Week5 MacroTechnicals - Stretched...

Shutdown risk is back in focus as markets look stretcheddd as it it's just looking for a reason to snap back and to get a short-term reset in some monster rallies.

Market doesn't appear to be pricing in much downside risks with lots going on and many markets looking stretched and some potential tail risks in crowded systematic and retail positioning as well as the highly leverage basis trade that could cause spikes in rates volatility.

The first thing I see scrolling through twitter this morning is everyone talking about a potential government shutdown as if it was big and somewhat unexpected news. The MTT group will know quite well that this is something I've been discussing for quite some time and have said to expect a lot more of, given that we've seen last-minute stop-gap bills and filibuster votes being a regular occurrence every 3-months or so, if not leading to a temporary government shutdown on 2 occasions during Trump's first term.

If shutdown risk isn't part of your ongoing scenario analysis of any sort, it really ought to be. Though it can create some tricky headline-driven trading conditions, some market volatility is something we traders (should) all relish.

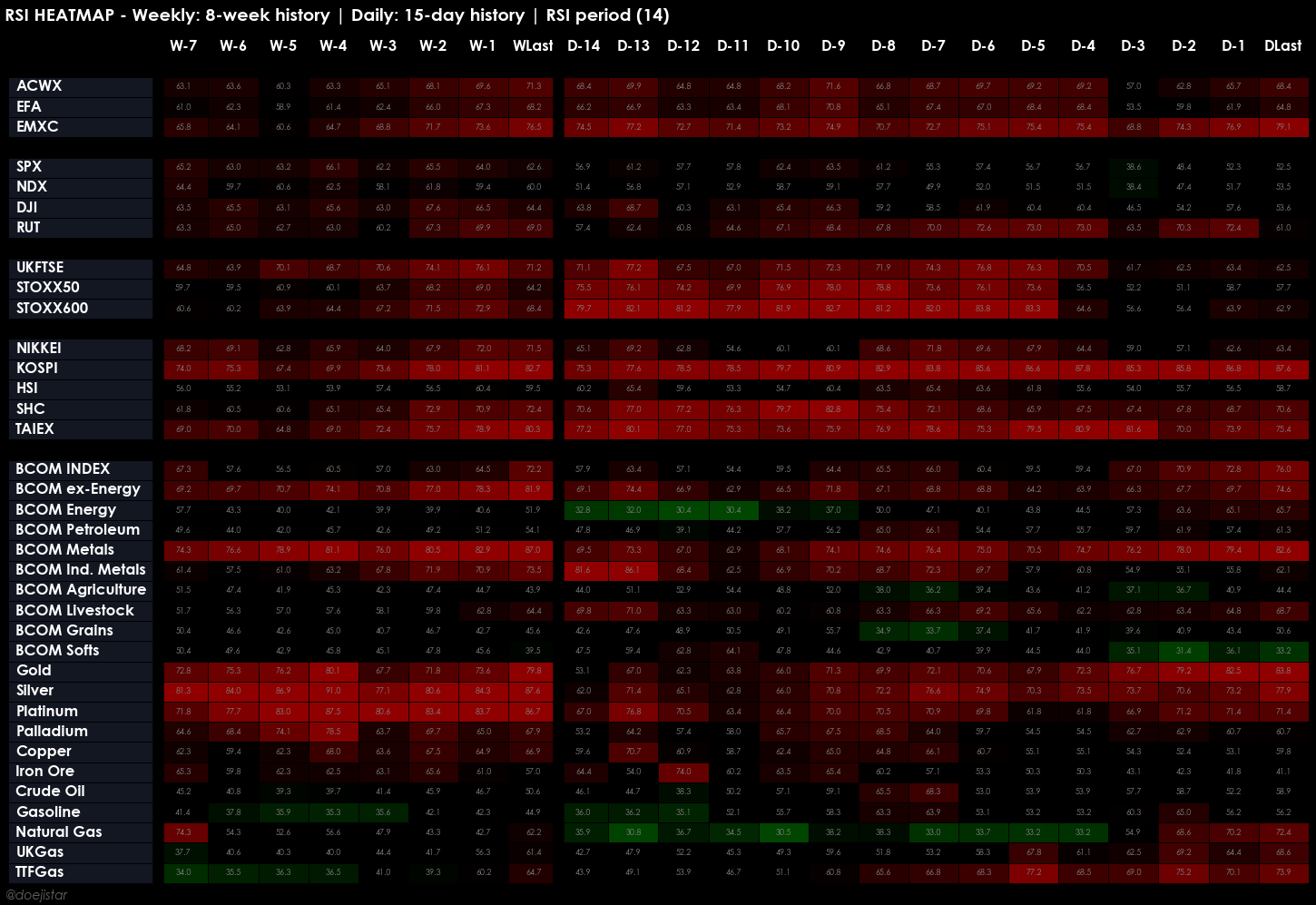

That ties in nicely with the point I wanted to highlight for this week which is that the broader market is looking very vulnerable to a pullback. I've put together a table showing Weekly and Daily RSI's covering some major equity indices and commodities to illustrate.

Some notable mentions goes to major equity indices ACWX (All-Countries-World ex-US), EFA (Developed markets), and EMXC (Emerging ex-China) with Weekly and Daily RSIs near or above the 70 threshold. Asian equities have been on a tear and are well into the extremes - KOSPI in particular whose RSIs are at 82.7 and 87.6 as of last Friday's close, as well as TAIEX (80.3 and 75.4) and the Shanghai Composite (72.4 and 70.6).

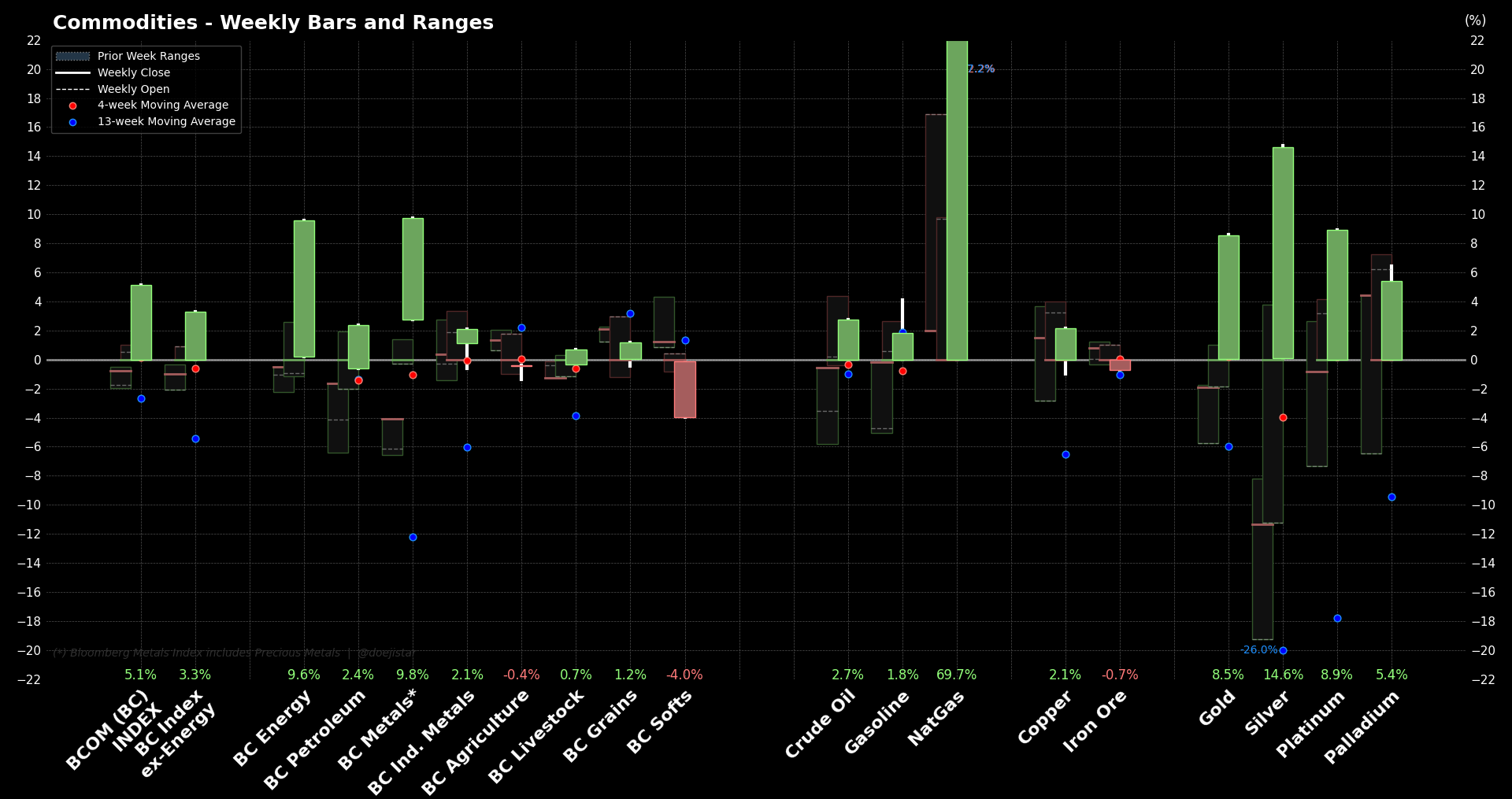

Commodities are also ripping led by metals, as I'm sure we're all aware. The Bloomberg Metals Index (which includes Precious metals) has RSI readings of Weekly 87.0 and Daily 82.6. Nat Gas should also get a mention with its massive 70% rally which was the Daily RSI go from 33.2 at the start of the week to end at 72.4.

This is by no means a call to fade all the extremes, but it certainly is worth taking note given that there have been geopolitical risks in the background to which the market has largely ignored, as well as the positioning risks we've flagged in prior weeks.

Speaking of positioning, the good ol' basis trade is being talked about and reportedly back to near-record levels. This is a popular arbitrage among hedge funds which requires high leverage to make meaningful profit on the spread, so when there is a deleveraging event, the cascading unwinds and spike in rates-vol can be brutal to the extent that it has a systemic-impact on financial markets, and leaving no prisoners in such an episode... even Gold.

Some assets have had one heck of a run, and as foolish as it might seem to contemplate fading them, it won't take much to see some rallies collapse as fast as they have gone up, if not faster. The risk/reward is clearly there, but a decent success rate most likely isn't; I do feel however that a shrewd trader can manage that lowly success rate with some decent trade management skills. Granted this won't be for everyone - a series of losses and trail-outs after going in profit can be frustrating enough to go on 'tilt', but the idea is that 1 of every several attempts will at least pay off to some degree to make up for some losses and efforts. Again, not for everyone.

Also, whilst I'm on the subject of trade management around a certain idea, another method as an alternative to using options that I employ from time to time is to allocate 'x' percentage of capital into a separate account for the sole purpose of trading a particular idea, and an account with the highest leverage accessible. Not that you plan to go all guns blazing immediately, but so that it's there should it come in handy such as adding aggressively to a profitable position.

Macro

WEF TAKEAWAYS

Starting with some key takeaways from a rather eventful WEF...

Ice-land?

Trump's agenda dominated the forum after stating that he would get Greenland "the easy way or the hard way". Tensions were high in the lead-up to the forum after a series of escalations that began with 8 EU nations 'symbolically' deploying military to the island signalling their opposition. Trump responded with 25% tariffs on those nations forcing the EU to consider massive retaliatory tariffs.

Trump in his keynote speech maintained his intention for the complete ownership of Greenland (which he repeatedly referred to as "Iceland" to momentarily confuse markets) but did, however, rule out military force opting instead for economic leverage. A high-stakes meeting with NATO Secretary General Rutte followed leading to Trump announcing a "framework of a future deal" and a pause to the imposed tariffs. The framework focuses on expanding US military access and mineral exploration rights under a 1951 defense treaty, but most notably - excluded any discussion for a transfer of sovereignty.

Latest headlines suggest the EU are expected to ratify the trade deal with the US with a preliminary vote this week, but in terms of a potential Greenland deal, some uncertainty remains with only a framework to a possible deal being agreed to by Trump and the NATO general, while Denmark and other EU members have not expressed any agreement nor willingness to agree.

Climate what?

Geopolitical fragmentation became the key-focus replacing what had been the top topic of discussion over many annually held forums - climate-change, pivoting away from traditional ESG and towards "energy realism" favouring nuclear and grid-reliability amid a power-hungry AI revolution.

No Room for Dessert...

During the BlackRock dinner. US Commerce Secretary Howard Lutnick took the mic to berate European political and economic model, which sparked off a heckling match with a fired-up Al Gore. The real mic-drop however, came from ECB President Christine Lagarde, who reportedly vanished mid-speech. Either way, the vibes were so cooked that the event was called off before dessert! A perfect, bitter metaphor for the current state of US-EU relations.

GROWTH & INFLATION

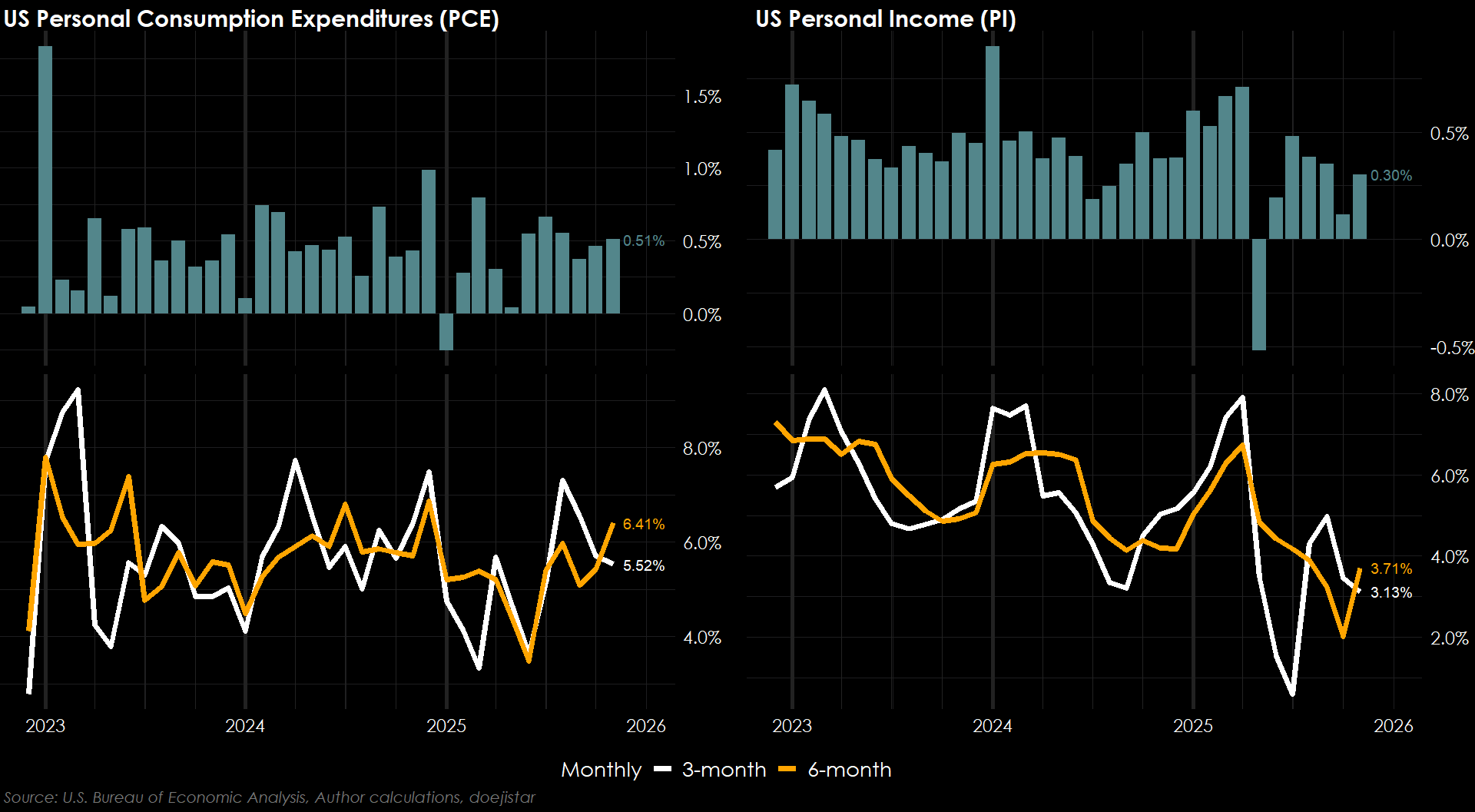

Q3 GDP growth continued to revise higher with the Final print settling at 4.4% - strong! and expected to be even stronger for Q4 at 5.4% according to the latest Atlanta Fed's GDPnow estimate.

Consumer spending via headline PCE continues to prove robust running at an annualised pace well above 5%. Incomes are easing; however, the savings rate also dipping to the lowest since October of 2022 suggests consumers are becoming increasingly stretched, but still far from something to be overly concerned about.

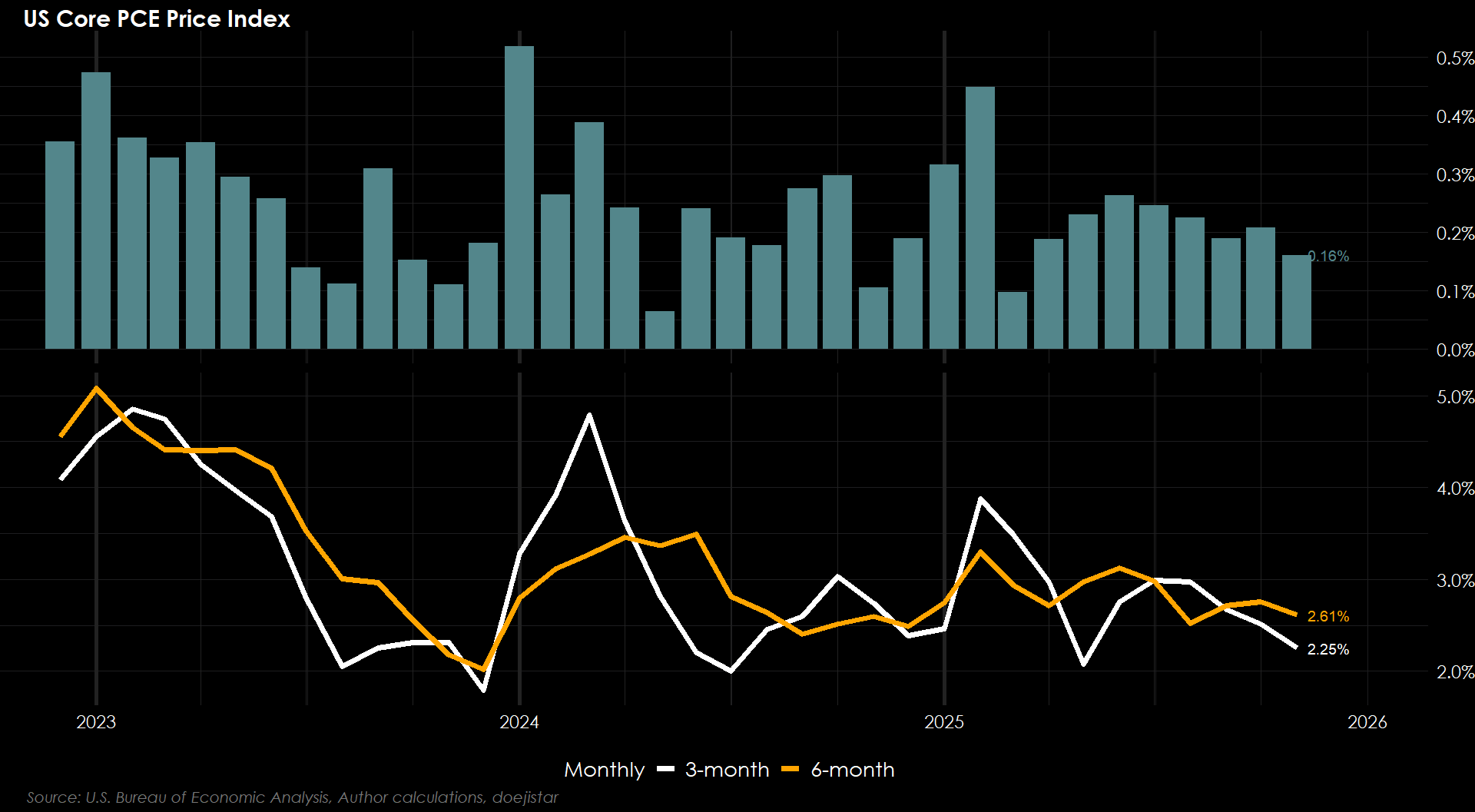

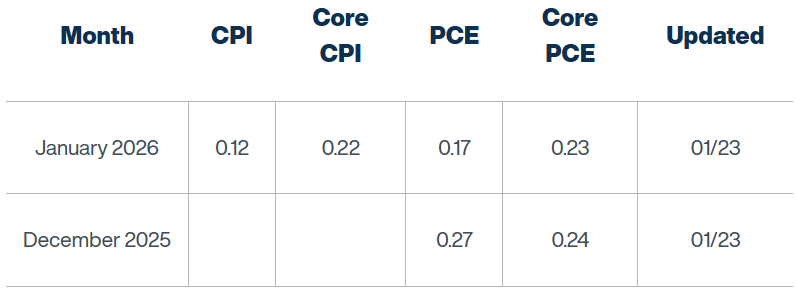

Core-PCE printed 0.2%, rounded up from 0.16% and reinforcing the trend of cooling inflation. It is expected to tick up however from 0.16% to 0.24% in December, then 0.23% in January, according to the Cleveland Fed nowcast.

While these inflation reports reinforce the narrative of further rate cuts, it needs to be balanced against the evidence of inflation stickiness, GDP growth well over 4%, and wage growth at roughly 4%*. The case for further cuts is difficult to argue for with a 3.72% effective fed funds rate for the time being.

* The Atlanta Fed Wage Tracker has wage growth dipping to 3.7% but the last jobs report for the same period shows wage growth running firm on a 3-month annualised basis at 4.1%.

LABOUR MARKET

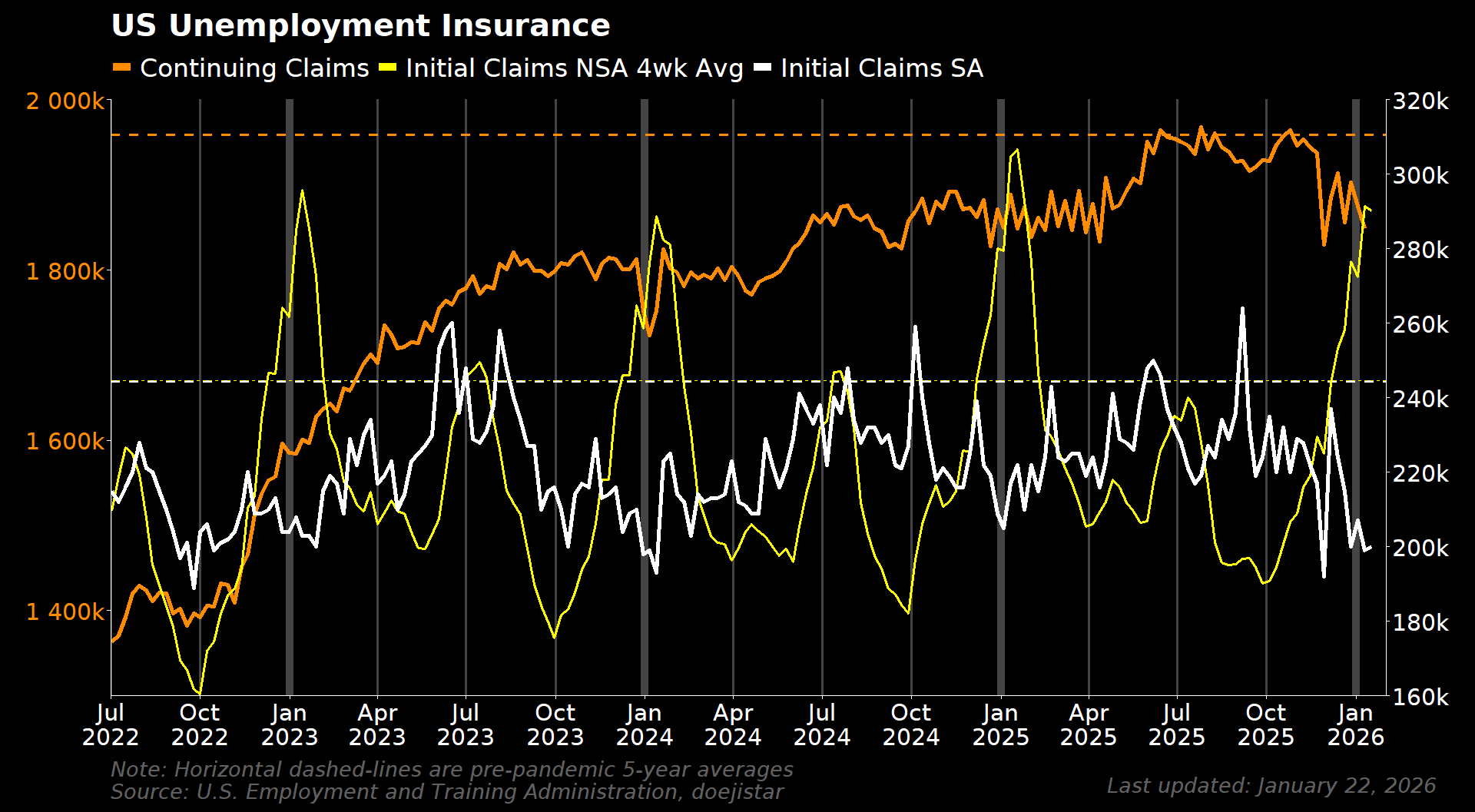

Latest claims data were encouraging overall. Initial claims was 9k below expectations while Continuing claims points to further stabilisation at 1,849k down from a downwardly revised 1,875k.

CONSUMER SENTIMENT

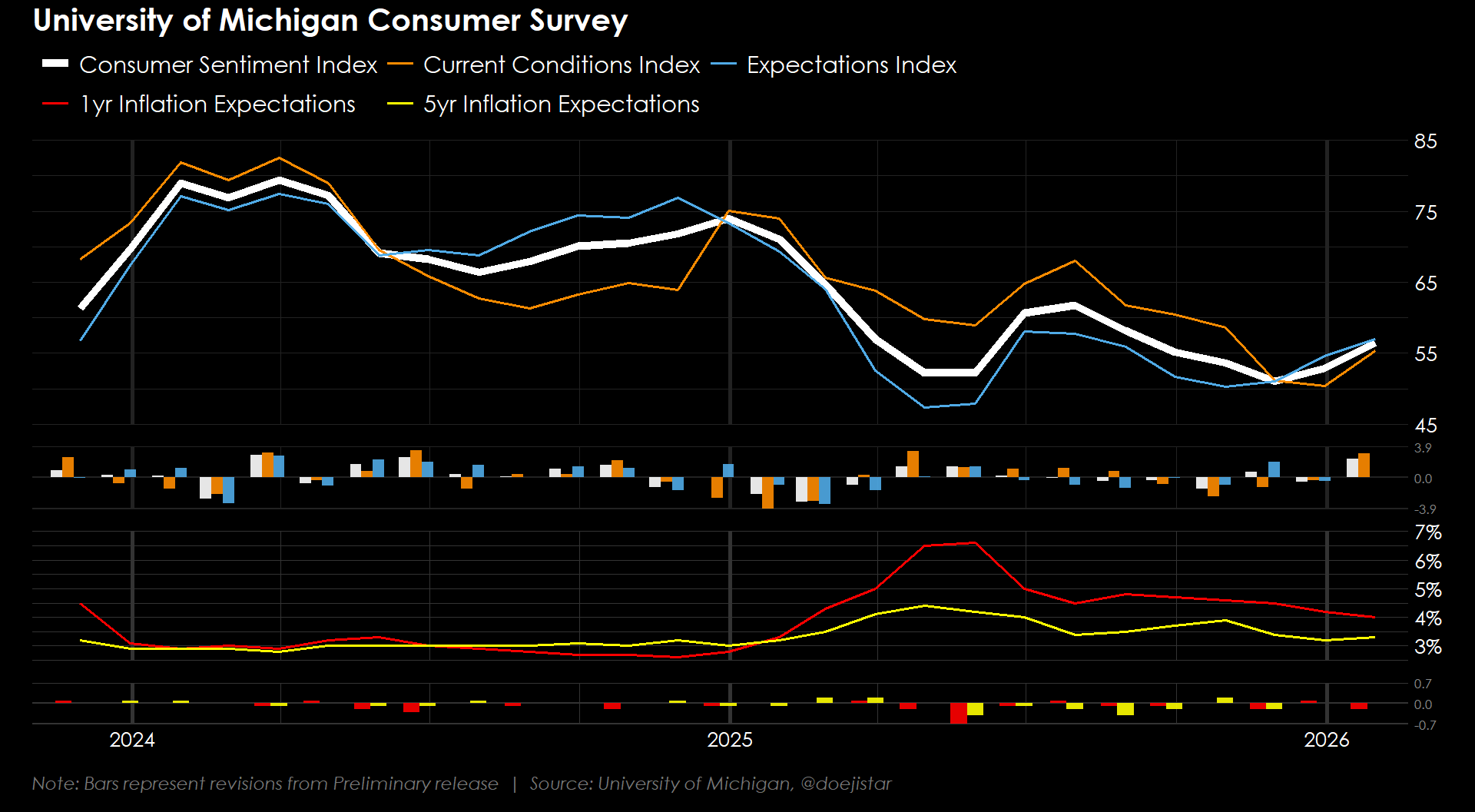

U0M survey points to recovering consumer sentiment with the final release showing a strong upward revision in the Current Conditions Index, and the 1yr Inflation Expectations getting revised down a touch. Though recent consumer surveys have been a touch softer, the rebound in consumer confidence has been quite evident with the UoM survey further reinforcing that trend.

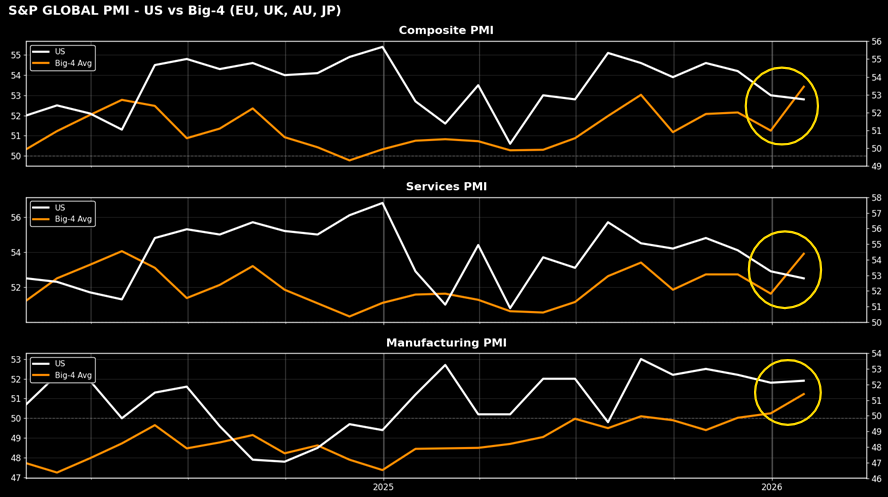

FLASH PMIs

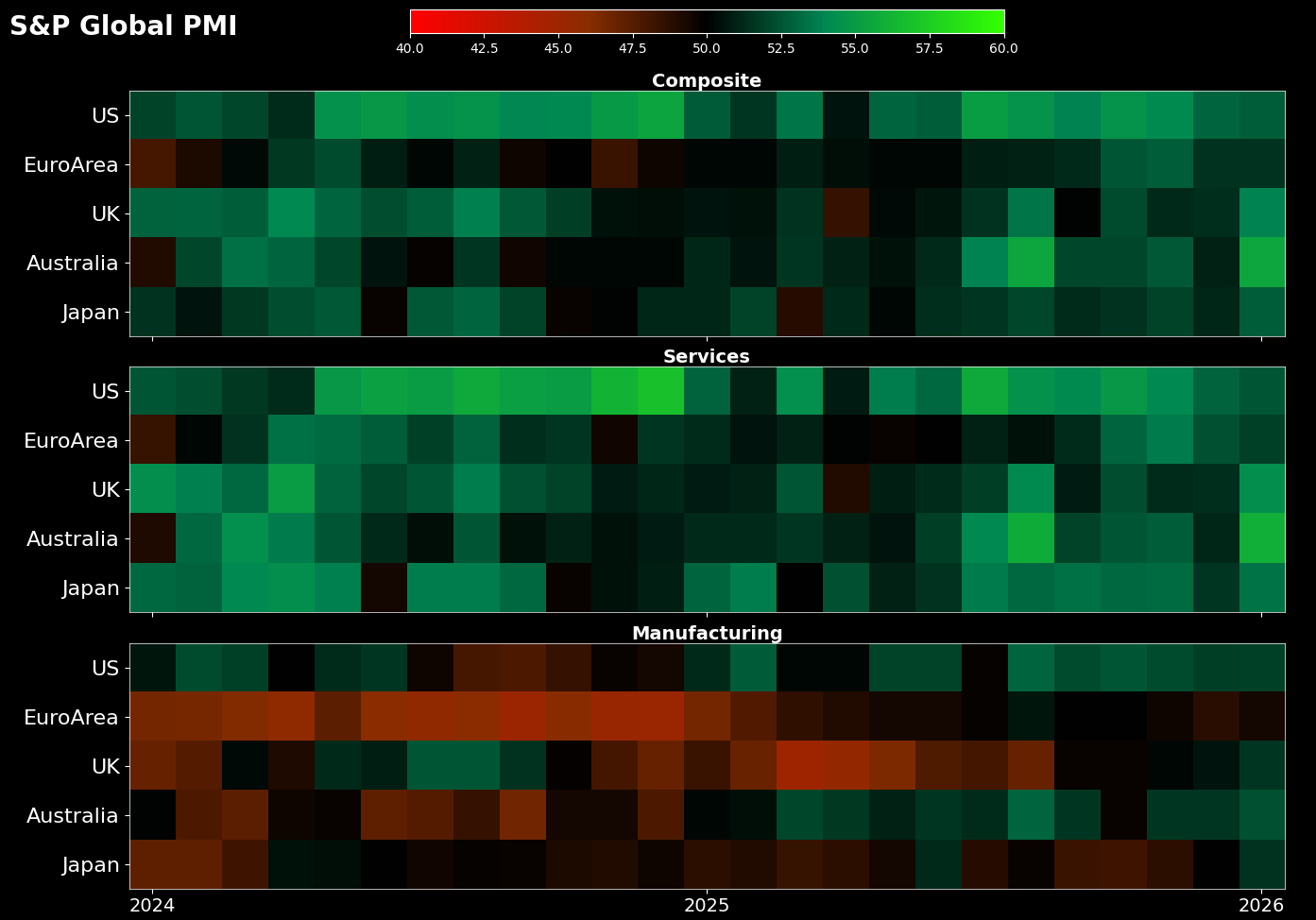

Latest Flash PMI reports show a broad improvement in major non-US economies, while the US expansion has continued to slow.

Recent rates of change according to the latest Flash PMIs favour non-US assets for the moment. Also considering heightened US political risks, I am cautious of jumping back into long USD bets too soon even though that is a trade idea that has my full attention over the near-term.

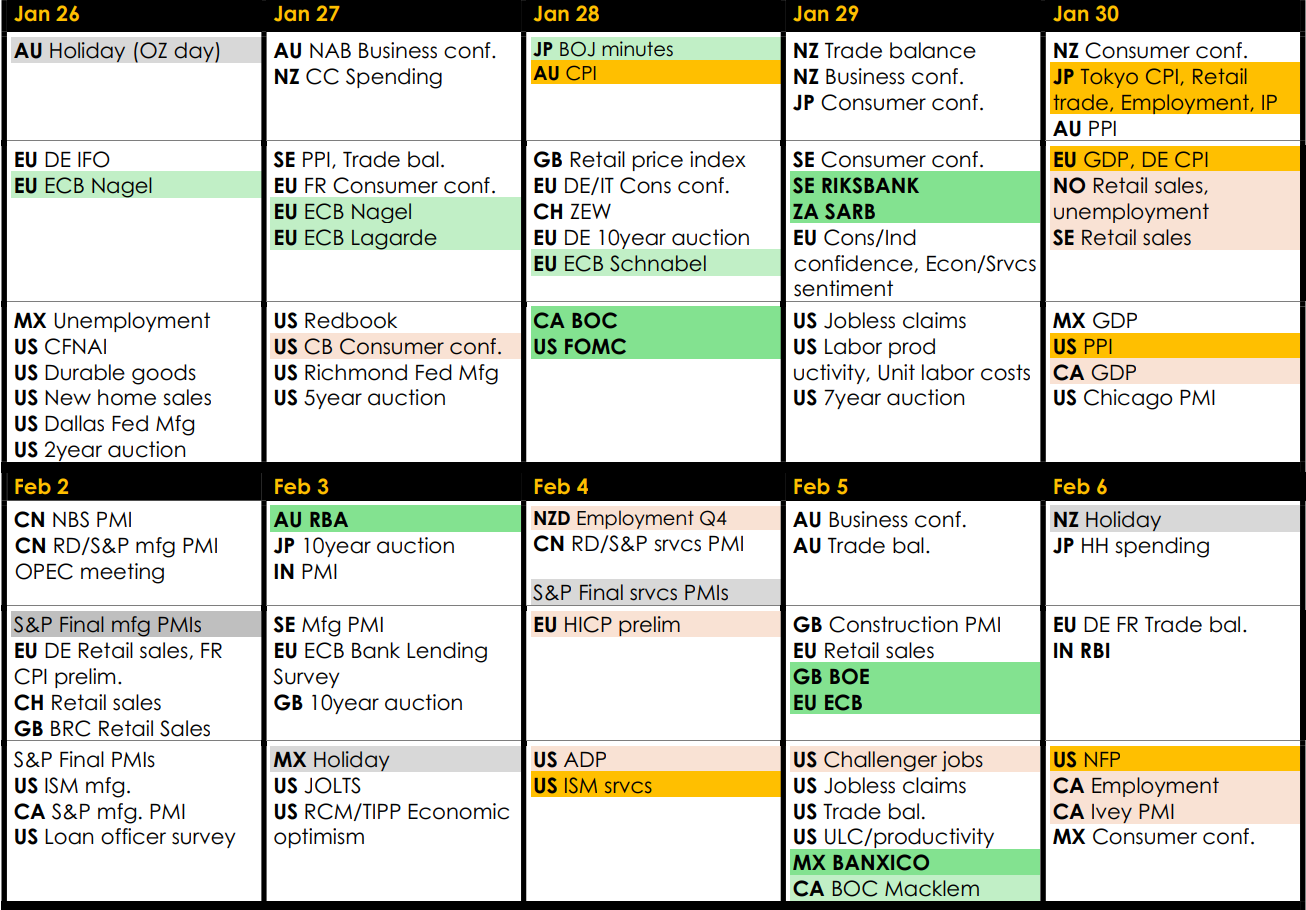

LOOKING AHEAD

Speaking of the Dollar, perhaps the FOMC could offer some relief to some recent selling. We also have the BOC and Riksbank meetings this week, followed by the RBA, BOE and ECB risks to factor in where I can quite easily think of a few trade ideas to think about based on how certain currencies have been trading recently.

In addition to another of economic data points to digest, we also have MSFT, META and TSLA reporting after-hours on Wednesday after FOMC, and AAPL after-hours on Thursday, along with plenty of other names that amounts to roughly 30% of S&P 500 market cap reporting this week.

Technicals

EQUITIES

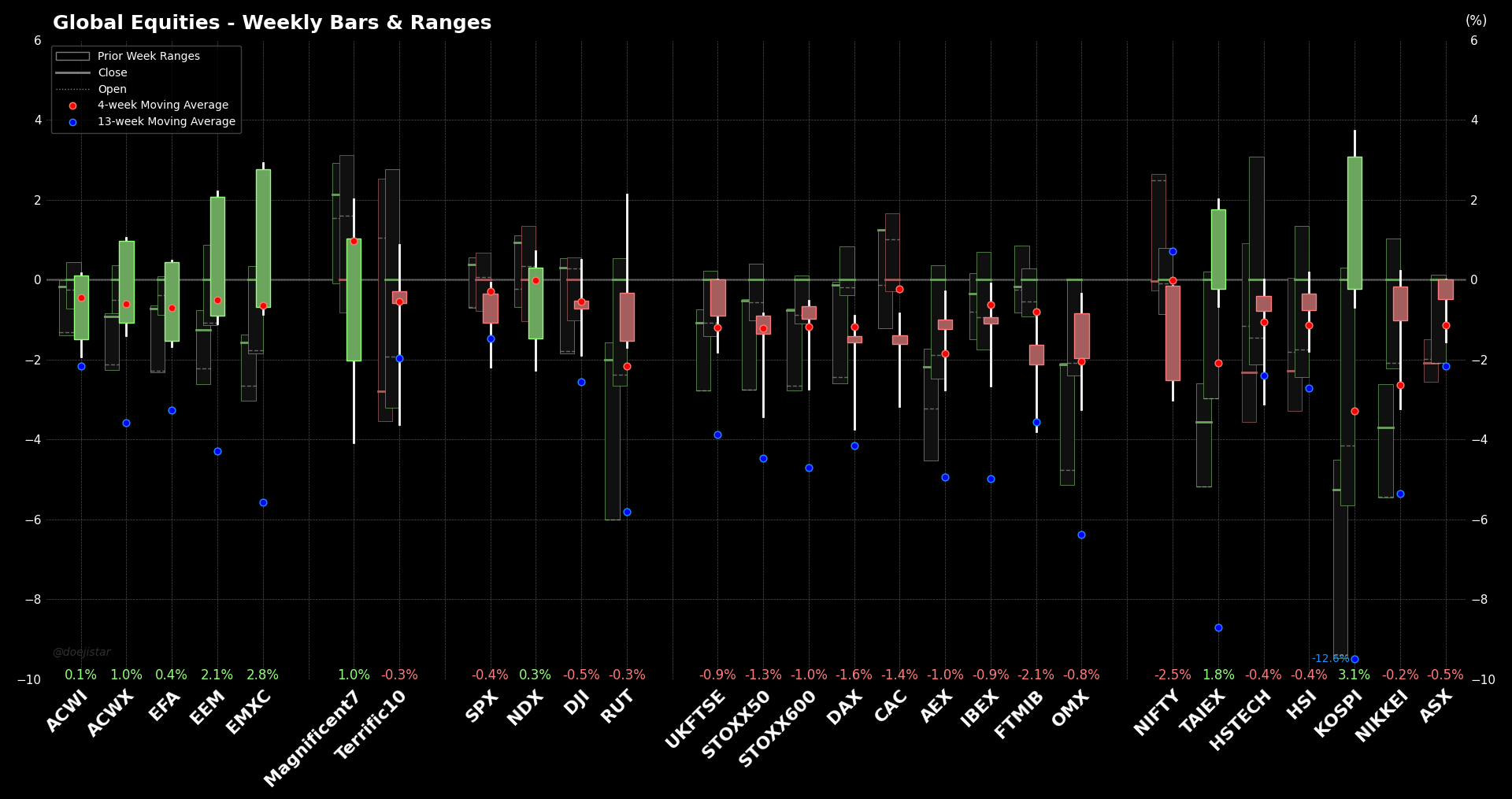

Global equities has had yet another strong week. Emerging markets were particularly strong, while US and European markets generally faltered. KOSPI and TAIEX continue to perform strongly which appear to be benefiting from an increasingly undersupplied chips market.

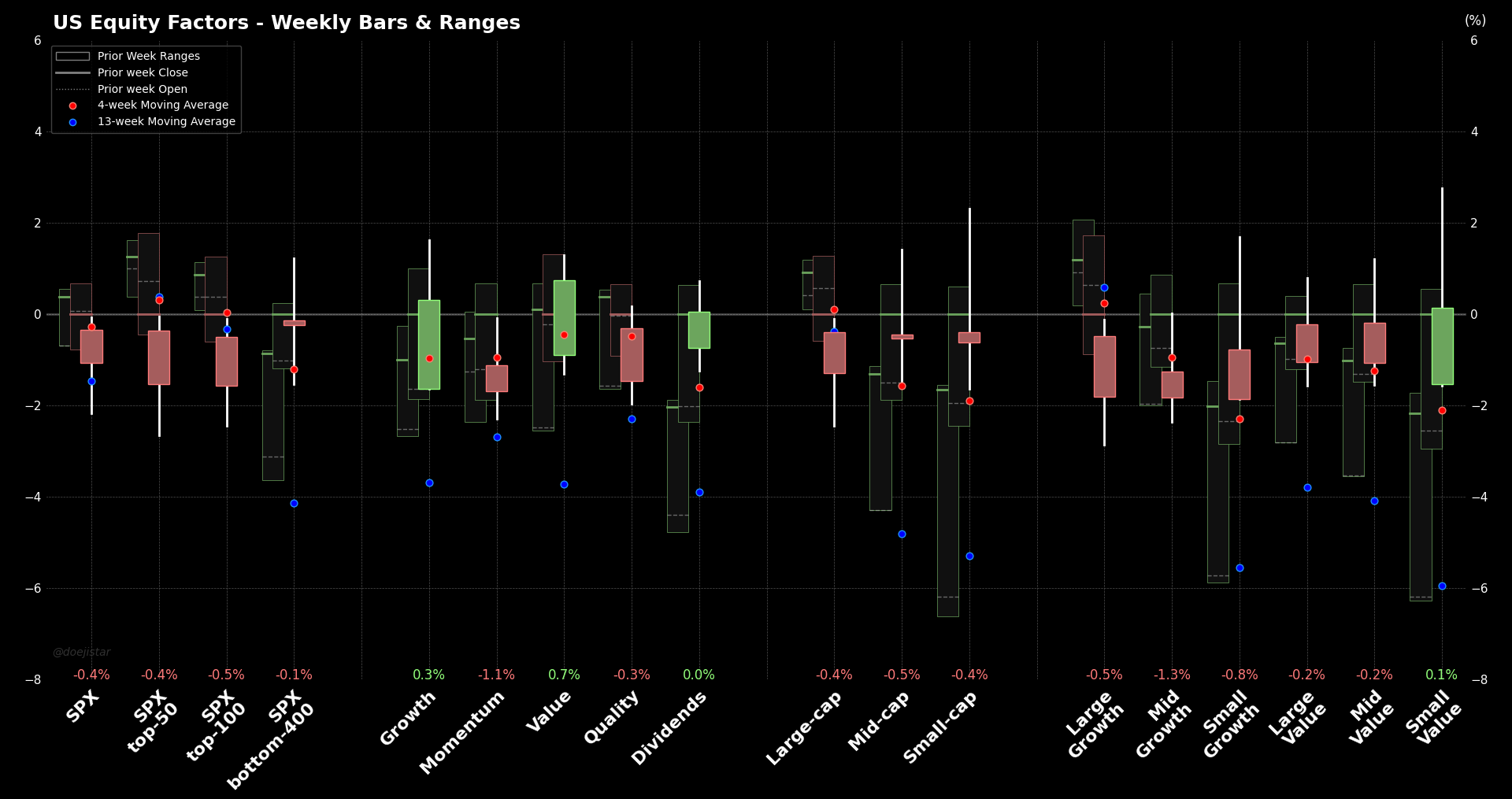

US equities are showing signs of the rally fading with factors finishing positive being up only marginally.

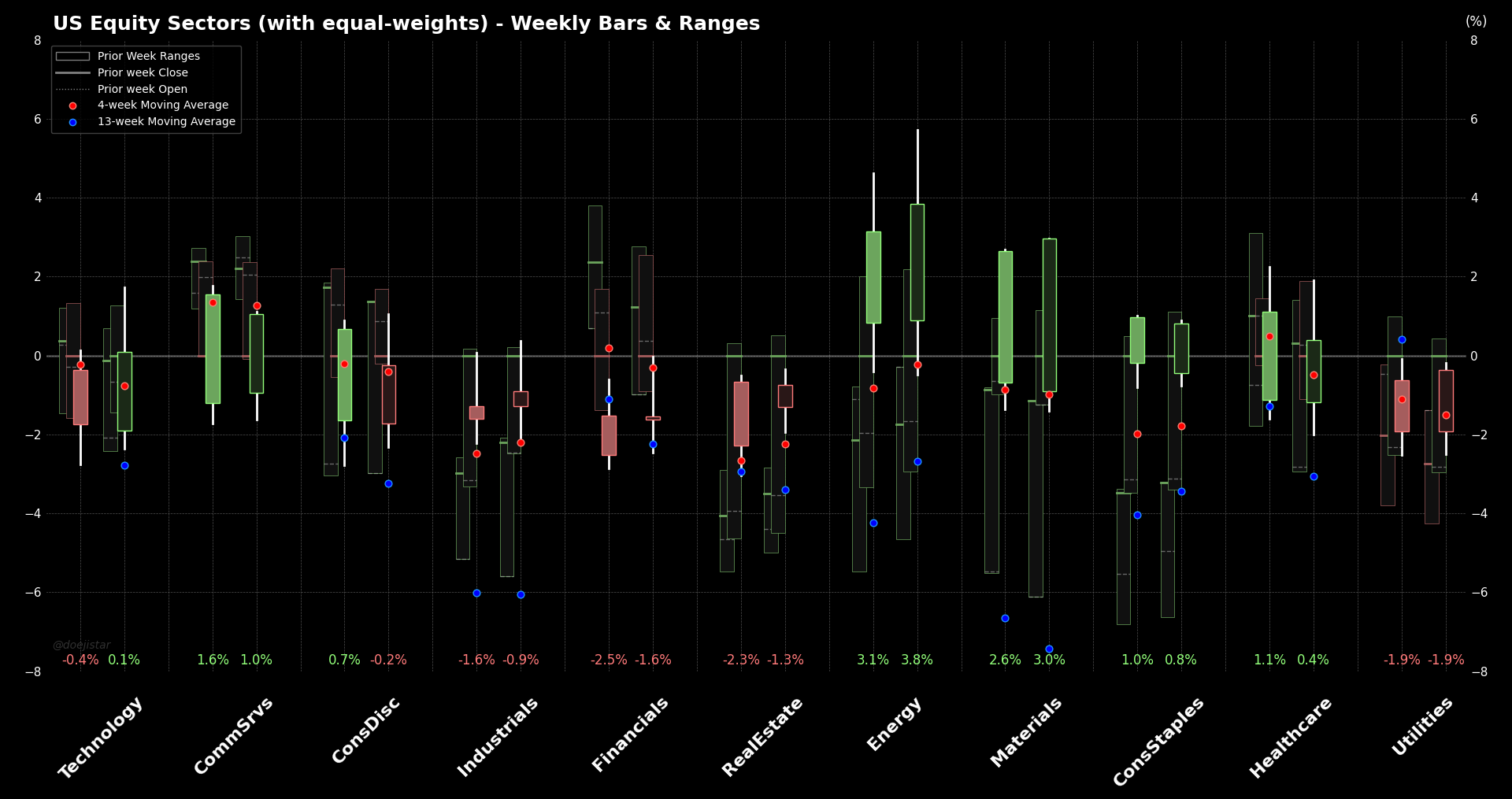

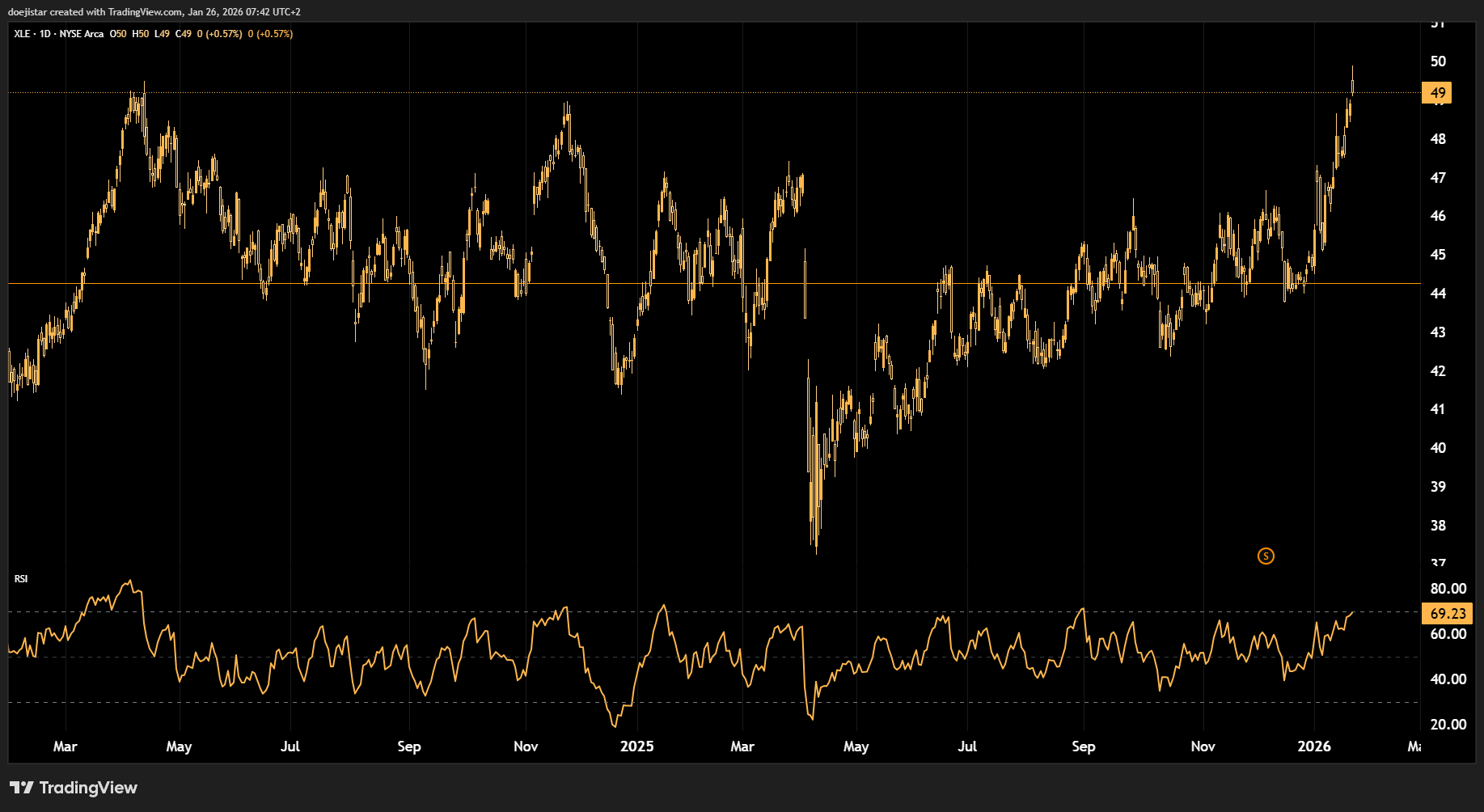

At the sector level, Energy continues to perform very strongly followed by Materials, while the Tech and AI-related sectors displayed some resilience last week after falling out of favour for many weeks.

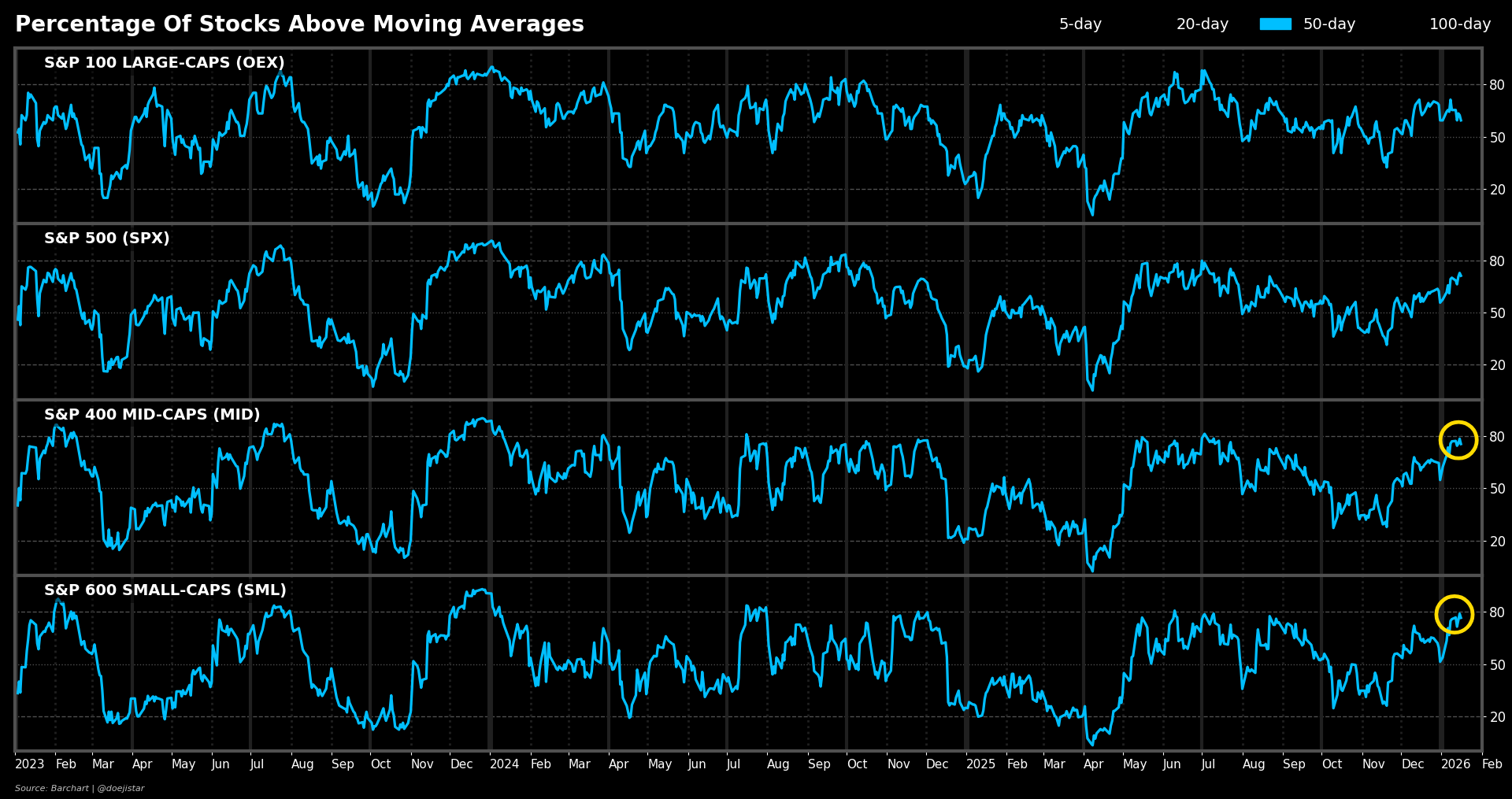

As flagged last week, the number of stocks trading above their 50dma's has reached overbought levels in the S&P Small and Mid-caps indices and are prone to a pullback. Mid-caps while the Large-caps OEX index has been slowly rolling over.

The Russell has printed a weekly evening star pattern closing just below the 2675 handle which opens up the strong possibility of a retest of the breakout level just below 2600. Weekly RSI been in contact with the 70 level the past two weeks and is beginning to curl over while the Daily RSI has printed a bearishly divergent higher-high last Thursday.

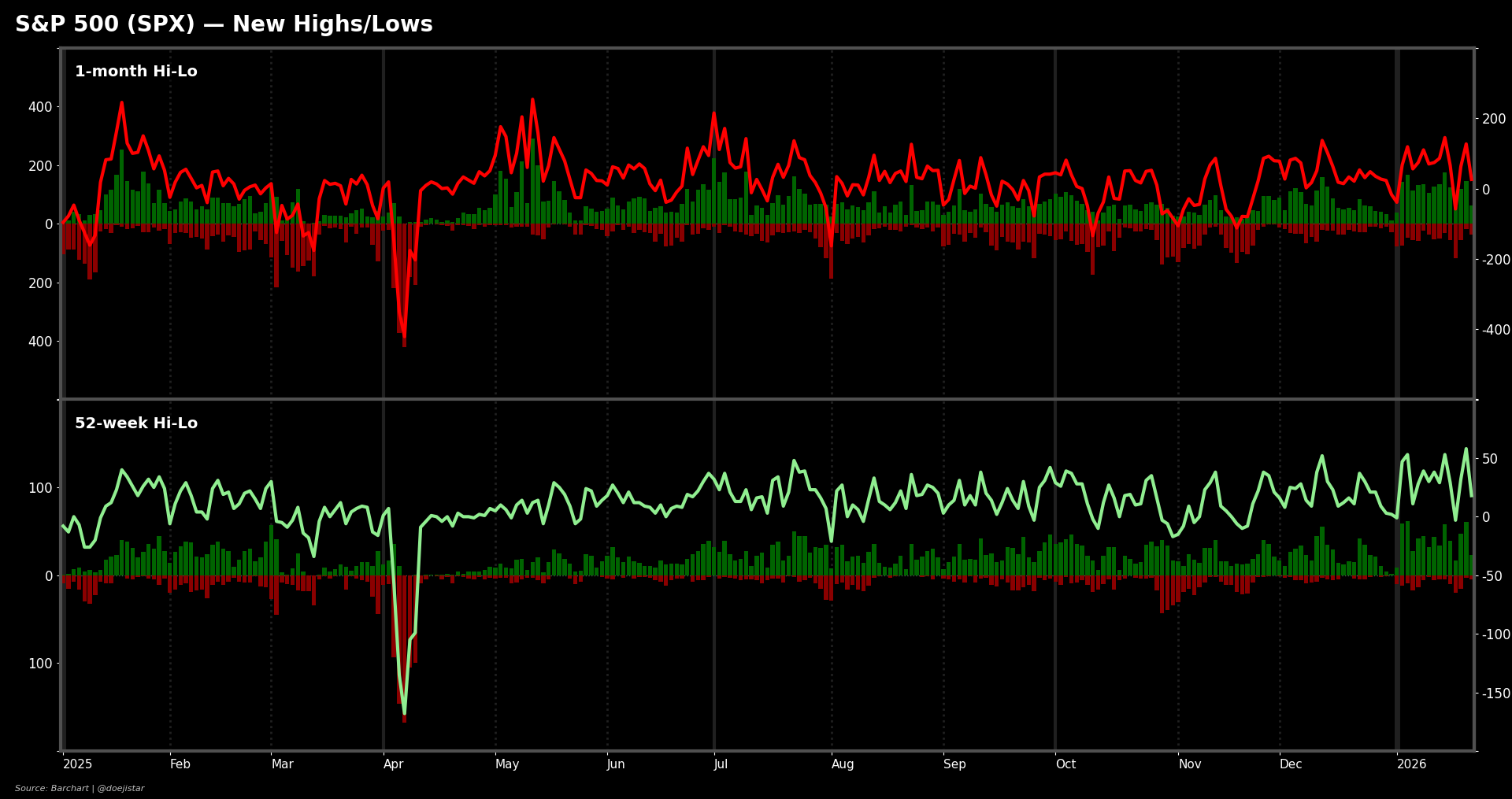

Number of S&P500 stocks making new highs has stalled out last week, with now more stocks making new 1-month lows than there are making new highs while the 52-week Hi-Lo spread is receding from the top end of the range.

SPX came within just 5pts of closing the gap left-behind by the selloff after Trump announced a 25% tariff over the long US-weekend. It's printed 2 consecutive indecision bars that is signalling a lack of strength

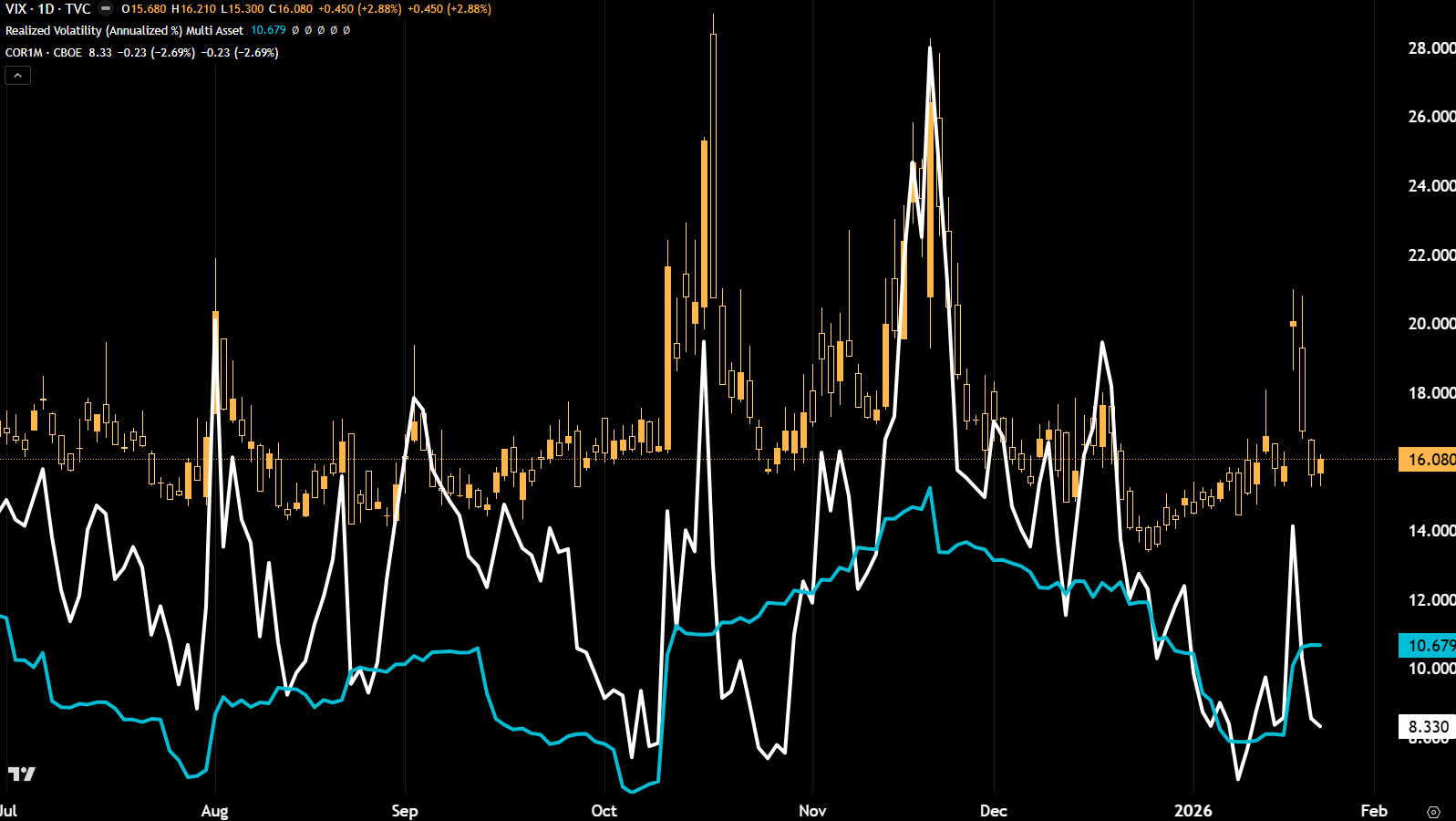

VIX has round-tripped back down to below the 16 level after going above 20 on last week's series of Greenland escalations and deescalations. Uncertainty around a Greenland deal remains, as well as the potential for the market to seek hedges against positioning and government shutdown risks.

While there are pockets of strength in Emerging markets, Energy and Materials, as well as mega-cap stocks finding some resilience, an overall look at the market shows deteriorating internals, particularly among those that have been the outperformers so far this month.

COMMODITIES

Bloomberg Energy and Metals subindices put in almost 10% gains last week driven by the massive rallies in NatGas, as well as Silver continuing to power higher.

I continue to like trading Crude Oil upside, which is still eyeing up a firm retest of the 63-64 area with a very strong base formed at 59 and a solid change in structure to higher lows and highs.

Nat Gas I've had a go at a short last week but after a lack of follow-through I managed to get out at breakeven. It appears the US winter blast could last well into February, but I do think there will be a trade there at some point as we reach the peak of the winter storm.

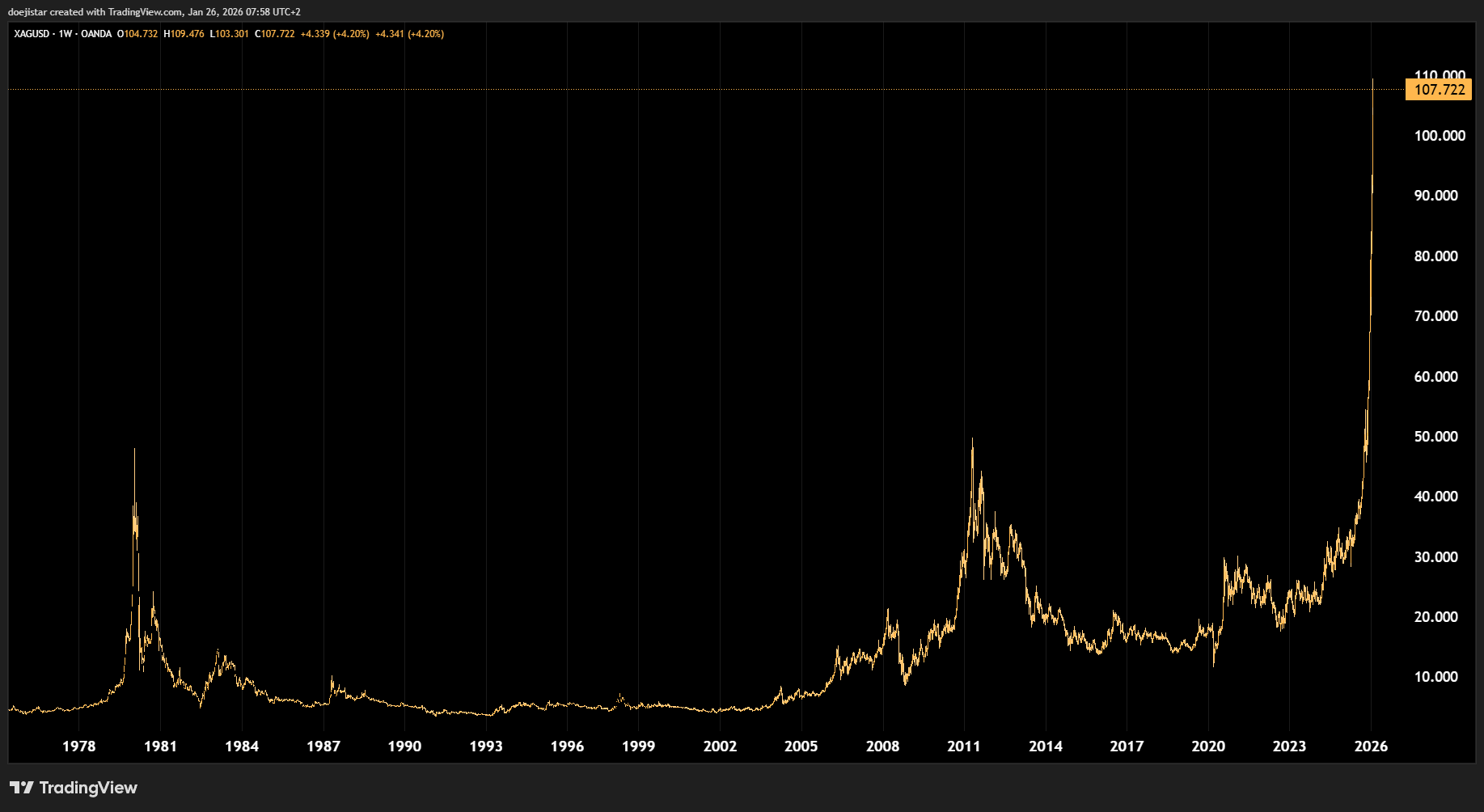

Silver! That is some sight to behold! We've breezed through the 100 handle without much resistance and we've been joking in the group that it'll probably be at 200 within a couple of months. Joking aside, I feel there needs to be a 'big' enough reason for the rally in precious metals to unravel, and it could very well come in the form of some rates volatility as discussed in the opening comments. I must be a glutton for punishment as I am fairly intent on having a few feelers on precious metal shorts ahead of some central bank meetings this week.

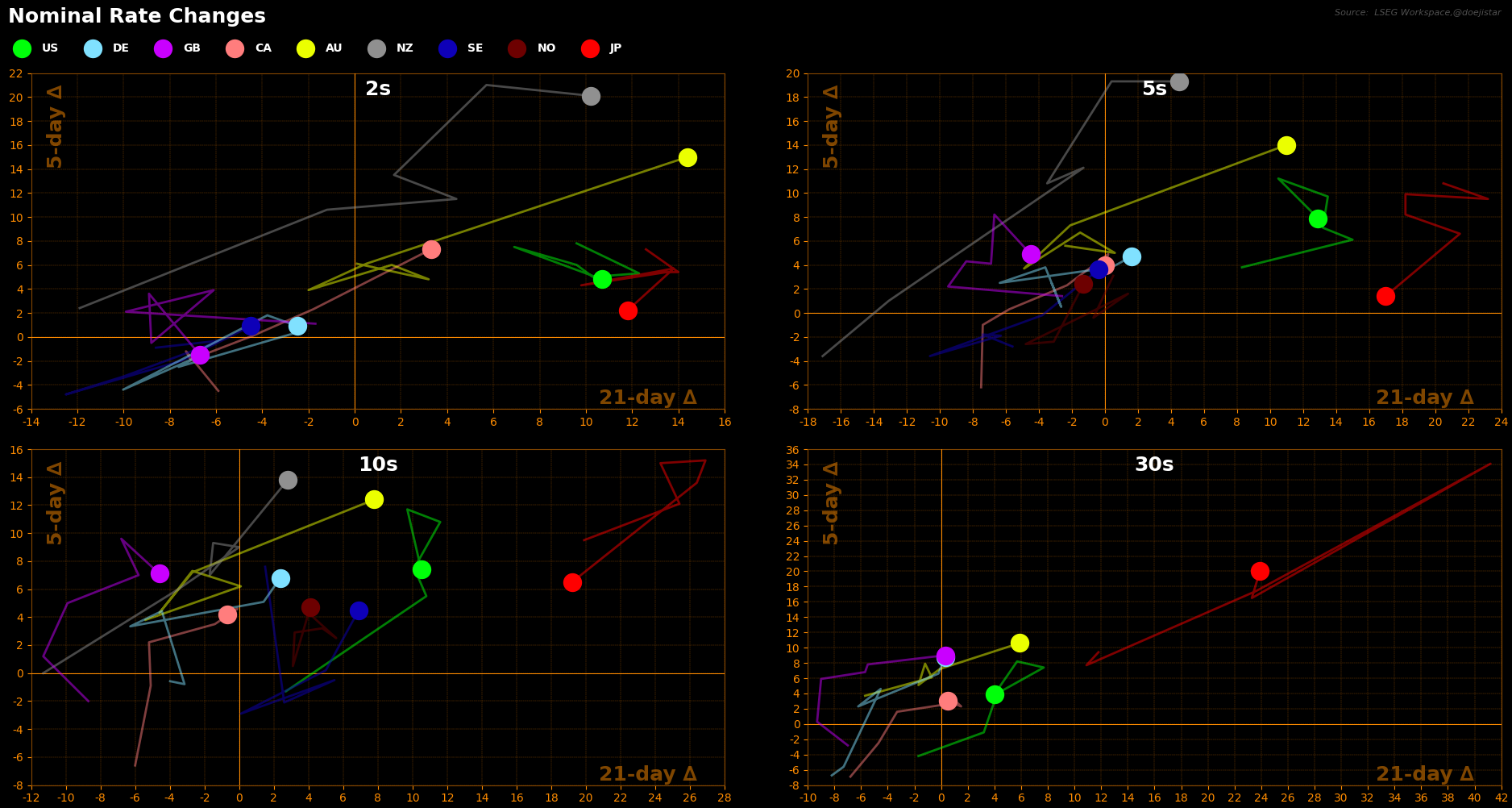

RATES & FX

Starting at the front-end, the market continued to rein in cuts to now pricing in roughly 50bps til the end of the year from 67bps at the start of the month. This very much looks like the wait and see level to see if the data starts tilting the odds towards 1 cut for the year, which I think it could do, but will probably have to see a couple jobs reports before this meaningfully changes.

I therefore expect the 2-year to stay resilient after its recent ascent given that the outlook for growth this year is healthy and a rebound in Energy prices to present some fresh upside risks to prices.

Economic data has been on a tad on the soft side recently so I'm inclined to think the 10year will be chopping around a bit before finding some direction. For now, we've seen a fairly strong reversal off the 4.3% handle setting up further mean reversion to the 4.17-19% area.

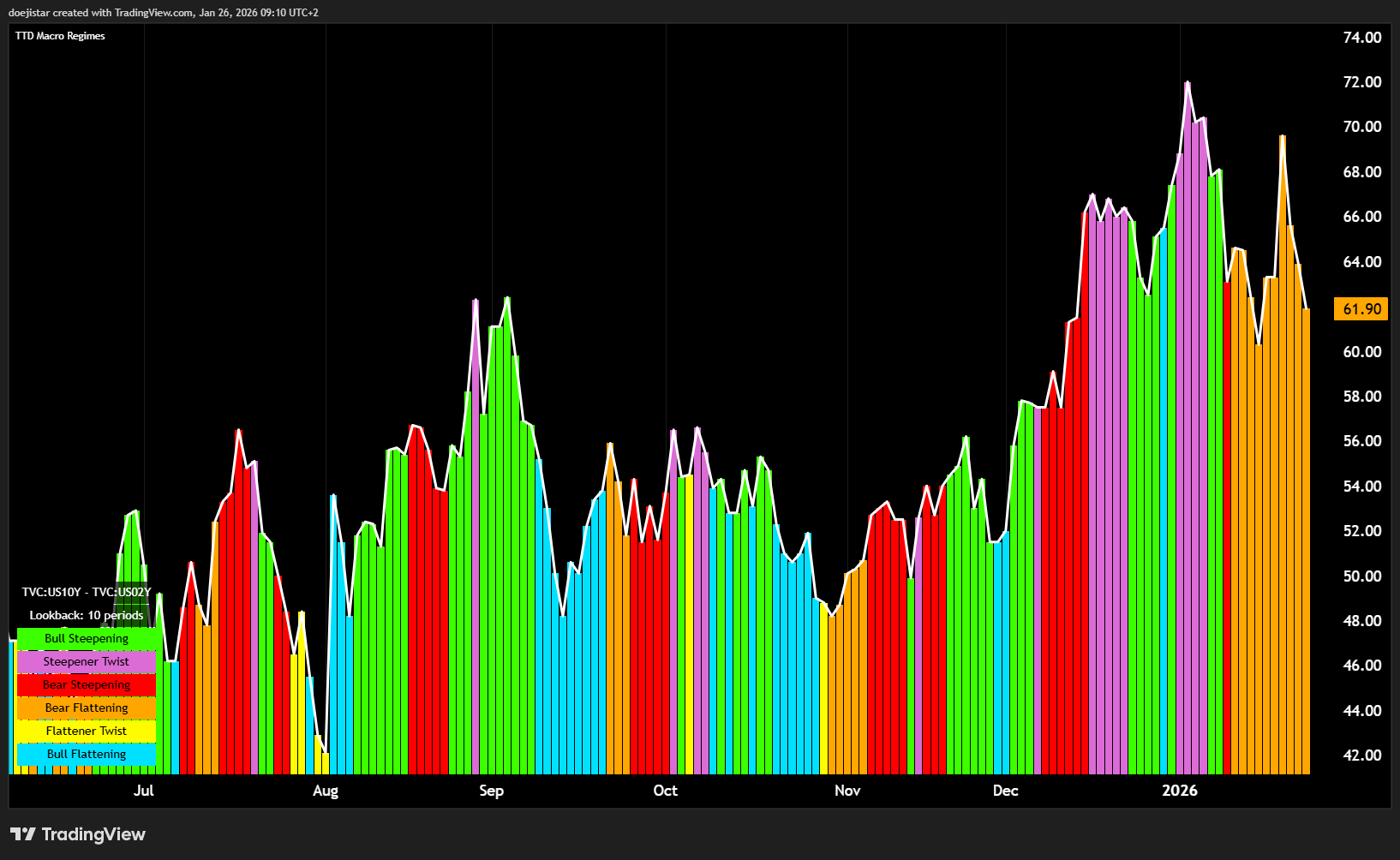

We've seen the 2s10s going through some bear flattening in recent weeks as the market priced out cuts after some steepening in the yield curve last month and I lean towards the curve being flatter as things are. It's a tough call however given the current geopolitical environment that could see the sell-America trade hit treasuries giving a lift to US yields, or treasuries find some safe-haven bid on heightened geopolitical uncertainty.

Looking at relative interest rate moves over the last two weeks, we've seen the upward move in US and JGB yields begin to peter out, while AUD and NZD yields have moved strongly higher.

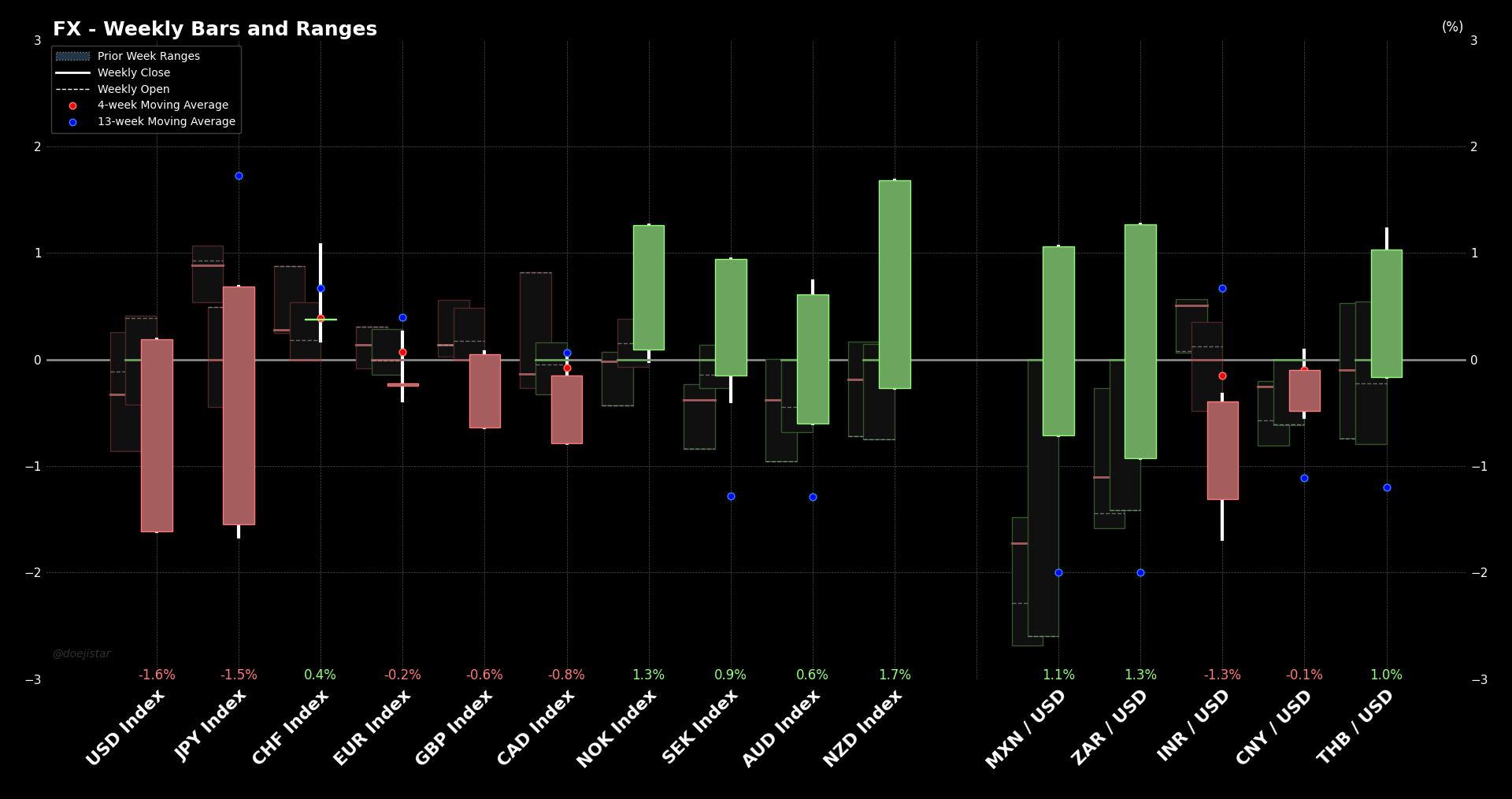

As a result, we've seen AUD and NZD perform well as FX markets traded with a risk-on tone last week with NOK SEK and a few EM's having a solid week of gains.

Looking at the DXY and its equal weighted rate spreads, it's at an interesting spot and probably looks about fair given their respective levels. Though I continue to maintain a positive view over the medium term for the USD, it seems that US political risks are just too high for the time being that there is a real sense of confidence lacking for the Dollar. Also, economic data of other major economies have gone further positive while the US data has softened a touch.

The Dollar does sit at very compelling levels to engage on the long side, so if one were to look at some long setups, it would be with the FOMC in mind to offer some temporary support in the lead-up.

For USD long candidates I think USDCAD and GBPUSD are the most compelling ideas. USDCAD is back to the trendline support from which it made a strong rebound. It may not produce a bounce like it did late-December, but it is still a technically strong level at 1.3690. GBPUSD also at equally compelling levels, with levels above the 1.36 handle seeing major swing highs last year.

Finally, a brief mention for USDJPY where I think the 154 handle is worth some attention this week. If intervention concerns soon subside, I think there is potential for the 154 handle to hold for a possible 154-156 trading range.

CRYPTO

Charts are looking miserable again and instead of running through the charts, I'll share some issues and doubts I have about crypto finding a meaningful rebound anytime soon which is stemming from the difficulty of finding answers or even any idea about where is the next wave of enthusiasm going to come? Some common narratives I've seen revolve around Trump making the US the 'crypto capital of the world', implying more deregulation, institutional involvement, as well as fed cuts and the dollar debasement narratives. But here's thing...

Crypto capital of the world, deregulation and institutionalisation- we've been hearing these things on repeat for quite some time that it's lost its punch, and if it has failed to support crypto in recent months, it's probably not what sparks the next wave of excitement. As for the Dollar debasement narratives, it is tied to fed policy as fed policy is tied to how weak/strong the US economy is. Let's start by reviewing recent crypto cycles which I think sets up a good basis for a forecast (we'll ignore everything from the 2021-23 period as there was a lot of weird things going on in crypto but to just focus on the 2023-25 cycle):

(1) In 2023-24, anticipation was building that a long disinflationary cycle would soon begin along with a rate cutting cycle that would take the fed funds rate from 5.5% to 3% or lower.

(2) As 2024 was underway, the Fed continued to delay the inevitable leaving the market disappointed until there were major concerns about the labour market crack. That came in August when the so-called 'Sahm-rule' recession indicator was triggered that prompted the market to aggressively price in cuts, and the Fed cutting 50bps at the next meeting.

(3) Those concerns came in August when the so-called 'Sahm-rule' recession indicator was triggered after the July NFP, prompting the market to price in cuts aggressively, and the Fed to cut rates at for the next 3 consecutive meetings. Everything was ripping and calls for 190k, 200k, 250k BTC began to swirl.

(4) By the end of 2024, the market was pricing in 150bps of cuts just for 2025! just as economic activity was sharply reaccelerating. That prompted the Fed to delay cuts and market to expect less aggressive cuts taking the wind out of the sails of the BTC rally.

(5) Not only did Trump's antics briefly impact economic activity, labor market started to show weakness, prompting expectations for more/sooner cuts again - risk assets and BTC rallies.

(5) Fed cuts interest rates in the last 3 consecutive meetings of 2025 and BTC rolled over... in fact, each rate cut roughly marked local BTC highs.

From the above example, it is quite clear that what drove BTC is the changes in rate cutting expectations. And with that in mind, we are currently in a situation where both GDP and wage growth is running at a rate above the current fed funds rate, and it doesn't appear that outlook is going to severely deteriorate from here anytime soon. What that implies is that crypto markets isn't likely to get the aggressive rate cutting expectations that drove bull cycles that it has sorely missed. since (5) last July. And just to address those that subscribe to the global liquidity narratives involving M2 money supply charts - there is much much to global liquidity than actual 'cash' and it's really a narrative-fitting exercise more than it is about meaningful analysis.