Week44 MacroTechnicals - Relative Exceptionalism

Trump, China, and trade - why this will be the overriding driver of markets and likely to extend the bull run in risk. Returning to a popular USD framework. A longer-term thesis for the USD. Game plan

This week we cover Trump, China, and trade, why it's likely to extend the bullish moment in risk assets regardless, and I return to some popular arguments to assess USD strength and introdcues some medium to long-term USD view. Then we look at the game plan for some thematic trading opportunities.

Macro

Trump-Xi Meeting

Bessent travelled to Malaysia to meet with Chinese delegates in preparation for the Trump-Xi meeting. What we know so far:

- "US and China Reach Trade ‘Framework’ Ahead of Trump-Xi Meeting";

- "China, US agree to preliminary framework deal in Malaysia, paving way for Xi-Trump talks" - Chinese negotiator Li Chenggang said the US position has been ‘tough’, whereas China has been ‘firm’ in defending its own interests and rights;

- "US Treasury Secretary Scott Bessent said on Sunday he has reached a "very substantial framework" with Chinese Vice Premier He Lifeng that will avoid 100% U.S. tariffs on Chinese goods and achieve a deferral of China's rare earths export controls" (RTS).

- Top quotes from Bessent to CBS and ABC - 100% tariffs on Chinese goods “is effectively off the table”, “I believe that they are going to delay that (rare earths export controls) for a year while they reexamine it.” Expects China to make “substantial” soybean purchases (annmarie hordern on X)

Discussion on "key issues" still said to be "ongoing" and “everything is on the table”, but there was a particular emphasis on a “framework” and “preliminary consensus” to prevent an immediate escalation. Preliminary talks seemed to have headed in the right direction, and we now look forward to Trump's Asia visit.

- October 26–27: Trump travels to Malaysia to participate in the ASEAN Summit in Kuala Lumpur and a bilateral meeting with Malaysian leadership;

- October 28: Trump travels to Japan for bilateral engagements with the Japanese government focusing on defense cooperation, supply chains, and economic/trade discussions as part of the broader Indo-Pacific outreach;

- October 29: Trump travels to Busan, meeting with South Korean President, keynote address at the APEC CEO luncheon, attend leaders’ working dinner

- October 30: Trump and Xi expected have a “bilateral meeting” on Thursday morning (local time) before returning to Washington.

The Trump-Xi meeting aside, Asian leaders are looking to take full advantage of the opportunity to have talks with Trump that I think the overall sentiment towards deescalating trade tensions - being a very broad and positive macro driver across all markets, will act as positive tailwind to sustaining the bullish momentum in risk. With that in mind for trading around some market events this week, I would look to take advantage of some spikes in intraday volatility to take trades in anticipation of more positive headlines this week.

Economic Data

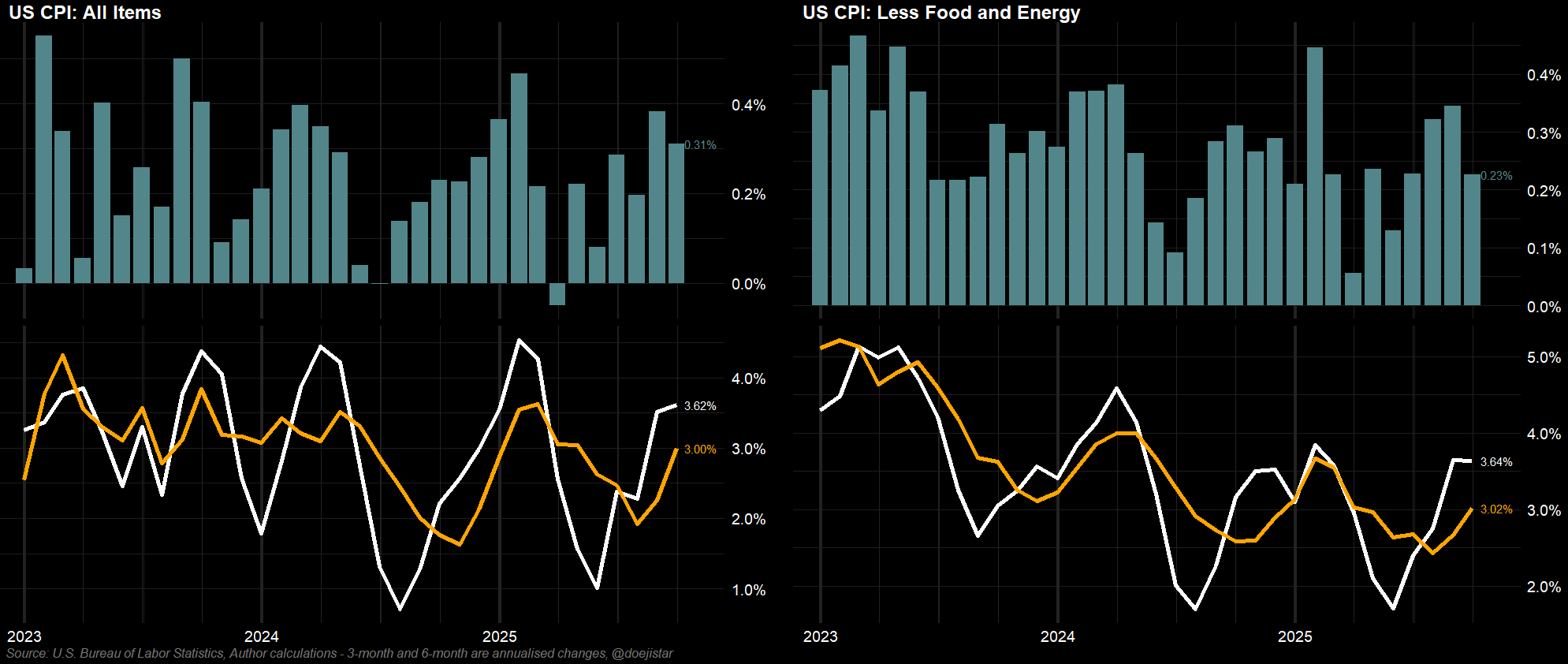

US CPI report for October was softer versus the prior month and against expectations. Headline came in at 0.31% versus 0.4% expected, and Core CPI was 0.23% versus 0.3% expected.

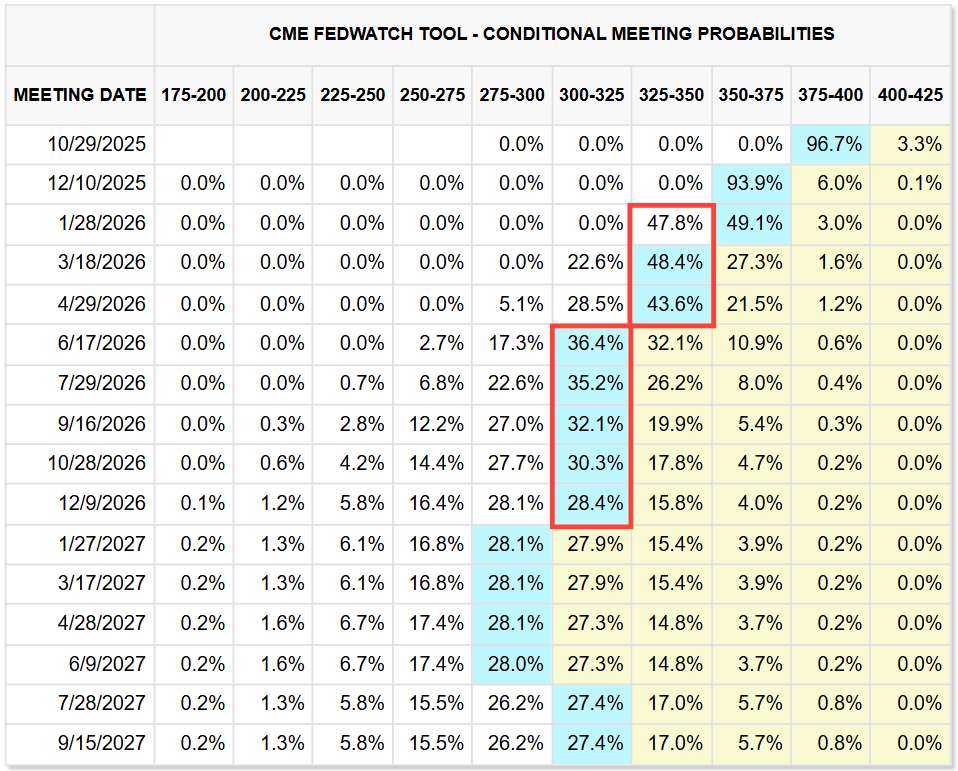

This report reaffirms the likelihood that the Fed will go ahead with the 25bps cut this week, and also leaving the market to fully expect a 3rd consecutive cut in December also that would take the fed funds target range to 3.25-3.50%. Looking into what's priced for 2026 (Table), the market fully expects 2 more cuts next year though far less clear about the exact timing of those cuts - roughly 1 in the 1st half and 1 in the 2nd half of next year.

We've also had inflation data from Canada and the UK last week. Canada posted a 0.1% m/m increase against the -0.1% expected. UK inflation reports came in softer with yr/yr readings print 2-tenths of a percent softer than expected and decelerating from the prior month's reading. Those and the softer US CPI report should ease inflation upside risks which, has been rebounding since May, and could further be booster by base effects at the start of 2026.

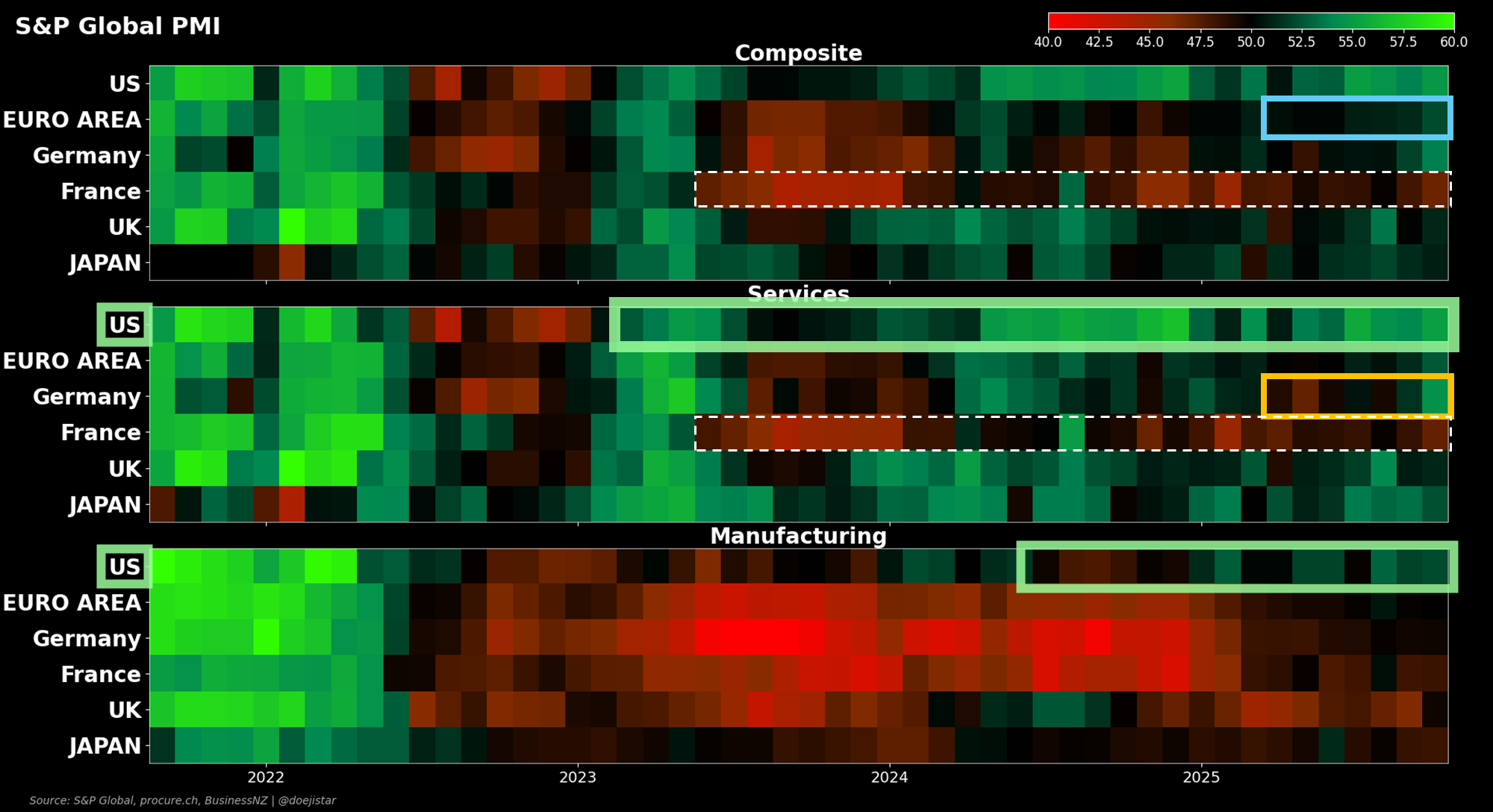

US continues to dominate the major economies, maintaining the higher PMI readings in both Manufacturing and Service sectors (Green). Europe extended their slow and steady trend of accelerating activity, Flash composite PMI rose to 52.2 in October and from 49.7 just 5 months earlier (Blue), Germany Services putting in a strong rebound to the highest Flash Services PMI to read 54.5 in in 30 months (Orange). UK and Japan appear stable, but France is notably showing a more recessionary outlook of this group (dashed White).

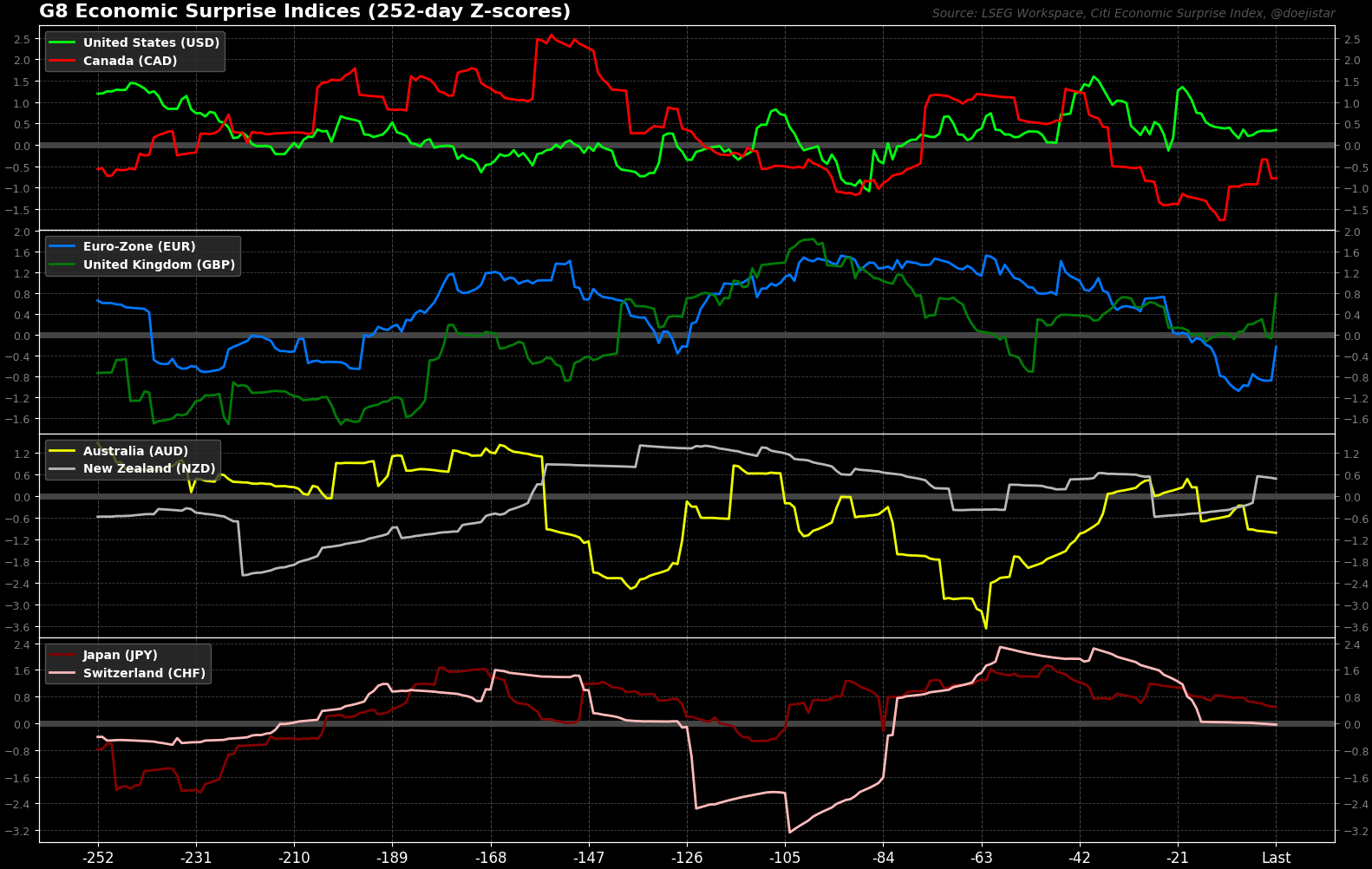

Top 2 panels with US CA EU and UK are positive, whereas bottom panel shows softness in economic data releases with the exception of New Zealand.

On review of all of the above, I think there are some good strategic ideas there which I'll discuss in the game plan and trading strategy for this week, as well as some detailed and interesting perspectives on why I think the USD could be now be in a '6 to 9-month buy-the-dip window'.

Relative Exceptionalism

Let's start by getting right into the Dollar - from short, medium to long-term.