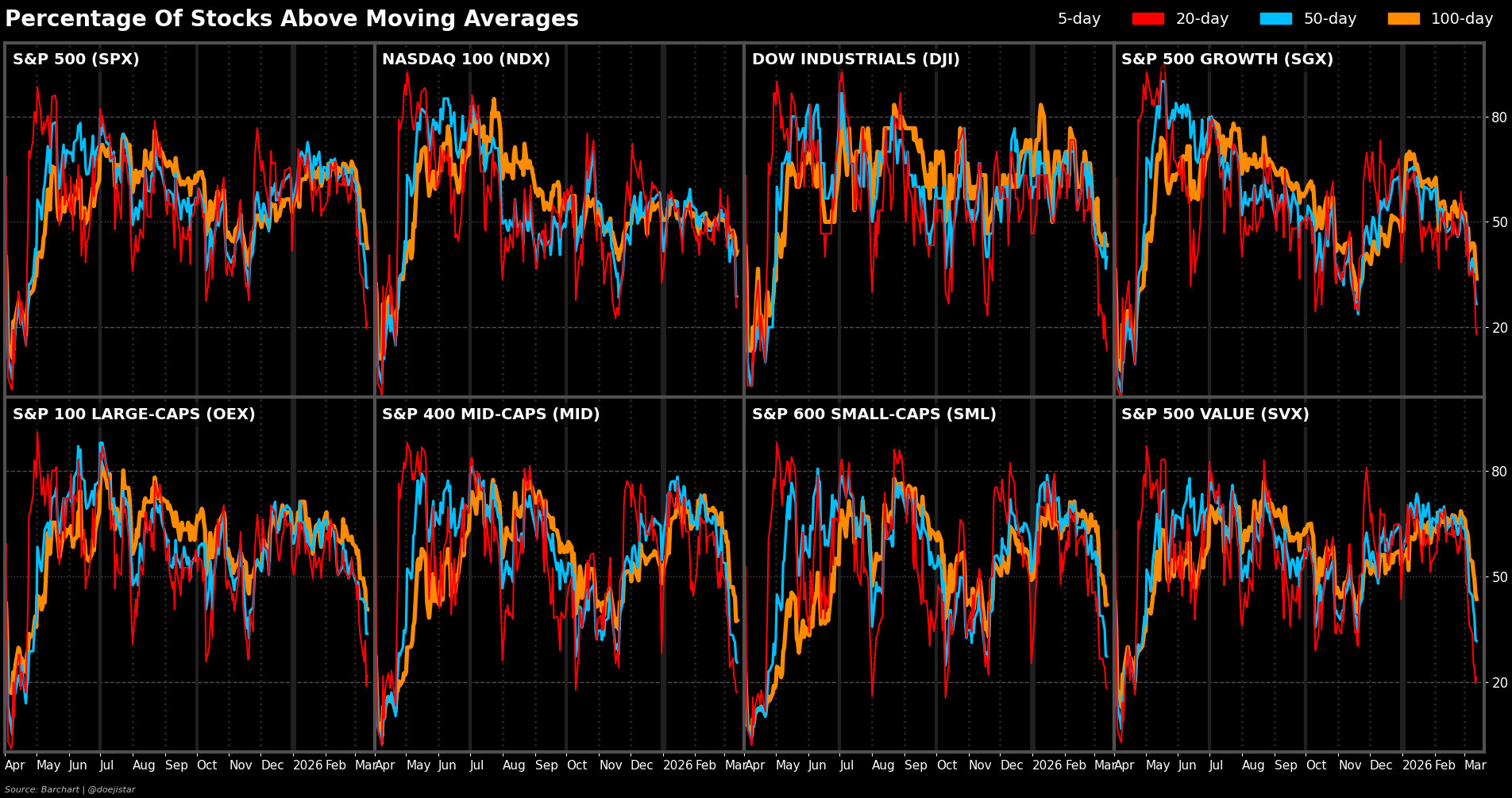

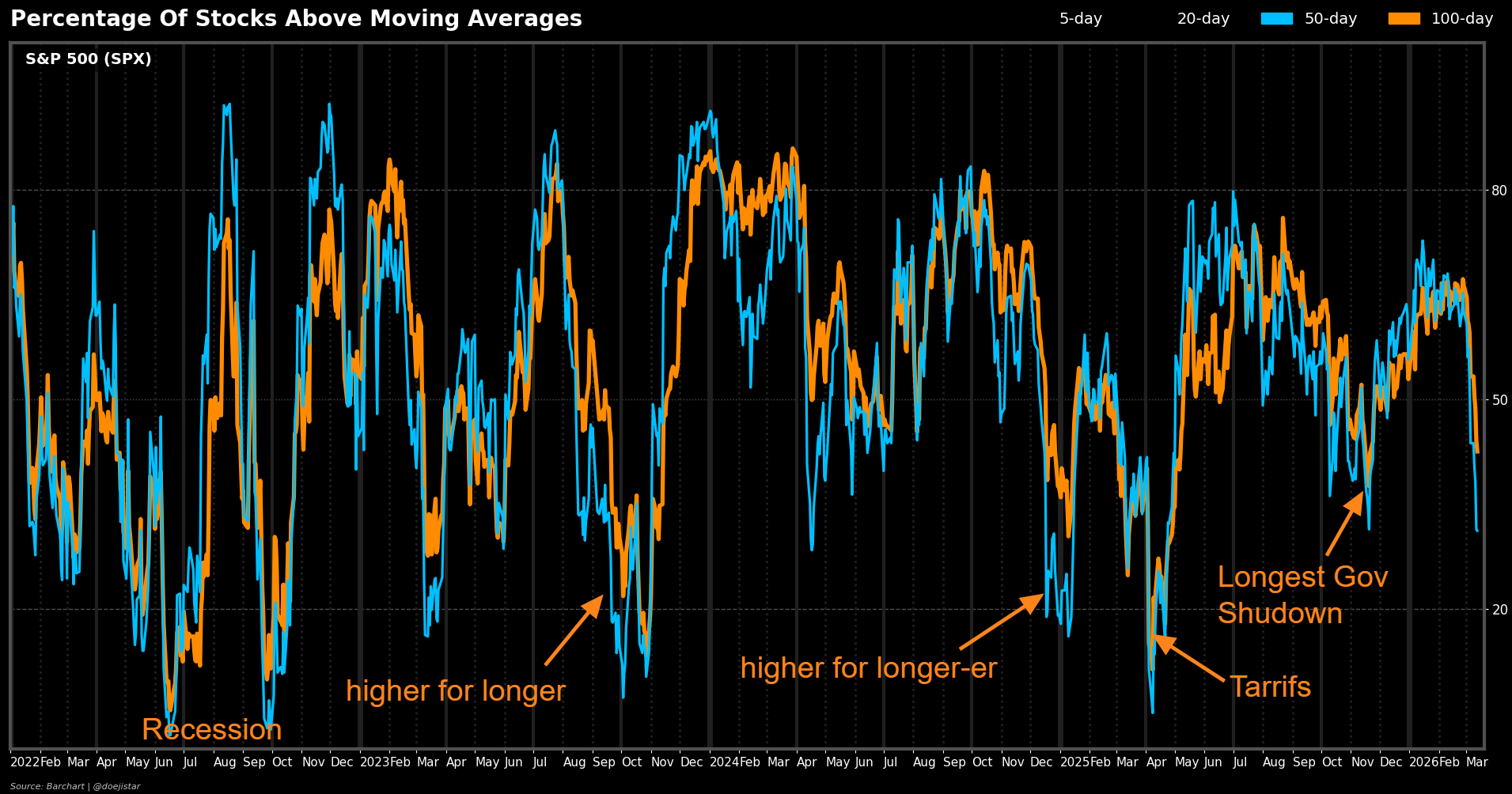

Equities are starting to look oversold looking at the percentage of stocks below the 20dma, but I want to focus on the 100dma series while there are some big macro narratives driving the market in a way that it could be differentiated from shorter term narratives. Taking the most recent example to benchmark from to start with, last November we were dealing with the longest Government shut in history, coupled with concerns about a cracking labour market and a US growth slowdown which amounted to the latest sell-America wave.

Today, the US economy faces +20% mtd and 30% ytd gas at the pump prices which are likely to have impact on macroeconomic indicators and fed policy. We've seen how the market has shifted from expecting almost 3 cuts before the Iran-war to now 1 cut being a doubt by the end of 2026. That complete change in policy expectations within the space of 2-weeks is so significant that it one should probably take their time to bet against, should they wish to do so, or have a view that it will pare back. Secondly, there is reason to believe that the growth risks that we face currently are far greater than those that existed around the government shutdown because the risks are created by higher Energy prices as a dampener on growth - i.e. stagflation. Those were the conditions that led to a mild recession and equities bear market in 2022. That said, I currently don't see stagflationary risks being as great as they were in 2022, but that is the regime we are venturing into now, and historically, these risks tend not to dissipate as quickly as they have arisen.

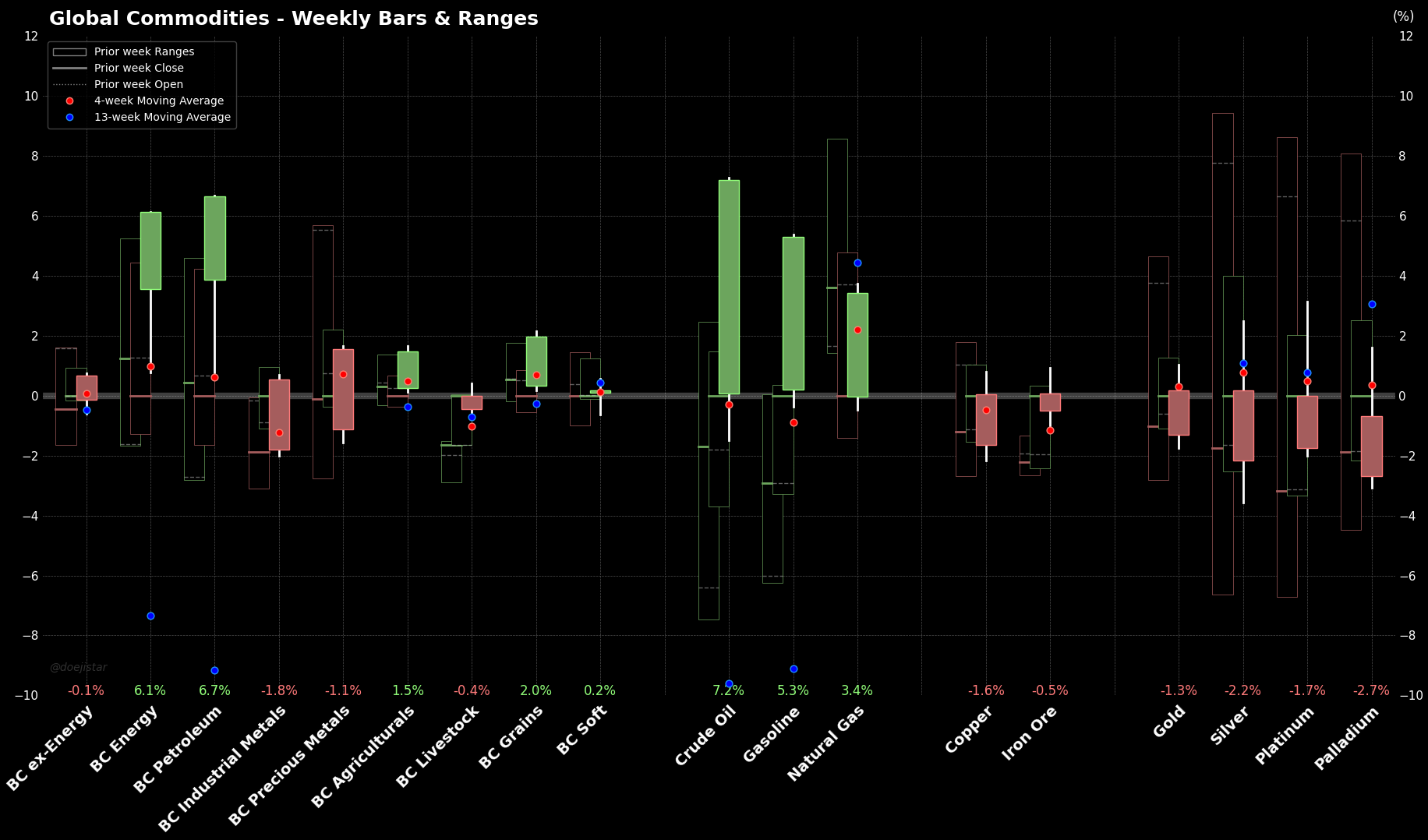

In Commodities, Crude is a clear winner while metals have been the worst performers. I've no idea how far higher Energy prices can go, or how low Metal prices can go, but I have yet to see concrete reasons why these trends should reverse based on my earlier analysis using basic game-theory to illustrate that a prolonged conflict is more likely than not.

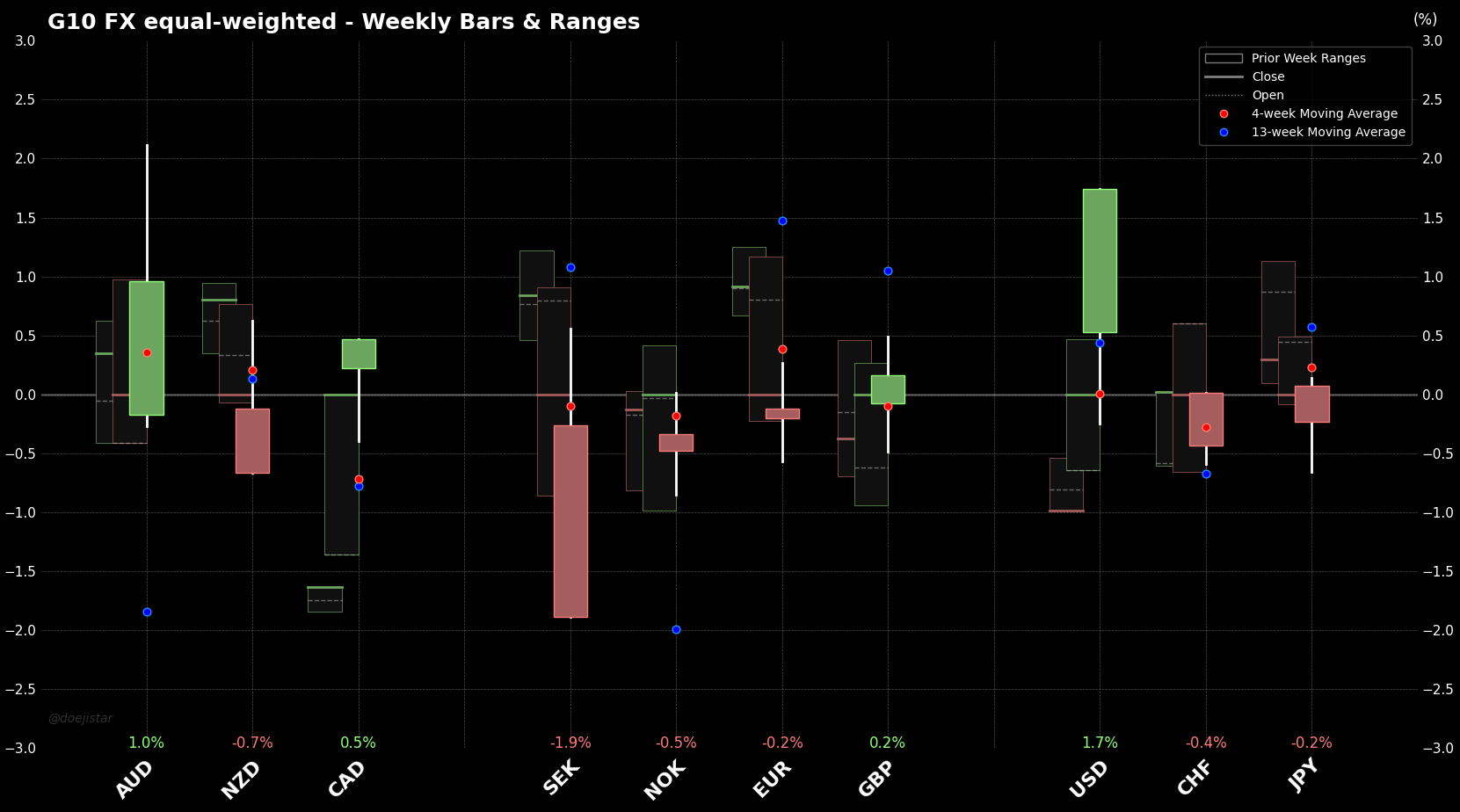

That gamed-out scenario points to the persistence of high Energy prices and Dollar to win out as a geopolitical safe-haven as well as on US exceptionalism due to growth differentials turning in favour of the US due to a more shielded impact compared to other major economies and currencies.